E-Sports Market Size

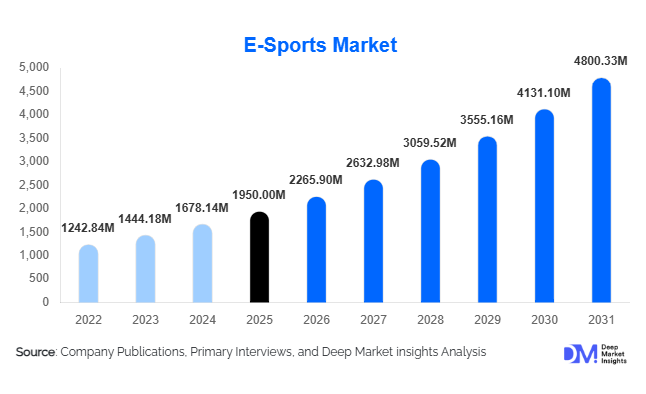

According to Deep Market Insights, the global E-Sports market size was valued at USD 1,950 million in 2025 and is projected to grow from USD 2,265.90 million in 2026 to reach USD 4800.33 million by 2031, expanding at a CAGR of 16.2% during the forecast period (2026–2031). The E-Sports market growth is primarily driven by rising global gaming audiences, increasing sponsorship and brand investments, and rapid adoption of advanced technologies in streaming and immersive gameplay.

Key Market Insights

- Mobile E-Sports continues to dominate, fueled by smartphone penetration, affordable internet access, and emerging markets in Asia-Pacific and Latin America.

- Sponsorship and advertising remain the largest revenue streams, reflecting strong brand engagement and growing monetization potential from digital and live audiences.

- Asia-Pacific is the fastest-growing region, led by China, South Korea, and India, with mobile gaming driving adoption and government-supported initiatives boosting infrastructure.

- Technological advancements, including AI, cloud gaming, and VR/AR integration, are enhancing both player performance and spectator engagement.

- Professionalization of E-Sports through leagues, organized teams, and global tournaments is solidifying E-Sports as a mainstream entertainment category.

- New monetization models such as NFTs, virtual merchandise, subscription content, and premium tournaments are expanding revenue opportunities beyond traditional sponsorships and media rights.

What are the latest trends in the E-Sports market?

Mobile-First E-Sports Growth

The global shift toward mobile gaming has made mobile E-Sports the largest segment by platform, accounting for nearly 45% of market share in 2025. Rapid smartphone adoption, improved mobile network infrastructure, and regionally tailored games have accelerated mobile participation and viewership. Countries such as India, Indonesia, and Brazil are witnessing explosive growth in mobile esports leagues and tournaments. Mobile-first tournaments are more scalable and cost-efficient than PC or console events, enabling organizers to reach wider audiences and attract sponsorships.

Technological Integration Enhancing Engagement

AI analytics, VR/AR experiences, and cloud gaming are reshaping both competitive play and spectator experiences. AI tools improve player performance analysis and coaching, while VR/AR platforms create immersive virtual arenas for viewers. Cloud gaming allows lower-end devices to participate in high-quality competitive gaming, widening access in emerging markets. Interactive features such as live voting, real-time statistics, and augmented broadcast overlays are increasing engagement and monetization opportunities, particularly among Gen Z and millennial audiences.

What are the key drivers in the E-Sports market?

Rising Global Gaming Audience

With over 500 million E-Sports viewers worldwide, growing internet penetration and the acceptance of gaming as mainstream entertainment are key growth drivers. This demographic skews younger, tech-savvy, and highly engaged, making them attractive for advertisers, sponsors, and subscription-based platforms. Social media amplification further drives audience growth and global engagement.

Increasing Sponsorship and Brand Investments

Global brands across technology, automotive, and consumer sectors are investing heavily in E-Sports sponsorships, which now account for roughly 40% of total market revenue. High-value sponsorship deals, event tie-ins, and brand activations provide companies with direct access to engaged digital audiences, driving revenue growth and market expansion.

Advanced Streaming and Connectivity Technologies

The expansion of 5G networks, low-latency streaming, and improved broadband infrastructure is enabling seamless live broadcasts of tournaments globally. These technologies enhance viewer experience, increase retention, and support interactive features, making tournaments more engaging and scalable.

What are the restraints for the global market?

Lack of Standardized Governance

E-Sports operates across multiple jurisdictions, often with inconsistent rules and regulations. Issues related to player contracts, match-fixing, and intellectual property rights pose challenges, potentially undermining market credibility and long-term growth.

Revenue Concentration

Heavy reliance on sponsorships and media rights creates vulnerability to economic downturns and fluctuations in advertising budgets. Diversifying revenue streams through in-game monetization, subscriptions, and digital merchandise remains a key challenge for participants.

What are the key opportunities in the E-Sports industry?

Emerging Regional Markets

Southeast Asia, India, Latin America, and the Middle East present significant growth opportunities due to rising smartphone penetration, affordable internet, and government recognition of E-Sports as a professional sport. Governments are supporting infrastructure, organizing leagues, and funding tournaments, creating fertile ground for new entrants and expansion of existing players.

Technology-Driven Monetization

Integrating AI, AR/VR, and cloud gaming unlocks new revenue streams and audience engagement opportunities. Interactive viewing experiences, virtual merchandise, and subscription-based premium content enhance monetization and reduce dependence on traditional sponsorships.

Diversification of Revenue Models

Beyond sponsorships and media rights, the market offers opportunities in digital content, in-game purchases, NFTs, and fan tokens. Brands can leverage E-Sports for targeted marketing, and platforms can monetize through subscriptions, pay-per-view events, and exclusive content offerings.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1950 Million |

| Market Size in 2026 | USD 2265.90 Million |

| Market Size in 2031 | USD 4800.33 Million |

| CAGR | 16.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Platform Insights

Mobile E-Sports dominates the global market, accounting for approximately 45% of total market share in 2025, primarily driven by its accessibility, lower entry barriers, and widespread smartphone penetration. The rapid expansion of affordable high-speed internet and 4G/5G networks in emerging economies such as India, Indonesia, and Brazil has enabled mass participation in mobile-based tournaments. Additionally, mobile E-Sports benefits from shorter game formats, localized content, and lower infrastructure requirements, making it highly scalable for organizers and attractive for sponsors targeting large, young audiences.

PC-based E-Sports continues to maintain a strong presence, particularly in developed regions such as North America, Europe, and South Korea, where high-performance gaming infrastructure, established franchises, and legacy titles drive consistent engagement. This segment is supported by premium tournaments, higher prize pools, and a dedicated enthusiast base. Console-based E-Sports, while smaller in comparison, is witnessing steady growth in North America and Europe, driven by franchise-based leagues and strong publisher support. The overall platform trend indicates a shift toward mobile-first ecosystems in high-growth regions, while PC and console platforms retain dominance in premium and professional competitive gaming segments.

Game Genre Insights

Multiplayer Online Battle Arena (MOBA) games lead the E-Sports market, accounting for approximately 30% of global market share in 2025. This dominance is driven by well-established global tournaments, strong publisher backing, and highly engaged player communities. MOBA titles offer strategic depth, team-based gameplay, and long match durations, making them ideal for both competitive play and spectator engagement. Their structured league ecosystems and recurring tournaments provide stable revenue streams through sponsorships, media rights, and in-game monetization.

First-Person Shooter (FPS) and battle royale genres are among the fastest-growing segments, fueled by their appeal to younger audiences and high-intensity gameplay formats suitable for live streaming. These genres benefit from shorter match cycles, high replayability, and strong integration with streaming platforms, making them attractive for advertisers and content creators. Sports simulation and fighting games also contribute to niche but stable segments, particularly in regions with strong console gaming cultures. Overall, genre diversification is enhancing audience reach while maintaining strong monetization potential across different player demographics.

Audience Insights

Enthusiast viewers represent the core revenue-generating segment, contributing approximately 65% of total audience-related revenue in 2025. This segment includes highly engaged users who regularly watch tournaments, subscribe to premium content, purchase merchandise, and participate in interactive features such as live chats and virtual events. Their high engagement levels make them particularly valuable for advertisers and sponsors, driving higher revenue per user compared to casual viewers.

Casual viewers, while contributing a smaller share of direct revenue, represent a significant growth opportunity for the market. As free-to-play models, mobile accessibility, and social media integration expand, casual audiences are increasingly converting into active participants. The introduction of interactive viewing features, gamified streaming experiences, and localized content is further enhancing engagement among this segment. The overall trend indicates a gradual expansion of the audience base, with monetization strategies evolving to capture value from both high-engagement and mass-market viewers.

Explore more data points, trends and opportunities Download Free Sample Report

E-Sports Market Segmentations

By Revenue Stream

- Media Rights

- Sponsorship & Advertising

- Publisher Fees

- Merchandise & Tickets

- Digital Content & In-game Purchases

By Platform

- PC-based E-Sports

- Console-based E-Sports

- Mobile E-Sports

By Game Genre

- MOBA

- First-Person Shooter (FPS)

- Real-Time Strategy (RTS)

- Battle Royale

- Sports Simulation

- Fighting Games

By Audience Type

- Casual Viewers

- Enthusiast Viewers

By Event Type

- Online Tournaments

- Offline/LAN Events

- Hybrid Events

Regional Insights

North America

North America accounts for approximately 30% of the global E-Sports market in 2025, led by the United States, which serves as a hub for major E-Sports leagues, streaming platforms, and sponsorship deals. The region’s growth is driven by advanced digital infrastructure, high consumer spending on gaming and entertainment, and strong participation from global brands investing in sponsorships and advertising. Franchise-based league models, particularly in FPS and sports simulation games, are well-established in this region, providing stable revenue streams. Canada is also contributing to regional growth through increasing mobile gaming adoption and investments in local esports ecosystems. The presence of leading publishers and content creators further strengthens North America’s position as a mature and high-value market.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing region, accounting for around 40% of global market share in 2025. China dominates the regional landscape due to its massive gaming population, strong publisher ecosystem, and government-supported E-Sports initiatives. South Korea remains a global pioneer, with advanced infrastructure, professional leagues, and a deeply ingrained gaming culture. India is emerging as the fastest-growing market in the region, driven by rapid smartphone penetration, affordable data, and increasing investments in local tournaments and streaming platforms. Southeast Asian countries such as Indonesia and Vietnam are also experiencing significant growth, supported by mobile-first gaming trends. The region’s expansion is primarily driven by demographic advantages, technological adoption, and strong government and private sector investments.

Europe

Europe holds approximately 20% of the global E-Sports market, with key contributions from Germany, the United Kingdom, and France. The region benefits from well-developed digital infrastructure, strong regulatory frameworks, and increasing institutional recognition of E-Sports as a professional discipline. Growth in Europe is driven by rising investments in organized leagues, university-level E-Sports programs, and partnerships between traditional sports organizations and gaming companies. Additionally, European audiences show a strong preference for interactive and community-driven gaming experiences, which is encouraging innovation in streaming and event formats. The region is also witnessing increased adoption of sustainable and long-term E-Sports ecosystem development strategies.

Latin America

Latin America is emerging as a high-growth region, led by Brazil and Mexico, where mobile gaming adoption is rapidly increasing. The region’s growth is driven by improving internet infrastructure, a young and digitally engaged population, and increasing access to affordable smartphones. Local tournaments and regional leagues are gaining traction, attracting both domestic and international sponsors. Additionally, Latin America is benefiting from increasing consumption of global E-Sports content, enabling local players and organizations to participate in international ecosystems. The region’s cost advantages and expanding audience base make it an attractive market for new entrants and investment.

Middle East & Africa

The Middle East & Africa region is witnessing accelerated growth, supported by significant government investments and strategic initiatives. Countries such as Saudi Arabia and the United Arab Emirates are investing heavily in E-Sports infrastructure, including dedicated arenas, gaming hubs, and international tournaments, positioning themselves as global E-Sports destinations. These initiatives are part of broader economic diversification strategies, such as Saudi Arabia’s Vision 2031. In Africa, countries like South Africa and Nigeria are driving growth through expanding professional leagues and increasing mobile gaming adoption. The region’s growth is further supported by a young population, rising internet penetration, and increasing interest from global investors and sponsors looking to tap into new markets.

Key Players in the E-Sports Market

- Tencent Holdings

- Activision Blizzard

- Electronic Arts

- Riot Games

- Valve Corporation

- Epic Games

- Take-Two Interactive

- Nintendo

- Ubisoft

- Garena

- ESL Gaming

- DreamHack

- Modern Times Group (MTG)

- Huya Inc.

- DouYu International