E-Cigarette Market Size

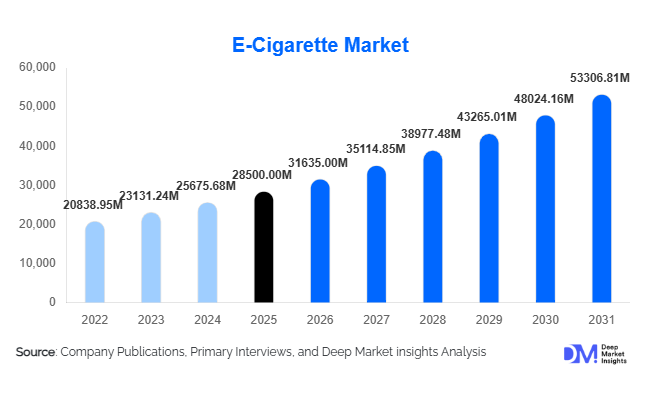

According to Deep Market Insights, the global e-cigarette market size was valued at USD 28,500 million in 2025 and is projected to grow from USD 31,635.00 million in 2026 to reach USD 53,306.81 million by 2031, expanding at a CAGR of 11.0% during the forecast period (2026–2031). The e-cigarette market growth is primarily driven by rising consumer shift toward reduced-risk nicotine alternatives, increasing demand for smoking cessation products, rapid product innovation in vaping devices and e-liquids, and expanding digital and retail distribution networks across global markets.

Key Market Insights

- E-cigarettes are increasingly positioned as harm-reduction alternatives, driving strong substitution demand from traditional combustible cigarette users.

- Disposable and pod-based systems are gaining rapid popularity, particularly among younger consumers, due to affordability and convenience.

- North America remains the largest market, led by high vaping penetration and strong retail infrastructure in the United States.

- Asia-Pacific is the fastest-growing region, supported by manufacturing dominance in China and rising adoption in Japan, South Korea, and India.

- Flavor innovation and nicotine salt formulations are significantly influencing consumer switching behavior and brand loyalty.

- Online retail channels are expanding rapidly, reshaping product accessibility and direct-to-consumer engagement strategies.

What are the latest trends in the e-cigarette market?

Shift Toward Disposable and Closed Pod Systems

The market is witnessing a strong shift toward disposable e-cigarettes and closed pod systems due to their ease of use, portability, and low upfront cost. These products eliminate the need for maintenance and refilling, making them highly attractive to first-time users and younger consumers. Manufacturers are increasingly focusing on compact designs with pre-filled nicotine salt formulations, which deliver faster nicotine satisfaction. This trend is reshaping product portfolios globally, with disposable devices accounting for nearly half of new product launches in several developed markets.

Digitalization and Direct-to-Consumer Expansion

E-commerce platforms and brand-owned digital stores are transforming how consumers purchase vaping products. Online channels provide wider product variety, discreet purchasing options, and subscription-based models for e-liquids and accessories. Social media marketing, influencer collaborations, and targeted digital campaigns are playing a key role in brand awareness. This digital shift is especially strong in North America and Europe, where regulatory frameworks still allow controlled online sales, significantly boosting market penetration.

What are the key drivers in the e-cigarette market?

Rising Demand for Smoking Alternatives

A major growth driver is the global transition from traditional tobacco smoking to alternative nicotine delivery systems. Increasing awareness of smoking-related health risks, combined with higher taxation on cigarettes, is accelerating the adoption of vaping products. Governments in several developed regions are also supporting harm-reduction strategies, indirectly boosting market growth.

Continuous Product Innovation

Technological advancements such as temperature control systems, nicotine salt technology, leak-proof pod designs, and smart vaping devices are significantly improving user experience. Flavor diversification, including fruit, menthol, and hybrid blends, is also enhancing consumer retention and encouraging repeat purchases across global markets.

Expanding Retail and Online Distribution Networks

The rapid expansion of vape specialty stores, convenience retail penetration, and digital commerce platforms has significantly increased product availability. Improved logistics infrastructure and direct-to-consumer branding strategies are allowing manufacturers to reach new consumer segments more efficiently.

What are the restraints for the global market?

Stringent Regulatory Restrictions

Regulatory uncertainty remains a key challenge, with many countries imposing strict rules on nicotine concentration, flavor bans, advertising limitations, and product approvals. Sudden policy changes create volatility and limit market expansion opportunities for manufacturers.

Health Concerns and Public Perception Issues

Despite being marketed as safer alternatives, the long-term health impacts of vaping remain under scrutiny. Concerns over youth addiction, nicotine dependency, and respiratory effects continue to influence public perception and may lead to stricter regulations in the future.

What are the key opportunities in the e-cigarette industry?

Expansion in Emerging Markets

Emerging economies across Asia-Pacific, Latin America, and parts of the Middle East present significant growth opportunities. As regulatory frameworks evolve, countries with large smoking populations are gradually opening up to controlled vaping adoption, creating untapped market potential for global players.

Smart and Connected Vaping Devices

The integration of IoT-enabled features, usage tracking apps, and smart nicotine control systems is creating a premium product segment. These innovations enhance personalization and user engagement, attracting tech-savvy consumers in developed markets.

Growth of Sustainable and Recyclable Products

Environmental concerns are driving demand for recyclable pods, refillable systems, and eco-friendly packaging. Companies investing in sustainability-focused product lines are expected to gain a competitive advantage as regulatory pressure around electronic waste increases.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28500 Million |

| Market Size in 2026 | USD 31635 Million |

| Market Size in 2031 | USD 53306.81 Million |

| CAGR | 11% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Rechargeable e-cigarettes continue to dominate the global market, accounting for approximately 48% share in 2025, primarily driven by their superior cost efficiency, long-term usability, and ability to deliver consistent nicotine satisfaction. These devices, particularly closed pod systems, are widely preferred by transitioning smokers due to their ease of use, reduced maintenance compared to open systems, and compatibility with nicotine salt formulations. The leading segment growth is further supported by continuous innovation in battery efficiency, leak-proof designs, and compact form factors, which enhance user convenience and portability. Disposable e-cigarettes are emerging as the fastest-growing segment, fueled by their low upfront cost, regulatory simplicity in certain markets, and strong appeal among first-time users and younger demographics. Meanwhile, modular or open-system vaporizers cater to experienced users seeking customization in vapor production and flavor intensity, although their share is gradually declining due to increasing regulatory scrutiny. Hybrid devices are gaining traction in premium niches, combining features of traditional vaping and heat-not-burn technologies. Overall, the industry trend is shifting toward compact, high-performance, and user-friendly devices, reshaping product development strategies globally.

Application Insights

The largest application segment remains adult smokers transitioning from combustible cigarettes, accounting for nearly 60% of total market demand in 2025. This dominance is primarily driven by increasing awareness of the health risks associated with traditional smoking and the positioning of e-cigarettes as reduced-risk alternatives. Government-backed smoking cessation programs and public health campaigns in developed regions are further accelerating adoption within this segment. The leading segment growth is supported by nicotine salt formulations that closely mimic the nicotine delivery of conventional cigarettes, enhancing user satisfaction and switching rates. Recreational usage among young adults is expanding rapidly, particularly in urban environments where lifestyle-driven consumption and flavor diversity play a significant role. Additionally, emerging applications such as controlled nicotine therapy and medically supervised harm-reduction programs are gaining traction in regulated markets, further broadening the application scope of e-cigarettes. This diversification of use cases is expected to sustain long-term demand growth.

Distribution Channel Insights

Specialty vape shops remain a dominant distribution channel, contributing a significant share of global sales due to their ability to provide expert guidance, product demonstrations, and a wide range of device and flavor options. The leading segment strength is driven by personalized customer experience and brand engagement, which are critical for consumer retention in a highly competitive market. However, online retail is rapidly emerging as the fastest-growing channel and is expected to account for over one-third of global sales by 2031. The growth of this segment is driven by convenience, wider product availability, competitive pricing, and the rise of direct-to-consumer business models. E-commerce platforms also enable subscription-based services for e-liquids and accessories, enhancing recurring revenue streams for manufacturers. Convenience stores and supermarkets are expanding their presence in regulated markets, increasing accessibility for mainstream consumers, while traditional tobacco retail outlets continue to cater to legacy users transitioning to vaping products. The overall distribution landscape is increasingly digital-first, with omnichannel strategies becoming critical for market players.

End User & Age Group Insights

Adult smokers transitioning to reduced-risk products constitute the largest end-user segment globally, supported by strong demand for smoking alternatives and increasing regulatory recognition of harm-reduction strategies. The leading segment growth is driven by higher disposable income among adult consumers and their willingness to invest in premium vaping devices for long-term use. The 18–35 age group dominates overall consumption patterns, driven by lifestyle-oriented adoption, strong preference for flavored products, and high engagement with digital marketing channels. This demographic is also more receptive to disposable and pod-based systems, further accelerating market expansion. The 31–50 age group contributes significantly to premium product demand, favoring advanced devices with enhanced performance and customization features. Older consumers, particularly those above 50, show a preference for regulated nicotine replacement solutions and simpler device formats. Increasing adoption among first-time users, especially in emerging markets, continues to expand the global consumer base and supports sustained market growth.

Explore more data points, trends and opportunities Download Free Sample Report

E-Cigarette Market Segmentations

By Product Type

- Disposable E-Cigarettes

- Rechargeable E-Cigarettes

- Modular / Advanced Personal Vaporizers

- Hybrid Nicotine Delivery Devices

By Nicotine Type

- Nicotine-Based E-Liquids

- Nicotine-Free E-Liquids

By Flavor Type

- Tobacco Flavors

- Menthol Flavors

- Fruit & Candy Flavors

- Beverage & Dessert Flavors

- Others (Herbal, Hybrid Blends)

By Distribution Channel

- Online Retail / E-Commerce

- Specialty Vape Shops

- Convenience Stores

- Supermarkets & Hypermarkets

- Tobacco Retail Stores

By End User

- Adult Smokers (Transition Segment)

- Young Adult Consumers (18–35 Years)

- Recreational Users

- Smoking Cessation Users

Regional Insights

North America

North America accounts for approximately 38% of the global market share in 2025, making it the largest regional market, with the United States as the dominant contributor. The region’s growth is primarily driven by high awareness of smoking-related health risks, early adoption of vaping as a harm-reduction alternative, and a well-established retail and online distribution infrastructure. The presence of major industry players and continuous product innovation further strengthens market expansion. Additionally, favorable consumer acceptance of nicotine salt-based products and strong demand for flavored variants contribute to sustained growth. Regulatory frameworks, although stringent, provide clarity that supports structured market development.

Europe

Europe holds around 27% share of the global market, led by key countries such as the United Kingdom, Germany, and France. The region’s growth is strongly supported by public health policies that recognize vaping as a smoking cessation tool, particularly in the UK. High consumer awareness, widespread availability of regulated products, and increasing preference for eco-friendly and refillable devices are key drivers. Additionally, the presence of standardized regulations under the Tobacco Products Directive (TPD) ensures product quality and consumer safety, fostering trust and steady market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a projected CAGR exceeding the global average, driven by China’s dominance in manufacturing and rising consumer demand across Japan, South Korea, and India. China serves as the global production hub, accounting for the majority of e-cigarette exports, while Japan and South Korea are major consumers of advanced nicotine delivery systems. Rapid urbanization, increasing disposable income, and growing awareness of smoking alternatives are key regional growth drivers. Additionally, the expanding young adult population and evolving regulatory frameworks in select markets are expected to unlock significant future demand.

Latin America

Latin America is an emerging market, with Brazil and Mexico leading regional demand. Growth in this region is primarily driven by increasing urbanization, rising awareness of vaping products, and gradual regulatory shifts toward controlled legalization. However, stringent restrictions in certain countries continue to limit rapid expansion. Despite these challenges, the growing middle-class population and increasing exposure to global consumer trends are expected to support moderate long-term growth.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth, led by countries such as the UAE and South Africa. Key drivers include increasing legalization of vaping products, high disposable income among consumers in Gulf countries, and growing demand for premium lifestyle products. The region is also benefiting from strong retail expansion and rising tourism-driven demand. In Africa, gradual regulatory developments and increasing awareness of harm-reduction alternatives are supporting early-stage market growth. Although the market remains relatively nascent, improving regulatory clarity and expanding distribution networks are expected to drive future expansion.

Key Players in the E-Cigarette Market

- British American Tobacco

- Philip Morris International

- Imperial Brands

- Japan Tobacco International

- Altria Group

- JUUL Labs

- RELX Technology

- Smoore International

- Innokin Technology

- GeekVape

- Vaporesso

- SMOK (IVPS Technology)

- NJOY

- Voopoo

- Lost Vape