Drylab Photo Printing Market Size

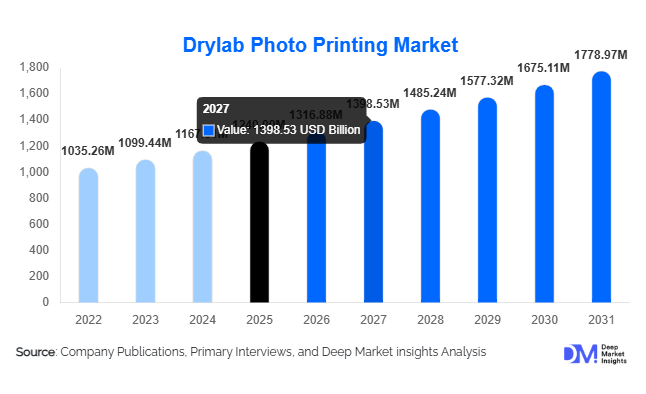

According to Deep Market Insights, the global drylab photo printing market size was valued at USD 1,240 million in 2025 and is projected to grow from USD 1,316.88 million in 2026 to reach USD 1,778.97 million by 2031, expanding at a CAGR of 6.2% during the forecast period (2025–2031). The market growth is primarily driven by the transition from traditional wet-lab photo processing to chemical-free digital printing technologies, increasing demand for instant photo printing in retail and event environments, and the expansion of personalized photo merchandise globally.

Drylab photo printing systems, based on dye-sublimation and inkjet technologies, are gaining widespread adoption due to compact design, lower maintenance costs, faster turnaround times, and compliance with environmental regulations. Unlike conventional silver-halide systems, drylab solutions eliminate water and chemical processing, making them suitable for retail stores, professional studios, healthcare documentation, and government ID printing applications. Growth is further supported by increasing smartphone photography, expansion of retail photo kiosks, and rising demand from emerging markets in the Asia-Pacific and Latin America.

Key Market Insights

- Dye-sublimation technology dominates, accounting for over 52% of the global market in 2025 due to superior color gradation and durability.

- Professional standalone printers lead the product segment, contributing approximately 46% of total revenue.

- North America holds the largest regional share (32%), driven by strong retail kiosk penetration and event photography demand.

- Asia-Pacific is the fastest-growing region, registering nearly 7.5% CAGR, led by China, Japan, and India.

- Professional photo studios remain the largest end-use segment, accounting for about 34% of global demand.

- The top five companies collectively hold nearly 58% market share, indicating moderate consolidation.

What are the latest trends in the drylab photo printing market?

Shift Toward Eco-Friendly and Chemical-Free Printing

Environmental regulations across North America and Europe are accelerating the replacement of wet-lab systems with dry-lab technologies. Businesses are increasingly prioritizing chemical-free operations to comply with wastewater and hazardous disposal standards. This trend is particularly strong in Germany, the U.K., the U.S., and Japan, where sustainability mandates influence equipment procurement decisions. Manufacturers are marketing energy-efficient printers and recyclable consumables to align with ESG requirements. Eco-certifications and green labeling are becoming important differentiators in public and institutional tenders.

Integration of Cloud Connectivity and Mobile Printing

Cloud-enabled drylab systems are transforming consumer engagement. Wi-Fi-enabled printers allow customers to print directly from smartphones, social media platforms, and cloud storage applications. AI-powered color correction and automated image optimization tools are being embedded into newer models, improving print consistency and reducing manual intervention. Retailers are also integrating self-service kiosks with mobile apps, enabling seamless photo uploads and instant printing, especially in malls and tourist destinations. This technology-driven evolution is strongly appealing to younger demographics and event-based photography businesses.

What are the key drivers in the drylab photo printing market?

Rising Demand for Instant Photo Services

Event photography, weddings, exhibitions, and tourist attractions increasingly require immediate, high-quality prints. Drylab printers provide prints within seconds without chemical processing, making them ideal for on-site operations. Growing event management industries in India, Southeast Asia, and the Middle East are significantly contributing to equipment demand.

Growth in Personalized Photo Merchandise

The expansion of customized photo products such as photobooks, greeting cards, and framed prints is driving medium- and large-format drylab printer adoption. Commercial printers rely on these systems for short-run, high-margin customized orders. Rising gifting culture and e-commerce-based personalization platforms are further stimulating demand.

What are the restraints for the global market?

High Initial Equipment Cost

Professional and industrial drylab printers require significant upfront investment, which can restrict adoption among small studios and independent retailers, particularly in developing regions.

Competition from Digital-Only Media

Increasing reliance on digital photo storage and social media sharing reduces overall print volumes in mature markets, particularly among younger consumers who prefer digital archiving.

What are the key opportunities in the drylab photo printing industry?

Expansion in Emerging Retail Kiosk Networks

Rapid urbanization in the Asia-Pacific and Latin America is driving mall-based retail expansion. Compact desktop drylab printers can be deployed in telecom stores, supermarkets, and tourist hubs, creating recurring consumable revenue streams for OEMs.

Government & ID Documentation Printing Programs

Standardized passport and visa photo regulations across multiple countries create stable institutional demand. Government procurement of secure, high-resolution printing systems presents long-term growth potential for equipment manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1240 Million |

| Market Size in 2026 | USD 1316.88 Million |

| Market Size in 2031 | USD 1778.97 Million |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Professional standalone drylab printers dominate the global market, accounting for approximately 46% of total revenue in 2025. Their leadership is primarily driven by strong demand from commercial photo studios, retail print shops, and event-based photography businesses that require high throughput, consistent image quality, and operational durability. These systems typically support larger paper rolls, automated cutting, color calibration tools, and integrated workflow software, making them ideal for medium- to high-volume printing environments. The replacement cycle from traditional wet-lab systems to compact standalone dry-lab printers has further accelerated adoption, particularly in North America and Europe where chemical disposal compliance costs are high.

Desktop drylab printers are gaining traction among small studios, passport photo centers, and kiosk operators due to their compact footprint and lower capital expenditure requirements. Their demand is especially strong in emerging markets where entrepreneurs operate small-format print businesses. Meanwhile, industrial high-capacity drylab systems serve commercial labs, corporate printing facilities, and photobook manufacturers, benefiting from growing demand for personalized photo merchandise and bulk short-run printing orders.

Technology Insights

Dye-sublimation technology leads the market with nearly 52% share in 2025, driven by its ability to produce smooth color gradation, high durability, water resistance, and fade-resistant prints. Its reliability and low maintenance requirements make it highly suitable for event photography, retail kiosks, and instant photo booths. The predictable cost-per-print model associated with dye-sublimation consumables also enhances operational planning for commercial users.

Inkjet-based drylab systems are expanding steadily, supported by advancements in pigment-based inks, micro-precision printheads, and enhanced color management software. These systems are increasingly preferred for medium- and large-format applications, particularly in commercial printing and customized merchandise production. Thermal transfer systems, though niche, remain relevant in government ID printing, healthcare documentation, and security-based photo applications where durability and compliance standards are critical drivers.

End-Use Industry Insights

Professional photo studios and photographers account for approximately 34% of total global demand, making them the largest end-use segment. The segment’s leadership is driven by sustained demand for wedding photography, portrait sessions, school photography contracts, and event coverage services. Increasing consumer preference for physical photo albums and framed prints continues to support studio-level investments in advanced drylab systems.

Retail photo kiosks and print shops represent the fastest-growing end-use category, projected to expand at nearly 7.5% CAGR through 2031. Growth is fueled by mall expansion, tourism recovery, and the rising popularity of instant souvenir photo services. Government agencies, healthcare institutions, and educational organizations are increasingly deploying drylab printers for passport photos, national ID documentation, visa processing, medical imaging outputs, and institutional ID cards. The shift toward standardized digital documentation globally further strengthens institutional demand.

Distribution Channel Insights

Direct OEM sales dominate the market with approximately 58% share, particularly in institutional and commercial segments. Large studios, government departments, and corporate buyers prefer direct procurement due to bundled service contracts, consumable agreements, warranty extensions, and customized installation support. This channel also allows manufacturers to maintain stronger customer relationships and generate recurring revenue through consumables.

Specialized imaging equipment dealers play a crucial role in regional distribution, particularly in Europe, Japan, and parts of Southeast Asia where localized technical support is valued. E-commerce platforms are emerging as a growing channel for compact and entry-level printers, particularly in North America and India, where small businesses and entrepreneurs increasingly rely on online procurement for cost efficiency.

Explore more data points, trends and opportunities Download Free Sample Report

Drylab Photo Printing Market Segmentations

By Product Type

- Desktop Drylab Photo Printers

- Professional Standalone Drylab Printers

- Industrial High-Capacity Drylab Printing Systems

By Printing Technology

- Dye-Sublimation Drylab Printing

- Inkjet-Based Drylab Printing

- Thermal Transfer Drylab Printing

By Print Format Size

- Small Format (Up to 6”x8”)

- Medium Format (8”x10” to 12”x18”)

- Large Format (Above 12”x18”)

By Distribution Channel

- Direct OEM Sales

- Specialized Imaging Equipment Dealers

- E-commerce / Online Platforms

By End-Use Industry

- Professional Photo Studios & Photographers

- Retail Photo Kiosks & Print Shops

- Event & Wedding Photography Services

- Government & Security Agencies

- Healthcare & Institutional Printing

- Commercial & Corporate Printing

Regional Insights

North America

North America accounts for approximately 32% of the global market in 2025, with the United States contributing nearly 25% of global revenue. Regional growth is driven by strong event photography culture, high consumer spending on personalized merchandise, and extensive retail kiosk penetration in shopping malls and tourist destinations. Strict environmental regulations encouraging the replacement of wet-lab systems with chemical-free alternatives further support adoption. In Canada, growth is supported by institutional documentation printing and educational photography contracts. Mature digital infrastructure and high disposable income levels reinforce stable demand across the region.

Europe

Europe holds roughly 28% market share, led by Germany, the United Kingdom, France, and Italy. Regional growth is strongly influenced by stringent environmental policies that discourage chemical-based photo processing. The European Union’s sustainability mandates have accelerated the shift toward drylab systems in commercial labs. Additionally, a well-established professional photography industry and strong demand for premium photo products support market stability. Growth in Eastern Europe is gradually increasing due to rising small business formation and retail modernization.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at nearly 7.5% CAGR. China and Japan together account for over 20% of global revenue, supported by strong domestic manufacturing capabilities and widespread retail photo services. China’s growth is fueled by expanding urban retail centers and rising demand for personalized photo gifts. Japan maintains stable demand due to advanced imaging technology adoption and institutional documentation requirements. India is the fastest-growing country in the region, registering close to 9% CAGR, driven by rapid growth in wedding photography, expanding middle-class consumption, and increasing mall-based retail kiosk installations.

Latin America

Brazil and Mexico dominate regional demand, supported by expanding urban retail networks, growing tourism activity, and rising event-based photography services. Improving retail infrastructure and increasing smartphone penetration are encouraging instant photo printing adoption. Although the region currently represents a smaller share of global revenue, gradual economic stabilization and rising entrepreneurial activity in small-format photo studios are expected to drive steady growth.

Middle East & Africa

The UAE and Saudi Arabia lead demand in the Middle East, supported by luxury event industries, tourism growth, and high per-capita income levels. Increasing mall developments and entertainment venues create favorable conditions for retail kiosk expansion. In Africa, South Africa represents a key demand hub for studio photography, government documentation printing, and educational ID systems. Regional growth is further supported by expanding tourism and gradual modernization of documentation processes across selected African economies.

Key Players in the Drylab Photo Printing Market

- Fujifilm Holdings Corporation

- Canon Inc.

- Seiko Epson Corporation

- HiTi Digital Inc.

- Mitsubishi Electric Corporation

- DNP Imagingcomm America Corporation

- Sony Corporation

- HP Inc.

- Agfa-Gevaert Group

- Shinko Electric Co., Ltd.

- Citizen Systems Japan Co., Ltd.

- Kodak Alaris

- Sinfonia Technology Co., Ltd.

- Noritsu Koki Co., Ltd.

- Primera Technology, Inc.