Drawn Textured Yarn (DTY) Market Size

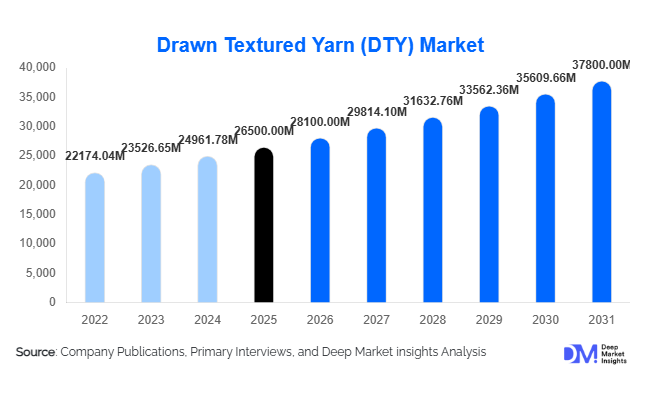

According to Deep Market Insights, the global Drawn Textured Yarn (DTY) market size was valued at USD 26,500 million in 2025 and is projected to grow from USD 28,100 million in 2026 to reach USD 37,800 million by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). The DTY market growth is primarily driven by increasing demand for cost-effective synthetic textiles, rapid expansion of the global apparel industry, and rising adoption of performance fabrics across sportswear and technical textile applications.

Key Market Insights

- Polyester-based DTY dominates the market, accounting for over 70% share due to its affordability, durability, and versatility in textile applications.

- Asia-Pacific leads global production and consumption, supported by strong textile manufacturing hubs in China, India, and Southeast Asia.

- Demand for sustainable and recycled DTY is increasing, driven by environmental regulations and brand commitments to circular textiles.

- Apparel applications account for the largest share, fueled by fast fashion and rising global clothing consumption.

- Technical textiles are emerging as a high-growth segment, especially in automotive and industrial applications.

- Technological advancements in texturing processes are improving yarn quality, efficiency, and performance characteristics.

What are the latest trends in the Drawn Textured Yarn (DTY) market?

Shift Toward Sustainable and Recycled Yarn Production

The DTY market is witnessing a significant transition toward sustainability, with increasing adoption of recycled polyester yarns derived from PET bottles and textile waste. Manufacturers are investing in closed-loop recycling systems and eco-friendly production technologies to meet stringent environmental standards. Global apparel brands are actively sourcing recycled DTY to align with sustainability goals, leading to a structural shift in procurement strategies. Additionally, certifications such as Global Recycled Standard (GRS) are becoming essential, influencing purchasing decisions across the value chain.

Rising Demand for Microfilament and Performance Yarns

There is growing demand for microfilament DTY, which offers superior softness, lightweight properties, and enhanced moisture management. This trend is particularly strong in sportswear and athleisure segments, where performance and comfort are critical. Innovations in yarn engineering are enabling manufacturers to produce DTY with specialized properties such as anti-bacterial finishes, UV resistance, and high elasticity. These advancements are expanding DTY applications beyond traditional textiles into high-performance and technical domains.

What are the key drivers in the Drawn Textured Yarn (DTY) market?

Expansion of the Global Apparel and Fast Fashion Industry

The rapid growth of the apparel sector, particularly fast fashion, is a major driver of DTY demand. Brands are focusing on quick turnaround times and cost efficiency, making DTY an ideal choice due to its affordability and adaptability. Increasing disposable income in emerging economies is further boosting clothing consumption, directly impacting DTY market growth.

Growth of Athleisure and Performance Wear

The rising popularity of athleisure and activewear is driving demand for stretchable and breathable fabrics made from DTY. Consumers are increasingly prioritizing comfort and functionality, leading to higher adoption of DTY in sportswear and fitness apparel. This trend is particularly prominent in North America and Europe.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fluctuations in the prices of key raw materials such as purified terephthalic acid (PTA) and monoethylene glycol (MEG) significantly impact DTY production costs. These variations create pricing instability and margin pressures for manufacturers, especially smaller players.

Environmental Concerns Related to Synthetic Fibers

Growing concerns over microplastic pollution and the environmental impact of synthetic fibers pose challenges to market growth. Increasing regulatory scrutiny and consumer preference for natural or sustainable alternatives may limit the expansion of conventional DTY products.

What are the key opportunities in the Drawn Textured Yarn (DTY) industry?

Expansion into Technical and Industrial Textiles

DTY is increasingly being used in technical applications such as automotive fabrics, geotextiles, and industrial materials. The growing demand for durable and high-performance textiles presents significant opportunities for manufacturers to diversify their product portfolios and tap into high-margin segments.

Emerging Manufacturing Hubs in Southeast Asia

Countries such as Vietnam, Bangladesh, and Indonesia are becoming key textile manufacturing centers due to lower labor costs and favorable government policies. This shift provides opportunities for DTY producers to expand production capacity and establish strategic partnerships in these regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 26500 Million |

| Market Size in 2026 | USD 28100 Million |

| Market Size in 2031 | USD 37800 Million |

| CAGR | 6.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Polyester DTY continues to dominate the global market, accounting for approximately 72% of the total market share in 2025. This leadership is primarily driven by its superior cost efficiency, ease of large-scale production, and versatility across a wide range of textile applications. Polyester DTY benefits from strong backward integration with petrochemical feedstocks, ensuring a consistent supply and competitive pricing. Additionally, its properties, such as wrinkle resistance, durability, and adaptability to various texturing processes, make it the preferred choice for mass-market apparel and home textiles. Nylon DTY, while occupying a smaller share, is gaining traction in high-performance applications such as sportswear and industrial fabrics due to its higher strength, elasticity, and abrasion resistance. Meanwhile, bio-based and recycled DTY segments are emerging rapidly, supported by stringent environmental regulations and brand-level sustainability commitments. The increasing adoption of recycled polyester DTY is expected to significantly reshape the product mix over the forecast period, as manufacturers invest in circular production technologies and eco-friendly innovations.

Application Insights

Apparel applications remain the largest segment in the DTY market, contributing approximately 58% of total demand in 2025. This dominance is driven by the rapid expansion of fast fashion, increasing global clothing consumption, and the need for affordable yet high-quality fabrics. DTY’s ability to provide stretch, softness, and aesthetic appeal makes it highly suitable for knitted and woven garments. Home textiles, including curtains, upholstery, and carpets, represent a stable and consistent demand segment, supported by urbanization, rising disposable incomes, and evolving interior design trends. Industrial textiles are emerging as a high-growth application area, particularly in automotive interiors, geotextiles, and infrastructure-related fabrics, where durability, strength, and performance are critical. The leading driver across applications is the growing preference for synthetic fibers that offer cost advantages and functional benefits over natural alternatives, alongside the increasing diversification of DTY into technical and performance-based applications.

Distribution Channel Insights

Direct B2B sales dominate the DTY market, forming the backbone of the distribution ecosystem. Manufacturers primarily supply DTY directly to textile mills and fabric producers through long-term contracts, ensuring stable demand and predictable revenue streams. This channel is leading due to its efficiency in handling bulk volumes and maintaining quality consistency across large production cycles. Textile processors and mills play a pivotal intermediary role, converting DTY into finished fabrics and ensuring continuous downstream demand. Export traders and merchants are particularly significant in the Asia-Pacific region, where large-scale production is oriented toward global exports. These intermediaries help bridge supply-demand gaps across regions and facilitate international trade flows. Increasing digitalization in procurement and supply chain management is further enhancing transparency, reducing transaction costs, and enabling real-time pricing mechanisms, thereby strengthening the overall efficiency of DTY distribution networks.

End-Use Industry Insights

The fashion and apparel industry remains the largest end-use segment, accounting for approximately 55% of global DTY demand. This leadership is driven by high consumption volumes, rapid product turnover, and the global expansion of fast fashion brands. The segment benefits from DTY’s adaptability to various fabric types and its cost-effectiveness, making it a preferred material for large-scale garment production. The sportswear and activewear segment is the fastest-growing end-use category, with a CAGR exceeding 7.5%, fueled by increasing health consciousness, rising participation in fitness activities, and growing demand for performance-oriented fabrics. Home furnishing and automotive industries also contribute significantly, supported by urban housing growth and advancements in vehicle interior design. A key driver across end-use industries is the increasing demand for functional textiles that combine comfort, durability, and aesthetic appeal, along with the emergence of technical textiles in specialized applications.

Explore more data points, trends and opportunities Download Free Sample Report

Drawn Textured Yarn (DTY) Market Segmentations

By Product Type

- Polyester DTY

- Nylon (Polyamide) DTY

- Polypropylene DTY

- Bio-based / Recycled DTY

By Application

- Apparel

- Home Textiles

- Industrial Textiles

By Distribution Channel

- Direct B2B Sales

- Textile Mills & Processors

- Export Traders / Merchants

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global DTY market, accounting for approximately 62% of the total market share in 2025. China leads with around 35% of global demand, supported by its extensive textile manufacturing infrastructure, integrated supply chains, and large domestic consumption. India is another key growth market, driven by government initiatives such as textile production-linked incentives, increasing export competitiveness, and a rapidly expanding domestic apparel market. Southeast Asian countries, including Vietnam and Bangladesh, are emerging as high-growth regions due to shifting global supply chains, lower labor costs, and favorable trade agreements. The primary driver of regional growth is the concentration of textile manufacturing hubs, coupled with strong export-oriented production and continuous investments in capacity expansion.

North America

North America holds approximately 12% of the global DTY market share, with the United States being the primary contributor. The region’s demand is driven by high consumption of performance textiles, particularly in sportswear, athleisure, and industrial applications. The presence of advanced textile technologies and a strong focus on innovation further support market growth. Additionally, increasing demand for sustainable and recycled textiles is influencing DTY consumption patterns. The key driver in this region is the growing preference for high-performance and functional fabrics, along with rising investments in technical textile applications.

Europe

Europe accounts for around 10% of the global DTY market, with major contributions from Germany, Italy, and Turkey. The region is characterized by a strong emphasis on sustainability, high-quality textile production, and stringent environmental regulations. Demand for recycled and eco-friendly DTY is particularly strong, driven by consumer awareness and regulatory frameworks. Turkey serves as a major textile manufacturing hub within Europe, supporting regional supply chains. The leading growth driver in Europe is the increasing adoption of sustainable textiles and premium fabric production, which aligns with evolving consumer preferences and regulatory mandates.

Latin America

Latin America, led by Brazil and Mexico, represents a moderate but steadily growing DTY market. The region’s growth is supported by expanding domestic apparel manufacturing, rising middle-class consumption, and gradual integration into global textile supply chains. Brazil’s large consumer base and Mexico’s proximity to North American markets provide strategic advantages. The key driver for regional growth is the increasing localization of textile production and rising domestic demand for affordable apparel, which is boosting DTY consumption.

Middle East & Africa

The Middle East & Africa region is emerging as a promising growth market for DTY, driven by increasing investments in textile manufacturing and industrial diversification efforts. Countries such as Egypt and the UAE are investing in textile infrastructure to reduce import dependency and enhance export capabilities. Urbanization, population growth, and rising disposable incomes are further supporting demand for textiles and apparel. The primary driver in this region is the expansion of local manufacturing capabilities combined with government initiatives aimed at developing the textile sector as part of broader economic diversification strategies.

Key Players in the Drawn Textured Yarn (DTY) Market

- Reliance Industries Limited

- Indorama Ventures

- Tongkun Group

- Zhejiang Hengyi Group

- Shenghong Group

- Far Eastern New Century

- Alpek S.A.B. de C.V.

- Toray Industries

- Hyosung Corporation

- Jiangsu Sanfangxiang Group

- Billion Industrial Holdings

- Nan Ya Plastics Corporation

- Sinopec Yizheng Chemical Fibre

- Rongsheng Petrochemical

- Formosa Plastics Corporation