Doors Market Size

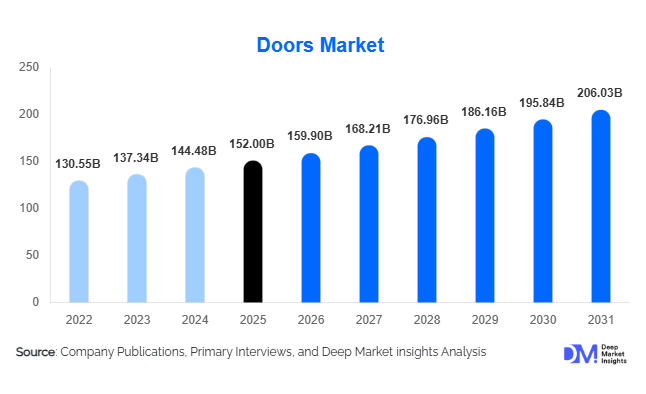

According to Deep Market Insights, the global doors market size was valued at USD 152 billion in 2025 and is projected to grow from USD 159.90 billion in 2026 to reach USD 206.03 billion by 2031, expanding at a CAGR of 5.2% during the forecast period (2026–2031). The growth of the doors market is driven by expanding global construction activity, rising residential housing demand, and the increasing adoption of energy-efficient and technologically advanced entrance solutions.

Doors play a critical role in residential, commercial, and industrial buildings by providing security, thermal insulation, privacy, and aesthetic value. With rapid urbanization and infrastructure development, particularly across emerging economies in the Asia-Pacific and the Middle East, the demand for high-quality door systems is rising steadily. The market is also witnessing a transition toward innovative materials such as fiberglass composites, uPVC, insulated steel panels, and hybrid door systems designed to improve durability and energy efficiency.

Another important growth factor is the rising integration of automation and smart access technologies. Automated sliding doors, biometric entry systems, and sensor-based commercial doors are increasingly used in airports, hospitals, retail malls, and office buildings. In residential environments, smart locks and IoT-enabled access systems are transforming conventional doors into connected home security devices. With increasing emphasis on sustainable construction, fire safety compliance, and architectural design trends, the doors market is expected to maintain steady expansion across both developed and emerging economies.

Key Market Insights

- Interior doors represent the largest product segment, accounting for nearly 46% of the global doors market due to high usage in residential construction.

- Asia-Pacific dominates the market, holding approximately 37% market share in 2025, supported by large-scale construction activity in China and India.

- Residential construction is the largest end-use sector, contributing around 57% of total door demand globally.

- Wood remains the most widely used material, representing roughly 38% of the global doors market.

- Automated and smart doors are among the fastest-growing segments, driven by demand from commercial buildings and smart homes.

- Technological advancements such as IoT-enabled access systems and biometric locks are transforming traditional door products into smart building components.

What are the latest trends in the doors market?

Rising Adoption of Smart and Automated Door Systems

The integration of smart technologies into building infrastructure is reshaping the global doors market. Automated sliding doors, sensor-activated entrances, and biometric access control systems are becoming standard in modern commercial facilities such as airports, hospitals, office complexes, and retail malls. These systems improve accessibility, safety, and operational efficiency by enabling touchless entry and advanced monitoring capabilities.

In residential applications, smart door locks and remote access solutions connected to smartphones and home automation platforms are becoming increasingly popular. Consumers are showing strong interest in doors integrated with digital security systems that allow remote monitoring, real-time alerts, and keyless access. This trend is particularly strong in North America and Europe, where smart home adoption is rapidly increasing.

Growing Demand for Energy-Efficient and Sustainable Doors

Energy efficiency has emerged as a major design requirement in the construction sector, leading to increased adoption of insulated doors and thermally efficient materials. Fiberglass composite doors, insulated steel doors, and multi-layer wooden doors are designed to minimize heat transfer and improve building energy performance.

Government regulations and green building certifications such as LEED and BREEAM are encouraging the use of energy-efficient construction materials. As a result, manufacturers are investing in sustainable production methods, recycled materials, and environmentally friendly coatings to meet evolving regulatory requirements and consumer expectations.

What are the key drivers in the doors market?

Rapid Growth in Global Construction Activities

The expansion of the global construction industry is one of the primary drivers of the doors market. Residential housing development, commercial real estate expansion, and infrastructure projects such as airports, metro stations, and hospitals require significant volumes of doors for both interior and exterior applications. Rapid urbanization in developing economies such as India, Indonesia, and Vietnam is generating strong demand for affordable housing projects, which directly increases door installations.

Large infrastructure investments in emerging economies are also contributing to market growth. Government housing programs, smart city initiatives, and urban infrastructure modernization projects are increasing procurement volumes for building materials, including door systems.

Increasing Demand for Home Renovation and Remodeling

Renovation and remodeling activities represent a major demand driver for doors in developed markets such as the United States, Canada, Germany, and the United Kingdom. Aging residential properties often require replacement of interior doors, security doors, and insulated entry doors to improve aesthetics, energy efficiency, and home security.

Homeowners are increasingly investing in modern interior design upgrades, which include customized wooden doors, glass panel doors, and contemporary sliding doors. The growth of DIY home improvement culture and retail building material stores is also boosting door replacement demand.

What are the restraints for the global market?

Fluctuating Raw Material Prices

The manufacturing of doors relies heavily on raw materials such as timber, steel, aluminum, glass, and PVC. Price volatility in these materials can significantly impact manufacturing costs and profit margins for door manufacturers. Global supply chain disruptions and fluctuations in timber availability often create pricing instability in the industry.

Highly Fragmented Market Structure

The global doors market remains highly fragmented, with thousands of small regional manufacturers competing alongside large multinational companies. Local manufacturers often compete aggressively on price, making it difficult for premium brands to maintain margins. This intense competition can slow down the adoption of advanced door technologies in price-sensitive markets.

What are the key opportunities in the doors industry?

Expansion of Smart Buildings and Automated Infrastructure

The growth of smart buildings is creating new opportunities for door manufacturers to develop technologically advanced products. Commercial buildings increasingly require automated door systems integrated with security cameras, biometric authentication, and centralized access control systems. Airports, healthcare facilities, and corporate offices are particularly strong adopters of these technologies.

Rising Housing Demand in Emerging Economies

Emerging economies in Asia, Africa, and Latin America are witnessing rapid urbanization and growing middle-class populations. Government housing initiatives and affordable housing projects are generating large-scale demand for cost-effective door systems. Manufacturers that establish strong distribution networks and localized production facilities in these markets are expected to benefit significantly.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 152 Billion |

| Market Size in 2026 | USD 159.90 Billion |

| Market Size in 2031 | USD 206.03 Billion |

| CAGR | 5.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Interior doors dominate the global doors market, accounting for nearly 46% of total demand in 2025. The widespread use of interior doors in residential buildings is the primary reason for this segment’s dominance. Each housing unit typically requires multiple interior doors for bedrooms, bathrooms, and utility areas, resulting in high unit volumes. Exterior doors represent another significant segment, particularly in residential and commercial buildings where security and durability are essential. Patio doors and sliding glass doors are gaining popularity due to modern architectural preferences for open living spaces and natural lighting. Industrial doors such as roll-up doors and high-speed doors are widely used in warehouses and logistics facilities, supported by the rapid growth of global e-commerce infrastructure.

Material Type Insights

Wood doors account for approximately 38% of the global doors market and remain the most widely used material category. Engineered wood doors made from MDF and HDF have gained popularity due to their affordability, durability, and ease of customization. Metal doors, including steel and aluminum doors, are commonly used in commercial and industrial environments where durability and security are critical. Fiberglass and composite doors are among the fastest-growing material segments due to their resistance to moisture, corrosion, and extreme weather conditions. uPVC doors are also gaining traction in residential construction due to their low maintenance requirements and strong thermal insulation properties.

End-Use Industry Insights

The residential construction sector represents the largest end-use industry for doors, accounting for approximately 57% of global demand in 2025. The construction of new housing units, combined with home renovation projects, generates substantial demand for both interior and exterior doors. Commercial buildings such as offices, retail complexes, hotels, and shopping malls represent another major demand segment. These facilities often require specialized doors, including fire-rated doors, automatic sliding doors, and security doors.

Industrial facilities and logistics warehouses are emerging as important growth sectors for the doors market. High-speed roll-up doors and insulated industrial doors are increasingly used in distribution centers to improve operational efficiency and temperature control. The expansion of global e-commerce logistics infrastructure is further strengthening demand for industrial door systems.

Distribution Channel Insights

Door manufacturers distribute products through a combination of direct project sales, building material dealers, and retail home improvement stores. Direct project sales to construction contractors and developers remain the dominant distribution channel in large infrastructure and housing projects. Retail home improvement stores play a major role in the residential renovation market, particularly in North America and Europe. Online sales channels are also growing, as digital platforms allow consumers to compare designs, customize products, and purchase doors directly from manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

Doors Market Segmentations

By Product Type

- Interior Doors

- Exterior Doors

- Sliding & Patio Doors

- Industrial Doors

- Specialty Doors

By Material Type

- Wood Doors

- Metal Doors

- Glass Doors

- Fiberglass & Composite Doors

- uPVC Doors

By Operation Mechanism

- Hinged Doors

- Sliding Doors

- Folding/Bi-Fold Doors

- Revolving Doors

- Automatic & Sensor-Based Doors

By End-Use Industry

- Residential Buildings

- Commercial Buildings

- Industrial Facilities

- Institutional Buildings

By Distribution Channel

- Direct Sales to Builders & Contractors

- Building Material Dealers & Distributors

- Home Improvement Retail Stores

- Online Sales Platforms

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global doors market with approximately 37% market share in 2025. China represents the largest demand center due to massive residential construction activity and large infrastructure projects. India is one of the fastest-growing markets, supported by government housing initiatives and rapid urbanization. Southeast Asian countries such as Indonesia, Vietnam, and Thailand are also witnessing strong demand due to expanding construction industries.

North America

North America holds around 23% of the global doors market, led by the United States. The market is driven primarily by renovation and remodeling activities in the residential sector. The adoption of smart home technologies and automated door systems is also accelerating market growth in the region.

Europe

Europe accounts for approximately 21% of the global market, with Germany, the United Kingdom, France, and Italy representing the largest consumers. Strict building regulations regarding energy efficiency and fire safety are encouraging the adoption of advanced door systems in both residential and commercial buildings.

Latin America

Latin America represents a smaller but steadily growing market, with Brazil and Mexico accounting for the majority of regional demand. Residential construction and urban infrastructure development are the key growth drivers.

Middle East & Africa

The Middle East and Africa region is experiencing growing demand for premium architectural doors, particularly in large infrastructure and real estate development projects in countries such as the United Arab Emirates and Saudi Arabia. Smart city projects and luxury residential developments are boosting demand for high-end door systems.

Key Players in the Doors Market

- Assa Abloy

- Masonite International

- JELD-WEN Holding Inc.

- Andersen Corporation

- Pella Corporation

- Hörmann Group

- Dormakaba Group

- Allegion plc

- Cornerstone Building Brands

- Marvin Windows and Doors

- Simpson Door Company

- Novoferm GmbH

- Boon Edam

- Corinthian Doors

- Therma-Tru Doors