Domestic Refrigerator Market Size

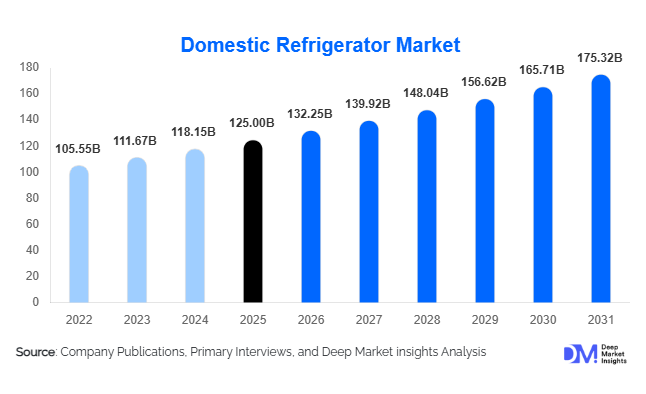

According to Deep Market Insights, the global domestic refrigerator market size was valued at USD 125 billion in 2025 and is projected to grow from USD 132.25 billion in 2026 to reach USD 175.32 billion by 2031, expanding at a CAGR of 5.8% during the forecast period (2026–2031). The domestic refrigerator market growth is primarily driven by rising urbanization, increasing disposable income, and the growing adoption of energy-efficient and smart appliances across both developed and emerging economies.

Key Market Insights

- The Asia-Pacific region dominates the global market, accounting for nearly a 45% share, driven by strong demand in China and India.

- Frost-free refrigerators lead technology adoption, capturing approximately 60% market share due to convenience and low maintenance.

- Mid-range refrigerators (USD 300–700) dominate the pricing segment, with a nearly 45% share, reflecting strong demand from the middle class.

- Residential applications account for over 85% of total demand, making it the core end-use segment globally.

- Offline retail channels remain dominant, contributing around 65% of total sales despite rising e-commerce penetration.

- Smart and IoT-enabled refrigerators are gaining traction, particularly in North America and Europe, driving premium segment growth.

What are the latest trends in the domestic refrigerator market?

Shift Toward Smart and Connected Appliances

The domestic refrigerator market is witnessing a significant shift toward smart appliances integrated with IoT and AI technologies. Modern refrigerators now feature Wi-Fi connectivity, touchscreen interfaces, voice assistant compatibility, and inventory tracking systems. These advancements are enhancing convenience and energy optimization for consumers. The growing adoption of smart home ecosystems is further accelerating this trend, particularly in developed regions such as North America and Europe. Manufacturers are increasingly focusing on software integration and ecosystem compatibility to differentiate their offerings and capture premium market segments.

Rising Demand for Energy-Efficient and Eco-Friendly Refrigerators

Energy efficiency has become a critical purchasing factor, driven by rising electricity costs and stringent environmental regulations. Consumers are increasingly opting for 3-star and above rated refrigerators, with inverter compressor technology gaining widespread adoption. Additionally, the transition toward eco-friendly refrigerants and recyclable materials is shaping product innovation. Governments worldwide are promoting energy-efficient appliances through labeling programs and subsidies, encouraging replacement demand and driving sustainable market growth.

What are the key drivers in the domestic refrigerator market?

Rapid Urbanization and Rising Disposable Income

The expansion of urban populations, particularly in emerging economies such as India, China, and Southeast Asia, is a major driver of refrigerator demand. Increasing disposable incomes are enabling consumers to upgrade from basic models to larger and more feature-rich appliances. The growing middle-class population is also driving demand for mid-range and premium refrigerators, contributing significantly to overall market expansion.

Technological Advancements in Refrigeration

Continuous innovation in refrigeration technology, including frost-free systems, inverter compressors, and smart connectivity, is enhancing product performance and efficiency. These advancements not only improve cooling efficiency but also reduce energy consumption and maintenance requirements. As a result, consumers are increasingly replacing older models with technologically advanced alternatives, boosting market growth.

What are the restraints for the global market?

High Cost of Advanced Refrigerators

The adoption of premium and smart refrigerators is limited by their high upfront cost, particularly in price-sensitive markets. While these appliances offer long-term energy savings and advanced features, their initial investment remains a barrier for many consumers in developing regions.

Volatility in Raw Material Prices

Fluctuations in the prices of key raw materials such as steel, aluminum, and plastics significantly impact manufacturing costs. This volatility affects pricing strategies and profit margins for manufacturers, posing a challenge to market stability and growth.

What are the key opportunities in the domestic refrigerator industry?

Expansion in Emerging Markets

Emerging economies in Asia, Africa, and Latin America present significant growth opportunities due to increasing electrification, urbanization, and rising consumer purchasing power. Governments are also supporting appliance adoption through subsidies and infrastructure development, creating favorable conditions for market expansion. Local manufacturing and cost optimization strategies can further enhance market penetration in these regions.

Integration of Smart Technologies

The growing adoption of smart home ecosystems is creating opportunities for manufacturers to develop connected refrigerators with advanced features such as remote monitoring, AI-based cooling optimization, and voice control. This trend is expected to drive premium segment growth and enhance consumer engagement.

Sustainability and Green Innovation

Increasing environmental awareness is driving demand for eco-friendly refrigerators. Manufacturers investing in energy-efficient designs, natural refrigerants, and recyclable materials can gain a competitive advantage. Circular economy initiatives, including recycling and refurbishment programs, are also emerging as key opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 125 Billion |

| Market Size in 2026 | USD 132.25 Billion |

| Market Size in 2031 | USD 175.32 Billion |

| CAGR | 5.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Double-door refrigerators dominate the market, accounting for approximately 32% of the global share in 2025. Their leadership is driven by the optimal balance they provide between storage capacity and affordability, making them highly attractive to urban and middle-class households globally. The convenience of separating freezer and refrigerator compartments, coupled with modern features like frost-free operation and inverter compressors, enhances their appeal. Single-door refrigerators remain popular in rural areas and entry-level segments, where affordability and smaller household sizes are key drivers. Side-by-side and French door refrigerators are gaining traction in premium markets, particularly in North America, Europe, and Asia-Pacific urban centers, where rising disposable incomes and lifestyle preferences drive demand for high-capacity, feature-rich models. Mini and compact refrigerators are witnessing increased adoption in urban apartments, co-living spaces, and small commercial offices due to space constraints and lifestyle convenience.

Capacity Insights

The 300–500 liters segment leads the market with around 35% share, largely driven by medium-sized households seeking adequate storage for daily needs. This capacity range offers the right balance between affordability and utility, appealing to urban families and dual-income households in APAC and North America. Refrigerators below 200 liters remain significant in emerging markets such as India, Africa, and parts of Latin America, where smaller households and budget-conscious consumers dominate. The above 500 liters segment is experiencing strong growth in developed regions, including Europe and North America, due to premiumization trends, larger family units, and increasing demand for multi-functional, smart refrigerators with additional features such as water dispensers, ice makers, and IoT connectivity.

Technology Insights

Frost-free refrigerators dominate the global market with nearly 60% share, driven by consumer preference for low-maintenance, convenient cooling solutions. The ability to prevent ice buildup and maintain uniform temperature distribution makes frost-free models highly appealing across urban and semi-urban areas. Direct cool technology continues to serve price-sensitive markets in regions like Africa, India, and Latin America due to lower manufacturing costs and energy consumption. Smart and inverter refrigerators are gaining traction globally, driven by energy efficiency, advanced features, and IoT integration. Energy efficiency regulations and consumer demand for reduced electricity bills are major drivers for inverter technology adoption, especially in North America, Europe, and Asia-Pacific.

Price Range Insights

The mid-range segment (USD 300–700) holds the largest market share at approximately 45%, reflecting strong demand from middle-income households in Asia-Pacific, Latin America, and Europe. This segment offers a balance between affordability and desirable features such as frost-free operation, moderate capacity, and energy efficiency. Economy models continue to cater to rural and budget-conscious buyers in Africa, South Asia, and Latin America, while premium refrigerators are expanding rapidly in urban markets worldwide, driven by rising disposable incomes, premiumization trends, and the growing popularity of smart, connected appliances.

Distribution Channel Insights

Offline retail channels dominate with around 65% market share, supported by extensive dealer networks, brand trust, and consumer preference for physical product evaluation, particularly in emerging markets. However, online retail is gaining significant momentum due to convenience, competitive pricing, increasing internet penetration, and the rise of e-commerce platforms in APAC, North America, and Europe. Online channels also allow manufacturers to offer bundled services, extended warranties, and doorstep delivery, driving faster adoption among tech-savvy consumers.

End-Use Insights

The residential segment accounts for over 85% of total demand, driven by increasing household formation, urbanization, and dual-income families seeking reliable and modern refrigeration solutions. The commercial segment, including small retail stores, offices, and foodservice outlets, is growing steadily due to rising demand for compact, specialized refrigeration solutions that support business operations. Expansion in small-scale foodservice, cafes, and convenience stores, particularly in APAC and North America, is expected to further drive commercial segment growth.

Explore more data points, trends and opportunities Download Free Sample Report

Domestic Refrigerator Market Segmentations

By Product Type

- Single Door Refrigerators

- Double Door Refrigerators

- Side-by-Side Refrigerators

- French Door Refrigerators

- Top Freezer Refrigerators

- Bottom Freezer Refrigerators

- Mini/Compact Refrigerators

By Capacity

- Below 200 Liters

- 200–300 Liters

- 300–500 Liters

- Above 500 Liters

By Technology

- Direct Cool Refrigerators

- Frost-Free Refrigerators

- Inverter Refrigerators

- Smart/IoT-Enabled Refrigerators

By Distribution Channel

- Offline Retail

- Online Retail

By End-Use

- Residential

- Commercial

Regional Insights

Asia-Pacific

Asia-Pacific leads the global market with approximately 45% share in 2025. China alone accounts for nearly 25% of global demand, driven by large-scale manufacturing capabilities, urban population growth, and strong domestic consumption. India is one of the fastest-growing markets, supported by rising electrification, increasing urban household formation, government initiatives promoting appliance adoption, and affordable financing options. Southeast Asian countries such as Indonesia, Thailand, and Vietnam are also experiencing rising demand due to growing middle-class incomes and rapid urbanization. Key growth drivers include increasing consumer awareness of energy-efficient appliances, expanding e-commerce platforms, and premiumization trends in urban centers.

North America

North America holds around 20% of the global market, with the United States being the primary contributor. Market growth is driven by high replacement demand and strong adoption of premium, smart, and energy-efficient refrigerators. Consumers in this region prioritize advanced features such as IoT connectivity, inverter compressors, frost-free operation, and eco-friendly refrigerants. Rising electricity costs, sustainability awareness, and government incentives for energy-efficient appliances further stimulate market adoption. Canada also contributes significantly, with growing urban households and a preference for mid- to high-range refrigerator models.

Europe

Europe accounts for approximately 18% of the global market, with Germany, France, and the UK leading demand. The key growth drivers include stringent energy efficiency regulations, sustainability initiatives, and rising consumer awareness of eco-friendly appliances. Urbanization, premiumization, and increasing household sizes support the adoption of frost-free and smart refrigerators. Additionally, government programs promoting energy-saving appliances are incentivizing replacements of older, inefficient models, further boosting market growth across Western and Northern Europe.

Latin America

Latin America holds about 9% market share, led by Brazil and Mexico. Growth in the region is supported by economic recovery, rising disposable incomes, and expanding middle-class populations. Consumers increasingly prefer mid-range and frost-free refrigerators, while urbanization and the expansion of retail networks drive product penetration. Additionally, government policies promoting energy-efficient appliances and import facilitation for advanced technology refrigerators are contributing to the market expansion in the region.

Middle East & Africa

The Middle East & Africa region accounts for around 8% of the market. Growth is primarily driven by urbanization, infrastructure development, rising household formation, and increasing appliance penetration. In the Middle East, high-income populations in the UAE, Saudi Arabia, and Qatar fuel demand for premium, smart, and large-capacity refrigerators. In Africa, electrification projects, expanding urban middle-class populations, and government subsidies for appliance adoption are driving the fastest growth globally, with the region projected to exhibit a CAGR exceeding 7%. The growing preference for energy-efficient and frost-free models further supports regional market expansion.

Key Players in the Domestic Refrigerator Market

- Whirlpool Corporation

- Samsung Electronics

- LG Electronics

- Haier Group

- Electrolux AB

- Panasonic Corporation

- Hitachi Ltd.

- Bosch (BSH Hausgeräte)

- Sharp Corporation

- Midea Group

- Godrej Appliances

- Toshiba Corporation

- Hisense Group

- Liebherr Group

- Arçelik A.Ş.