Dogs Pet Clothing Market Size

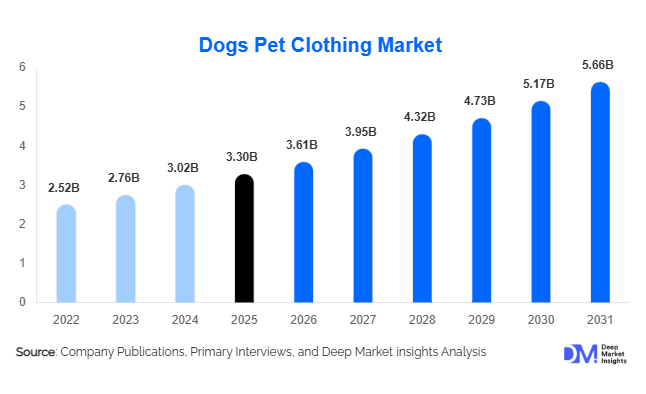

According to Deep Market Insights, the global dogs pet clothing market size was valued at USD 3.3 billion in 2025 and is projected to grow from USD 3.61 billion in 2025 to reach USD 5.66 billion by 2031, expanding at a CAGR of 9.4% during the forecast period (2025–2031). The dogs pet clothing market growth is primarily driven by increasing pet humanization, rising expenditure on premium petcare products, rapid expansion of online pet retail platforms, and growing demand for fashionable as well as functional dog apparel globally.

Key Market Insights

- Pet humanization trends are significantly accelerating premium dog apparel demand, with consumers increasingly treating pets as family members and spending on lifestyle-oriented products.

- Functional dog clothing categories are expanding rapidly, including cooling vests, waterproof jackets, anxiety wraps, and recovery suits designed for health and wellness applications.

- North America dominates the global dogs pet clothing market, supported by high pet ownership rates, premium petcare expenditure, and advanced organized retail infrastructure.

- Asia-Pacific is the fastest-growing regional market, driven by increasing urbanization, rising disposable income, and rapid growth in pet adoption across China, India, and Southeast Asia.

- E-commerce platforms are reshaping purchasing behavior, with online marketplaces and direct-to-consumer brands gaining strong traction globally.

- Sustainable pet fashion is emerging as a major industry trend, with increasing adoption of organic cotton, recycled fibers, and eco-friendly textile materials.

Dogs Pet Clothing Market Trends

Premium and Designer Dog Fashion Gaining Momentum

The dogs pet clothing market is increasingly shifting toward premiumization, with consumers seeking stylish, designer-oriented apparel for companion animals. Luxury dog apparel collections, boutique fashion lines, and customized seasonal wear are becoming mainstream across developed economies. Social media influence, celebrity pet culture, and rising participation of pets in family travel and lifestyle activities are supporting demand for visually appealing clothing products. Premium pet fashion brands are increasingly collaborating with apparel designers and influencers to launch limited-edition collections that appeal to affluent pet owners. Personalized embroidery, breed-specific tailoring, and exclusive event-based clothing are also becoming key differentiators within the premium category.

Functional and Climate-Protective Apparel Expanding Rapidly

Functional dog clothing is becoming one of the fastest-growing categories within the global market. Products such as thermal jackets, waterproof raincoats, UV-protection apparel, anxiety wraps, orthopedic recovery suits, and cooling vests are witnessing increasing demand due to rising awareness regarding pet comfort and health. Consumers are increasingly prioritizing practical utility in addition to aesthetics, particularly in regions with extreme weather conditions. Manufacturers are integrating antimicrobial fabrics, reflective safety materials, moisture-wicking textiles, and ergonomic designs to improve functionality and durability. Smart textiles capable of thermal regulation and enhanced comfort are also emerging as innovation areas within the industry.

Dogs Pet Clothing Market Drivers

Rising Pet Humanization and Companion Animal Spending

The increasing humanization of pets remains one of the primary growth drivers for the dogs pet clothing market. Pet owners globally are increasingly treating dogs as family members, leading to higher spending on discretionary products including fashion apparel, premium accessories, and customized clothing. Millennials and Gen Z consumers are particularly influential in driving expenditure on pet lifestyle products. Urban households with smaller family sizes are increasingly allocating greater disposable income toward premium petcare purchases, supporting long-term market expansion. In developed countries, higher annual spending per pet continues to create strong demand for luxury and seasonal dog apparel categories.

Rapid Expansion of E-Commerce and Social Media Influence

The rapid growth of digital commerce platforms has significantly improved product accessibility and market penetration for dog clothing brands. Consumers increasingly rely on online marketplaces, social media advertisements, influencer recommendations, and direct-to-consumer platforms when purchasing pet apparel. Visual platforms such as Instagram and TikTok have amplified pet fashion trends globally, encouraging repeat purchases and seasonal buying behavior. AI-driven product recommendations, subscription-based apparel boxes, and virtual fitting technologies are further improving consumer engagement and customer retention rates across online sales channels.

Dogs Pet Clothing Market Restraints

Pricing Sensitivity in Emerging Markets

Despite strong growth potential, pricing sensitivity remains a key challenge for the dogs pet clothing market, especially in emerging economies where pet apparel is often considered a non-essential discretionary purchase. Premium products featuring designer branding, technical fabrics, and customized designs are relatively expensive, limiting penetration among middle-income consumers. Inflationary pressures and fluctuations in consumer spending patterns can also impact purchasing behavior within economy and mid-range product categories.

Sizing and Product Standardization Challenges

The absence of universal sizing standards continues to create operational challenges across the industry. Dog breeds vary significantly in body structure, coat type, and mobility requirements, making standardized sizing difficult for manufacturers and retailers. Poor fit and inconsistent product quality can increase return rates, particularly within e-commerce channels. Companies are increasingly investing in breed-specific sizing systems, AI-enabled fit prediction technologies, and customized tailoring solutions to address these challenges and improve customer satisfaction.

Dogs Pet Clothing Market Opportunities

Growth of Sustainable Pet Fashion

Sustainability is emerging as a major opportunity area within the dogs pet clothing market. Consumers are increasingly demanding eco-friendly pet apparel manufactured using recycled fabrics, organic cotton, biodegradable packaging, and ethically sourced textile materials. European and North American consumers are particularly responsive to sustainability-focused branding strategies. Manufacturers investing in environmentally responsible supply chains and low-impact manufacturing processes are expected to gain strong competitive advantages in premium market segments. Sustainable dog fashion collections are also helping brands differentiate themselves within a crowded competitive landscape.

Expansion into Emerging Petcare Markets

Emerging economies across Asia-Pacific, Latin America, and the Middle East present significant untapped opportunities for market participants. Rising disposable income, rapid urbanization, and increasing pet adoption rates are creating favorable conditions for long-term market expansion. Countries such as China, India, Brazil, and the UAE are witnessing strong growth in premium petcare spending. Localized product offerings, affordable pricing strategies, and expansion of online retail infrastructure are expected to accelerate penetration in these developing markets. Companies establishing early brand recognition and regional manufacturing capabilities are likely to benefit substantially from future demand growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.3 Billion |

| Market Size in 2026 | USD 3.61 Billion |

| Market Size in 2031 | USD 5.66 Billion |

| CAGR | 9.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Winter and thermal clothing dominates the global dogs pet clothing market, accounting for approximately 28% of total revenue in 2025. Products such as insulated jackets, sweaters, hoodies, and fleece coats are widely purchased in colder regions including North America, Europe, Japan, and South Korea. Luxury and designer dog apparel is also witnessing rapid expansion, particularly among affluent urban consumers seeking fashionable and customized products for companion animals. Functional clothing categories including waterproof rainwear, anxiety wraps, UV-protection garments, and post-surgery recovery suits are increasingly contributing to overall market growth as consumers prioritize pet wellness and outdoor comfort. Costume and seasonal event apparel, including Halloween and holiday-themed products, continue generating strong seasonal sales across organized retail channels and e-commerce platforms.

Material Type Insights

Polyester and synthetic fabrics represent the leading material category within the dogs pet clothing market, contributing nearly 34% of global revenue. These materials are widely preferred due to their durability, water resistance, flexibility, and cost efficiency. Manufacturers increasingly utilize synthetic blends for outdoor apparel and climate-protective clothing applications. Cotton-based fabrics remain highly popular for casual everyday dog wear due to their breathability and comfort characteristics. Sustainable and organic textiles are emerging as high-growth material segments, supported by increasing consumer awareness regarding environmental sustainability and ethical sourcing practices. Waterproof nylon fabrics are also gaining traction for outdoor and monsoon-focused dog apparel collections.

Distribution Channel Insights

E-commerce marketplaces and direct-to-consumer online platforms dominate the distribution landscape for dog pet clothing products. Online channels account for nearly 31% of global market revenue due to wider product availability, ease of comparison, personalized recommendations, and strong social media integration. Consumers increasingly prefer online shopping for pet apparel because of convenience and access to international brands. Pet specialty stores continue to maintain strong relevance within premium product categories, particularly for customized fittings and high-end designer apparel. Veterinary clinics, grooming centers, and pet spas are also emerging as secondary retail channels for functional dog clothing products including recovery wear and protective garments.

Dog Size Insights

Small breed dogs account for the largest share of the dogs pet clothing market, representing nearly 46% of global demand. Breeds such as French Bulldogs, Pomeranians, Chihuahuas, Shih Tzus, and Dachshunds are highly popular among urban consumers due to apartment-friendly lifestyles. These smaller breeds are also more likely to require weather-protection clothing because of their body size and coat characteristics. Medium-sized dogs continue to represent stable demand for outdoor functional apparel and protective wear. Large and giant breeds contribute comparatively smaller market shares due to lower adoption rates in urban households and limited requirements for fashion-oriented clothing products.

End-Use Insights

Household pet owners remain the dominant end-use segment within the global dogs pet clothing market, accounting for approximately 72% of total revenue generation. Rising pet ownership, emotional attachment toward companion animals, and increasing expenditure on pet wellness products continue driving household demand globally. Pet grooming centers and luxury pet spas are emerging as rapidly expanding commercial end-use channels, increasingly offering seasonal clothing collections and premium accessories as value-added services. Pet boarding facilities, pet hotels, and photography studios are also contributing to recurring demand for themed apparel, event costumes, and climate-protection clothing. Social media-driven pet entertainment and content creation industries are further expanding commercial demand for premium and customized dog apparel products.

Explore more data points, trends and opportunities Download Free Sample Report

Dogs Pet Clothing Market Segmentations

By Product Type

- Everyday Apparel

- Winter & Thermal Clothing

- Rainwear & Outdoor Protection

- Luxury & Fashion Apparel

- Functional & Medical Clothing

- Footwear & Accessories

- Costume & Event Apparel

By Material Type

- Cotton-Based Fabrics

- Polyester & Synthetic Fabrics

- Wool & Fleece Materials

- Nylon & Waterproof Fabrics

- Organic & Sustainable Textiles

- Blended Fabrics

By Price Category

- Economy

- Mid-Range

- Premium

- Luxury

By Distribution Channel

- E-Commerce Platforms

- Pet Specialty Stores

- Supermarkets & Hypermarkets

- Veterinary Clinics & Pet Hospitals

- Brand-Owned Stores

- Direct-to-Consumer Websites

- Subscription-Based Retail

By End User

- Household Pet Owners

- Pet Grooming & Spa Centers

- Pet Boarding & Daycare Facilities

- Pet Photography & Entertainment Industry

- Animal Welfare Organizations

- Professional Breeders

Regional Insights

North America

North America remains the largest regional market for dogs pet clothing, accounting for nearly 41% of global revenue in 2025. The United States dominates regional demand due to high pet ownership rates, advanced organized retail infrastructure, and strong consumer willingness to spend on premium petcare products. Seasonal winter apparel, luxury dog fashion, and functional outdoor wear categories demonstrate particularly strong demand within the U.S. market. Canada also contributes significantly due to colder climatic conditions and increasing expenditure on thermal dog clothing products.

Europe

Europe represents approximately 27% of the global dogs pet clothing market, led by countries such as Germany, the United Kingdom, France, and Italy. European consumers show strong preference for sustainable pet apparel and designer dog fashion collections. Germany and the UK dominate regional sales due to higher pet adoption rates and premium retail penetration. Italy and France remain important markets for luxury dog fashion and boutique pet apparel. Increasing focus on sustainable textiles and eco-friendly manufacturing is further influencing purchasing behavior across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, supported by rapid urbanization, expanding middle-class populations, and rising pet ownership across China, India, Japan, South Korea, and Southeast Asia. China represents the largest regional market due to increasing premium petcare spending and strong growth in online retail sales. Japan and South Korea demonstrate high demand for luxury and functional pet apparel products, while India is emerging as a promising high-growth market driven by increasing disposable income and accelerating urban pet adoption. Social media influence and expanding organized pet retail infrastructure continue supporting regional market expansion.

Latin America

Latin America accounts for nearly 6% of global market revenue, with Brazil emerging as the largest regional market. Rising awareness regarding pet wellness, increasing urban pet ownership, and improving retail accessibility are supporting gradual market growth across the region. Consumers are increasingly adopting affordable winter wear and seasonal clothing products for companion animals. Mexico and Argentina are also witnessing moderate demand growth through expanding e-commerce platforms and organized pet retail channels.

Middle East & Africa

The Middle East & Africa region currently represents a smaller share of the global market but demonstrates strong long-term growth potential. The UAE and Saudi Arabia are witnessing rising demand for luxury dog apparel and premium petcare products due to increasing expatriate populations and high-income consumer groups. South Africa represents an important market within the African region because of rising pet ownership and expanding organized retail infrastructure. Premium imported pet apparel brands are increasingly entering major Middle Eastern urban markets to capitalize on growing luxury petcare spending trends.