Disposable Underarm Sweat Pads Market Size

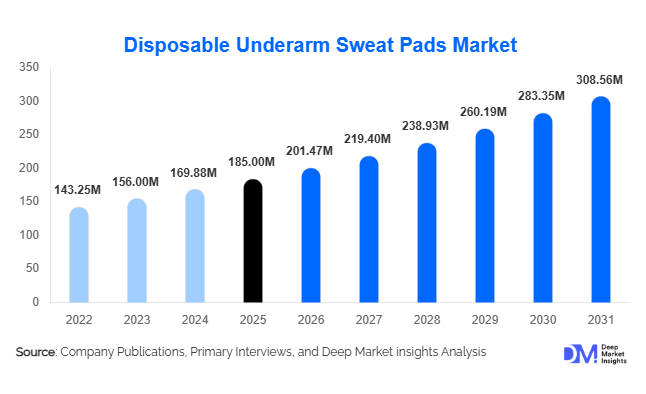

According to Deep Market Insights, the global disposable underarm sweat pads market size was valued at USD 185 million in 2025 and is projected to grow from USD 201.47 million in 2026 to reach USD 308.56 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The market growth is primarily driven by increasing consumer awareness regarding personal hygiene, rising adoption of discreet grooming solutions, and the growing demand for sweat-management products across professional and lifestyle applications. The expansion of e-commerce platforms and improvements in absorbent material technologies are further accelerating product accessibility and adoption globally.

Key Market Insights

- Growing awareness of personal hygiene and grooming is driving demand for discreet sweat management solutions globally.

- Online retail channels are expanding rapidly, enabling broader product accessibility and subscription-based purchase models.

- North America dominates the market due to high awareness levels and strong purchasing power.

- Asia-Pacific is the fastest-growing region, supported by rising urbanization and increasing middle-class populations.

- Sustainable and biodegradable sweat pads are emerging as a key trend among environmentally conscious consumers.

- Technological advancements in absorbent materials such as superabsorbent polymers and breathable fabrics are enhancing product performance.

What are the latest trends in the disposable underarm sweat pads market?

Shift Toward Eco-Friendly and Biodegradable Products

Consumers are increasingly demanding environmentally sustainable hygiene products, leading manufacturers to develop biodegradable and compostable sweat pads. Materials such as bamboo fibers and organic cotton are gaining traction, especially in Europe and North America. Brands are also investing in recyclable packaging and reducing plastic content, aligning with global sustainability goals. This trend is particularly prominent among premium consumers who are willing to pay higher prices for eco-friendly alternatives.

Rise of Direct-to-Consumer and Subscription Models

The growth of e-commerce has transformed distribution strategies in this market. Direct-to-consumer (D2C) models allow brands to establish stronger relationships with customers while reducing dependency on intermediaries. Subscription-based offerings are gaining popularity, ensuring recurring demand and customer retention. Digital marketing and influencer-driven campaigns are further enhancing product visibility and normalizing usage across younger demographics.

What are the key drivers in the disposable underarm sweat pads market?

Increasing Workforce Participation and Professional Grooming Needs

The expanding global workforce, particularly in urban areas, is driving demand for products that enhance comfort and maintain professional appearance. Sweat pads help prevent visible sweat stains, making them highly relevant for individuals in corporate and service sectors. Rising female workforce participation is also contributing significantly to market growth.

Advancements in Absorbent and Skin-Friendly Materials

Technological innovations in materials such as superabsorbent polymers and non-woven fabrics have improved product efficiency and comfort. Modern sweat pads offer enhanced moisture absorption, odor control, and skin compatibility, increasing consumer satisfaction and repeat purchases. Continuous R&D investments are enabling manufacturers to differentiate their offerings in a competitive market.

What are the restraints for the global market?

Low Awareness in Emerging Markets

Despite strong growth potential, awareness of disposable underarm sweat pads remains limited in several developing regions. Consumers often rely on traditional alternatives such as antiperspirants, which can restrict market penetration. Educational marketing and product demonstrations are required to overcome this barrier.

Environmental Concerns Related to Disposable Products

The disposable nature of these products raises sustainability concerns, particularly regarding plastic waste and non-biodegradable materials. Increasing regulatory pressure and consumer preference for eco-friendly solutions may challenge manufacturers relying on conventional materials, necessitating a shift toward sustainable production practices.

What are the key opportunities in the disposable underarm sweat pads industry?

Expansion in Emerging Markets

Emerging economies such as India, China, and Brazil present significant growth opportunities due to rising disposable incomes, urbanization, and increasing awareness of personal hygiene. Market penetration remains relatively low, allowing new entrants to establish a strong brand presence. Localization of products based on climate conditions and consumer preferences can further enhance adoption rates.

Product Innovation and Premiumization

There is substantial potential for innovation in product design and materials. Features such as odor-neutralizing technology, ultra-thin designs, and hypoallergenic adhesives can attract premium consumers. The introduction of eco-friendly variants also provides opportunities for differentiation and higher profit margins, particularly in developed markets.

Product Type Insights

Disposable adhesive underarm pads dominate the global market, accounting for approximately 62% of the total market share in 2025. This leadership is primarily driven by their superior convenience, ease of application, and strong adhesion capabilities that ensure secure placement throughout extended wear durations. These pads are highly versatile and compatible with a wide range of clothing types, including formal, casual, and activewear, making them the preferred choice among working professionals and frequent users. Additionally, advancements in adhesive technologies, such as skin-safe, residue-free formulations, have significantly enhanced consumer confidence and repeat usage.

Garment-integrated sweat pads are gaining traction in the premium segment, particularly in formal and high-value apparel, where maintaining garment longevity is critical. These products are increasingly being adopted by fashion-conscious consumers and professionals who prioritize discretion. Meanwhile, non-adhesive tuck-in variants cater to niche use cases, including occasional users and costume applications, where flexibility and repositioning are required. However, their limited stability compared to adhesive options restricts widespread adoption.

Material Type Insights

Non-woven synthetic fiber pads lead the market with nearly 48% share, primarily due to their cost efficiency, high durability, and superior absorbency performance. These materials enable mass production at lower costs while delivering consistent quality, making them highly suitable for both economy and mid-range product segments. Their ability to incorporate superabsorbent polymers (SAP) further enhances moisture retention, making them ideal for extended usage.

However, bamboo-based and cotton-based pads are emerging as the fastest-growing sub-segments, driven by increasing consumer preference for eco-friendly, biodegradable, and skin-sensitive products. Rising environmental awareness and regulatory pressure, particularly in Europe and North America, are accelerating the shift toward sustainable materials. Manufacturers are increasingly investing in hybrid material technologies that combine synthetic absorbency with natural fiber comfort, enabling them to balance performance with sustainability while catering to premium consumer segments.

Absorbency Level Insights

Medium absorbency pads hold the largest market share at approximately 45%, as they cater to a broad spectrum of consumers across diverse climatic conditions and usage scenarios. This segment benefits from its versatility, offering sufficient protection for daily use without compromising comfort or product thickness. The balanced performance-to-cost ratio makes medium absorbency pads the default choice for most consumers globally.

Light absorbency pads are primarily used by occasional users or in cooler climates where perspiration levels are lower. In contrast, heavy-duty absorbency pads are witnessing increasing demand in high-temperature regions such as the Middle East, Southeast Asia, and parts of Latin America. These variants are also preferred by individuals with higher perspiration levels and in physically demanding environments, contributing to their steady growth.

End-Use Insights

Individual consumers dominate the market with around 78% share, driven by rising awareness of personal hygiene, grooming standards, and the need for discreet sweat management solutions. Urban populations, particularly working professionals, form the core consumer base due to their frequent exposure to formal environments where appearance and comfort are critical. Within this segment, women account for a slightly higher share, reflecting stronger adoption of personal care products and grooming practices.

Institutional buyers, including the hospitality, healthcare, and fashion industries, are emerging as secondary demand drivers. In hospitality and healthcare, maintaining hygiene and professional appearance is essential, driving bulk procurement. The fashion and entertainment industries are also contributing to demand, particularly for events, performances, and long-duration shoots where sweat management is necessary. This diversification of end-use applications is gradually expanding the overall market scope.

Distribution Channel Insights

Online retail channels account for approximately 41% of total sales, making them the fastest-growing distribution segment. The rise of e-commerce platforms has significantly improved product accessibility, enabling consumers to explore a wide range of options, compare prices, and access customer reviews before purchasing. Subscription-based models are further driving recurring demand, particularly among regular users.

Offline channels, including pharmacies, supermarkets, and specialty stores, continue to play a vital role, especially in regions with lower digital penetration or among older demographics who prefer in-store purchases. These channels also provide immediate product availability and brand visibility. Direct-to-consumer (D2C) strategies are gaining momentum, allowing manufacturers to enhance customer engagement, gather consumer insights, and improve profit margins by reducing intermediary costs.

| By Product Type | By Material Type | By Absorbency Level | By End User | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 32% of the global market share in 2025, with the United States leading demand, followed by Canada. The region’s dominance is driven by high consumer awareness, strong purchasing power, and widespread adoption of personal hygiene and grooming products. Additionally, the presence of established brands, advanced retail infrastructure, and high penetration of e-commerce platforms significantly support market growth. The increasing demand for premium and eco-friendly products is also shaping innovation in this region. Workplace culture emphasizing professional appearance and comfort further reinforces product adoption.

Europe

Europe accounts for around 28% of the market, with key countries including Germany, the UK, and France. The region is characterized by strong regulatory frameworks and a high level of environmental consciousness among consumers. This has led to increased demand for biodegradable and sustainable sweat pads, driving innovation in material technologies. Additionally, rising awareness of personal hygiene and the growing popularity of organic and skin-friendly products are key growth drivers. Government regulations on single-use plastics are also pushing manufacturers toward sustainable alternatives, further shaping the regional market landscape.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR of approximately 10.5%, driven by countries such as China, India, and Japan. Rapid urbanization, increasing disposable incomes, and a growing middle-class population are key factors contributing to market expansion. Rising awareness of personal hygiene, particularly among younger consumers and working professionals, is accelerating adoption. In India and Southeast Asia, hot and humid climatic conditions significantly increase the need for sweat management products. Additionally, the rapid expansion of e-commerce platforms and digital marketing is enhancing product accessibility and awareness, further driving growth in the region.

Latin America

Latin America, led by Brazil and Mexico, is experiencing moderate but steady growth. The region’s warm climate creates a natural demand for sweat management solutions, while increasing urbanization and rising disposable incomes are supporting product adoption. Growing awareness of grooming and personal care, particularly among younger demographics, is further contributing to market expansion. However, price sensitivity remains a key factor, leading to higher demand for mid-range and economy products. The expansion of retail networks and online platforms is expected to improve market penetration over the forecast period.

Middle East & Africa

The Middle East and Africa region shows steady growth, driven primarily by extreme climatic conditions in countries such as the UAE and Saudi Arabia, where high temperatures significantly increase perspiration levels. Demand is further supported by a large expatriate population with higher purchasing power and strong adoption of personal care products. In addition, the growing retail sector and increasing availability of international brands are enhancing market accessibility. While awareness levels remain moderate in certain African countries, gradual improvements in urbanization, income levels, and distribution networks are expected to support long-term growth in the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|