Disposable Paper Plates Market Size

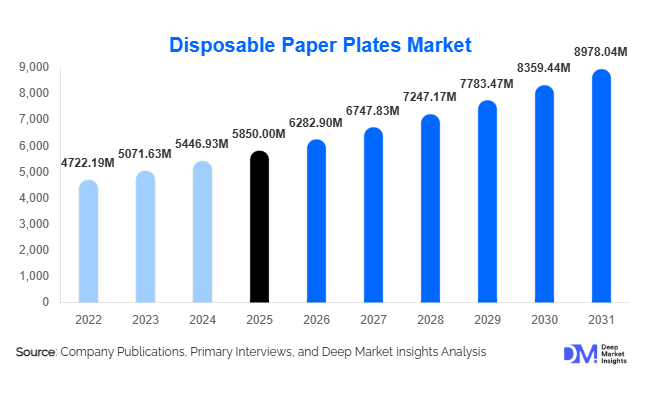

According to Deep Market Insights, the global disposable paper plates market size was valued at USD 5,850 million in 2025 and is projected to grow from USD 6,282.90 million in 2026 to reach USD 8,978.04 million by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for convenient, hygienic, and eco-friendly food service solutions, along with rising regulatory pressure against single-use plastics.

Key Market Insights

- Sustainability-driven demand is accelerating adoption, with biodegradable and compostable materials such as bagasse and bamboo gaining significant traction.

- Commercial food service dominates consumption, particularly quick-service restaurants (QSRs), catering businesses, and street food vendors.

- Asia-Pacific leads the global market, supported by high population density, urbanization, and strong manufacturing capabilities.

- Wholesale and bulk procurement channels dominate, driven by institutional and large-scale food service buyers.

- The economy segment leads in volume, especially in emerging markets where cost sensitivity remains high.

- Technological advancements in coatings and molding are improving durability, water resistance, and overall product performance.

What are the latest trends in the disposable paper plates market?

Shift Toward Compostable and Bio-Based Materials

The market is witnessing a strong transition from conventional coated paper plates to fully compostable alternatives. Materials such as bagasse (sugarcane residue), bamboo fiber, and palm leaves are gaining popularity due to their low environmental impact. Manufacturers are increasingly adopting PLA-based and water-based coatings to ensure both functionality and biodegradability. This trend is particularly strong in Europe and North America, where regulatory frameworks promote sustainable alternatives and penalize plastic usage.

Customization and Premium Product Offerings

Customization is emerging as a key trend, especially in the events and hospitality segment. Businesses are offering printed, themed, and designer paper plates tailored for weddings, corporate events, and branded food services. Premiumization is also evident through compartmentalized plates and enhanced durability features, allowing companies to target high-margin segments. This trend is enabling manufacturers to differentiate their offerings and move beyond commoditized pricing structures.

What are the key drivers in the disposable paper plates market?

Growing Food Service and Delivery Ecosystem

The rapid expansion of food delivery platforms, cloud kitchens, and quick-service restaurants is a major driver of demand. Disposable paper plates provide a convenient and hygienic solution for high-volume food operations. With the global food service industry exceeding USD 3 trillion, the demand for disposable tableware is closely linked to its growth trajectory.

Regulatory Push Against Plastic Products

Governments across the globe are implementing bans and restrictions on single-use plastics, driving the shift toward paper-based alternatives. Policies promoting biodegradable products and sustainable packaging are encouraging businesses to adopt disposable paper plates as a compliant solution. This regulatory support is a key factor underpinning long-term market growth.

What are the restraints for the global market?

Higher Costs Compared to Plastic Alternatives

Despite environmental benefits, disposable paper plates often have higher production costs, particularly for coated or compostable variants. This creates pricing challenges in developing markets where affordability is a critical factor influencing purchasing decisions.

Performance Limitations in Certain Applications

Paper plates may face limitations when handling heavy or high-moisture food items unless enhanced with coatings. However, such coatings can sometimes reduce biodegradability, creating a trade-off between functionality and sustainability. Overcoming this challenge remains essential for broader adoption.

What are the key opportunities in the disposable paper plates industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, Africa, and Latin America present significant growth opportunities due to rising urbanization, increasing disposable incomes, and expanding food service sectors. Localized manufacturing and distribution strategies can help companies tap into these high-growth regions effectively.

Integration of Advanced Manufacturing Technologies

Automation and high-speed molding technologies are enabling manufacturers to improve production efficiency and reduce costs. Investments in energy-efficient machinery and advanced coating technologies can enhance product quality while maintaining competitive pricing, creating opportunities for both new entrants and established players.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5850 Million |

| Market Size in 2026 | USD 6282.90 Million |

| Market Size in 2031 | USD 8978.04 Million |

| CAGR | 7.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Coated paper plates dominate the global disposable paper plates market, accounting for approximately 42% of the total market share in 2025. The primary driver behind this leadership is their enhanced functional performance, particularly resistance to moisture, oil, and heat, which makes them highly suitable for a wide range of food applications, including greasy, liquid-based, and hot meals. This durability advantage has made coated plates the preferred choice in commercial food service environments such as quick-service restaurants (QSRs), catering businesses, and takeaway outlets where product reliability is critical. Additionally, advancements in bio-based and water-based coatings are further strengthening this segment by aligning performance with sustainability requirements. Meanwhile, compartmentalized plates are witnessing increasing demand in premium and institutional applications, driven by their ability to separate multiple food items efficiently. This feature enhances food presentation, portion control, and convenience, making them particularly popular in airline catering, school meal programs, and large-scale events.

Material Type Insights

Bagasse-based plates lead the material segment with an estimated 28% market share in 2025, primarily driven by strong regulatory support for compostable and biodegradable products. Bagasse, a by-product of sugarcane processing, offers a sustainable and cost-effective alternative to traditional paper pulp while maintaining structural strength and heat resistance. The increasing global emphasis on circular economy practices and agricultural waste utilization has significantly accelerated the adoption of bagasse-based plates, particularly in Europe and North America. Recycled paper plates continue to maintain strong demand in price-sensitive markets due to their lower cost and acceptable performance for light-duty applications. At the same time, bamboo fiber and palm leaf plates are emerging as premium material options, driven by their superior durability, natural aesthetics, and chemical-free composition. These materials are increasingly preferred in high-end hospitality and eco-conscious consumer segments, where sustainability and product differentiation are key purchasing factors.

End-Use Insights

The commercial food service segment dominates the market with approximately 48% share in 2025, supported by the rapid expansion of QSR chains, food delivery platforms, and catering services globally. The primary growth driver for this segment is the need for cost-effective, hygienic, and disposable serving solutions capable of handling high customer volumes. The proliferation of street food vendors, especially in emerging markets, further strengthens demand. Household consumption remains a significant segment, driven by increasing preference for convenience during small gatherings, celebrations, and daily use in urban households. Meanwhile, institutional demand from schools, corporate offices, and healthcare facilities is growing steadily, supported by rising hygiene standards, bulk procurement practices, and the need for efficient food distribution systems. This segment is also benefiting from government initiatives promoting disposable, sanitary dining solutions in public institutions.

Distribution Channel Insights

Wholesale and bulk supply channels account for nearly 51% of total market sales, making them the leading distribution segment. This dominance is primarily driven by large-scale procurement by restaurants, catering companies, and institutional buyers who require consistent supply at competitive pricing. Bulk purchasing not only reduces per-unit costs but also ensures supply chain reliability, which is critical for high-volume operations. Retail channels, including supermarkets and convenience stores, cater mainly to household consumers and small-scale buyers, offering accessibility and product variety. E-commerce platforms are emerging as a fast-growing channel, supported by increasing digital adoption, competitive pricing, doorstep delivery, and the availability of customized and premium product offerings. The growth of online B2B marketplaces is also facilitating direct procurement for small and medium food service operators.

Price Range Insights

The economy segment leads the market with approximately 55% share in 2025, driven by high demand in emerging economies where affordability remains the most critical purchasing factor. These products are widely used by street vendors, small eateries, and budget-conscious consumers. The segment benefits from large-scale production and low-cost raw materials, enabling manufacturers to maintain competitive pricing. The mid-range segment offers a balance between cost and performance, catering to organized food service providers that require better durability without significantly increasing costs. Meanwhile, the premium segment is witnessing strong growth in developed markets, fueled by increasing environmental awareness and willingness to pay for eco-friendly, aesthetically appealing, and high-performance disposable tableware. Premium products often incorporate advanced materials and coatings, positioning them as sustainable alternatives to traditional disposables.

Explore more data points, trends and opportunities Download Free Sample Report

Disposable Paper Plates Market Segmentations

By Product Type

- Plain Paper Plates

- Coated Paper Plates

- Laminated Paper Plates

- Compartmentalized Plates

By Material Type

- Virgin Pulp-Based Paper Plates

- Recycled Paper Plates

- Bagasse (Sugarcane Fiber) Plates

- Bamboo Fiber Plates

- Palm Leaf Plates

By End-Use

- Household Consumption

- Commercial Food Service

- Institutional Use

- Events & Hospitality

By Distribution Channel

- Retail Sales

- Wholesale/Bulk Supply

- Online/E-commerce Platforms

By Price Range

- Economy Segment

- Mid-Range Segment

- Premium/Eco-Friendly Segment

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global disposable paper plates market with a 38% share in 2025 and is also the fastest-growing region, with a CAGR exceeding 9%. The region’s leadership is driven by a combination of high population density, rapid urbanization, and strong growth in the food service sector. Countries such as India, China, and Indonesia are key contributors. In India, the widespread street food culture and increasing adoption of disposable products for hygiene purposes are major demand drivers. China’s dominance is supported by its large-scale manufacturing capabilities, cost-efficient production, and export-oriented supply chains. Additionally, rising disposable incomes, expanding middle-class population, and increasing penetration of food delivery platforms are accelerating regional growth.

North America

North America holds approximately 24% of the global market share, led by the United States. The region’s growth is primarily driven by stringent environmental regulations aimed at reducing plastic waste, which has accelerated the adoption of biodegradable paper plates. High consumer awareness regarding sustainability and strong demand from established QSR chains and catering services further support market expansion. Additionally, the presence of advanced manufacturing technologies and a well-developed distribution network ensures consistent product availability. The growing trend of eco-friendly packaging in the food service industry continues to drive innovation and adoption in this region.

Europe

Europe accounts for around 22% of the global market, with key contributions from Germany, France, and the UK. The region’s growth is strongly influenced by strict regulatory frameworks, including bans on single-use plastics and mandates for compostable materials. These policies have significantly accelerated the shift toward paper-based disposable products. European consumers also exhibit high environmental consciousness, driving demand for premium, sustainable tableware. Additionally, government incentives for eco-friendly manufacturing and circular economy initiatives are encouraging innovation and investment in biodegradable materials, further strengthening market growth.

Latin America

Latin America is an emerging market, with Brazil and Mexico as the primary growth engines. The region is witnessing increased demand due to rapid urbanization, expansion of the food service industry, and a growing middle-class population. The rise of street food culture and informal food vendors is a significant driver of disposable paper plate consumption. Additionally, improving retail infrastructure and increasing penetration of organized food chains are contributing to market expansion. Although cost sensitivity remains a challenge, gradual shifts toward sustainable products are expected to support long-term growth.

Middle East & Africa

The Middle East and Africa region represents a smaller but steadily growing market. Countries such as the UAE and South Africa are leading demand, driven by expanding hospitality, tourism, and event management industries. Large-scale events, festivals, and a growing expatriate population are contributing to increased consumption of disposable tableware. Additionally, rising awareness of environmental sustainability and gradual regulatory shifts toward reducing plastic usage are supporting adoption of paper-based alternatives. Infrastructure development and increasing investments in the food service sector are expected to further drive growth in this region.

Key Players in the Disposable Paper Plates Market

- Huhtamaki Oyj

- Dart Container Corporation

- Graphic Packaging International

- Georgia-Pacific LLC

- International Paper Company

- Eco-Products Inc.

- Genpak LLC

- Vegware Ltd.

- Pactiv Evergreen Inc.

- Duni Group

- Lollicup USA Inc.

- Billerud AB

- WestRock Company

- Sabert Corporation

- Reynolds Consumer Products