Disinfectant Market Size

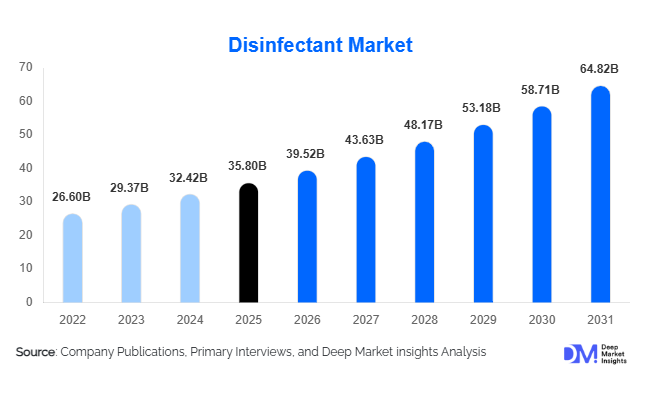

According to Deep Market Insights, the global disinfectant market size was valued at USD 35.8 billion in 2025 and is projected to grow from USD 39.52 billion in 2026 to reach USD 64.82 billion by 2031, expanding at a CAGR of 10.4% during the forecast period (2026–2031). The disinfectant market is experiencing growth primarily driven by rising global hygiene awareness, increasing measures to prevent healthcare-associated infections, expansion of healthcare infrastructure, and growing sanitation requirements across industrial, commercial, and residential sectors.

Key Market Insights

- Healthcare facilities remain the largest consumers of disinfectants globally, driven by strict infection prevention protocols and rising surgical procedures.

- Eco-friendly and bio-based disinfectants are rapidly gaining market traction, particularly across Europe and North America due to tightening environmental regulations.

- North America dominates the disinfectant market, supported by advanced healthcare infrastructure, institutional hygiene standards, and high per-capita sanitation spending.

- Asia-Pacific is the fastest-growing regional market, led by healthcare expansion, industrialization, and increasing public hygiene investments in China and India.

- Food processing and pharmaceutical manufacturing industries are emerging as major demand generators, driven by stricter contamination-control regulations.

- Technological adoption, including electrostatic sprayers, automated sanitation systems, UV-assisted disinfection, and robotic cleaning technologies, is reshaping operational efficiency across institutional environments.

Disinfectant Market Trends

Sustainable and Bio-Based Disinfectants Gaining Momentum

Environmental sustainability is becoming a major trend across the global disinfectant market as governments and institutional buyers increasingly prioritize safer and eco-friendly hygiene solutions. Manufacturers are investing heavily in biodegradable formulations, hydrogen peroxide-based products, botanical disinfectants, and low-residue chemistries to comply with stricter environmental and occupational safety regulations. The European market in particular is witnessing significant adoption of green disinfectants due to tightening chemical usage regulations under biocidal product frameworks. Corporate buyers in hospitality, healthcare, and commercial real estate sectors are also incorporating sustainability goals into procurement strategies, creating demand for recyclable packaging, reduced VOC emissions, and non-toxic cleaning solutions. This trend is encouraging manufacturers to differentiate products through green certifications, carbon-neutral production practices, and environmentally responsible formulations.

Automation and Smart Sanitization Technologies Expanding Rapidly

Technological integration is transforming disinfectant deployment across healthcare facilities, transportation hubs, airports, pharmaceutical plants, and commercial buildings. Automated fogging systems, electrostatic sprayers, robotic sanitation units, and IoT-enabled hygiene monitoring systems are increasingly being adopted to improve cleaning consistency and reduce labor dependency. Hospitals are implementing automated room disinfection systems to reduce healthcare-associated infections, while airports and hospitality facilities are integrating smart sanitation technologies to improve operational efficiency and customer confidence. Mobile monitoring platforms, automated chemical dispensing systems, and UV-assisted disinfection technologies are also improving process optimization and compliance tracking. This trend is expected to accelerate further as enterprises continue prioritizing workplace hygiene and infection-prevention infrastructure.

Disinfectant Market Drivers

Rising Global Focus on Infection Prevention

The increasing prevalence of healthcare-associated infections and infectious disease outbreaks has significantly accelerated demand for disinfectants across healthcare and public infrastructure environments. Hospitals, clinics, diagnostic laboratories, and long-term care facilities are maintaining stricter sanitation standards to minimize contamination risks and improve patient outcomes. Rising surgical volumes, aging populations, and expanding healthcare access across emerging economies are further increasing disinfectant consumption. Institutional buyers are increasingly prioritizing high-level disinfectants and advanced sterilization solutions that offer broad-spectrum microbial efficacy and faster kill times.

Expansion of Commercial and Industrial Hygiene Standards

Regulatory expansion across food processing, pharmaceutical manufacturing, water treatment, biotechnology, transportation, and industrial manufacturing sectors is supporting long-term disinfectant demand growth. Food safety compliance requirements are increasing adoption of food-contact surface disinfectants, while pharmaceutical manufacturing facilities require contamination-controlled environments supported by sterile cleaning systems. Airports, shopping malls, schools, offices, and hospitality establishments are also institutionalizing routine sanitization programs, transforming disinfectants into recurring operational necessities rather than temporary preventive products.

Disinfectant Market Restraints

Volatility in Raw Material Prices

Raw material price fluctuations continue to challenge disinfectant manufacturers globally. Key inputs including alcohols, chlorine derivatives, surfactants, hydrogen peroxide, and specialty chemicals are closely linked to petrochemical supply chains, creating pricing instability during periods of supply disruption. Rising packaging and transportation costs are further pressuring operating margins, especially among smaller manufacturers operating in highly competitive consumer categories. Manufacturers are increasingly adopting regional sourcing strategies and long-term procurement agreements to mitigate these cost pressures.

Increasing Regulatory and Environmental Compliance Requirements

The disinfectant industry is subject to stringent regulatory frameworks governing chemical safety, toxicity, labeling, efficacy validation, and environmental impact. Regulatory authorities in North America and Europe are tightening restrictions on certain active ingredients associated with respiratory irritation, environmental contamination, and hazardous residues. Compliance with EPA regulations, European Biocidal Products Regulation (BPR), FDA guidelines, and occupational safety standards requires continuous investments in product testing, reformulation, and certification processes. Smaller manufacturers often face significant operational and financial challenges in adapting to evolving regulatory expectations.

Disinfectant Market Opportunities

Expansion of Healthcare Infrastructure in Emerging Economies

The rapid development of healthcare infrastructure across the Asia-Pacific, Latin America, and the Middle East presents significant long-term opportunities for disinfectant manufacturers. Countries including India, China, Saudi Arabia, Indonesia, and Brazil are investing heavily in hospitals, diagnostic laboratories, public health systems, and surgical centers. These facilities require continuous procurement of high-level disinfectants, sterilization chemicals, and surface sanitation solutions. Government-led healthcare modernization programs and increasing public healthcare spending are expected to create recurring institutional demand contracts for global and regional disinfectant suppliers.

Growth of Food Processing and Pharmaceutical Manufacturing

Global expansion of food processing and pharmaceutical manufacturing industries is creating strong opportunities for specialized disinfectant products. Food exporters are increasingly adopting advanced sanitation protocols to comply with international safety standards, boosting demand for food-safe disinfectants and industrial cleaning systems. Pharmaceutical manufacturing facilities, biologics production plants, and vaccine manufacturing units require contamination-controlled cleanrooms and sterile production environments, supporting growth in high-purity disinfectant demand. Manufacturers offering low-residue and rapid-action products are expected to benefit significantly from these expanding industrial applications.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 35.8 Billion |

| Market Size in 2026 | USD 39.52 Billion |

| Market Size in 2031 | USD 64.82 Billion |

| CAGR | 10.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Surface disinfectants dominate the global disinfectant market, accounting for nearly 38% of total market revenue in 2025. Their widespread use across hospitals, commercial buildings, households, industrial facilities, and transportation infrastructure continues to support strong recurring demand. Liquid disinfectants remain the leading product format because of their versatility, scalability for institutional cleaning operations, and compatibility with automated dispensing systems. Wipes and spray disinfectants are witnessing rapid adoption within residential and commercial environments due to convenience, portability, and faster application. Instrument disinfectants are also experiencing steady growth, particularly in healthcare settings where stringent sterilization protocols are becoming increasingly important for infection prevention and patient safety compliance.

Application Insights

Surface cleaning and sanitization remain the largest application segment, contributing approximately 35% of global disinfectant market revenue in 2025. Increasing sanitation frequency across hospitals, transportation systems, educational institutions, offices, and hospitality facilities continues to drive segment growth. Medical device reprocessing and instrument sterilization applications are expanding rapidly due to rising surgical volumes and stricter healthcare hygiene standards. Water treatment applications are also generating strong demand for chlorine-based and ozone-based disinfectants as governments strengthen wastewater management and drinking water safety regulations. Food processing hygiene applications are growing significantly because of rising export-oriented manufacturing and tightening food safety compliance requirements across global supply chains.

Distribution Channel Insights

Direct institutional sales dominate the disinfectant market, accounting for nearly 41% of total market revenue globally. Large hospitals, pharmaceutical manufacturers, industrial facilities, airports, and government institutions typically procure disinfectants through long-term supply agreements to ensure product availability and regulatory compliance. Retail channels including supermarkets, pharmacies, and specialty cleaning suppliers continue to play a major role in residential disinfectant sales. E-commerce platforms are expanding rapidly, especially in emerging economies where online retail penetration is improving access to household and commercial disinfectant products. Manufacturers are increasingly strengthening direct-to-consumer digital strategies while integrating subscription-based hygiene supply models for recurring institutional and residential customers.

End-Use Industry Insights

Healthcare facilities remain the largest end-use segment within the global disinfectant market, contributing approximately 32% of total market demand in 2025. Hospitals, diagnostic laboratories, ambulatory surgical centers, and clinics require continuous disinfectant consumption to maintain infection-control standards. Food and beverage processing is one of the fastest-growing end-use industries due to rising global food exports and stricter contamination-control regulations. Pharmaceutical and biotechnology manufacturing facilities are also increasing disinfectant usage because of expanding sterile production requirements and biologics manufacturing growth. Commercial real estate, hospitality, transportation, and educational institutions are emerging as important demand generators as organizations institutionalize long-term hygiene and sanitation programs.

Explore more data points, trends and opportunities Download Free Sample Report

Disinfectant Market Segmentations

By Product Type

- Surface Disinfectants

- Air Disinfectants

- Instrument Disinfectants

- Skin and Hand Disinfectants

- Water Disinfectants

- Textile and Laundry Disinfectants

- Food Contact Surface Disinfectants

- Industrial Process Disinfectants

By Active Ingredient

- Quaternary Ammonium Compounds (QACs)

- Chlorine-based Disinfectants

- Alcohol-based Disinfectants

- Hydrogen Peroxide-based Disinfectants

- Peracetic Acid Disinfectants

- Phenolic Compounds

- Iodophors

- Aldehyde-based Disinfectants

- Bio-based and Botanical Disinfectants

By Application

- Surface Cleaning and Sanitization

- Instrument Sterilization and Reprocessing

- Water Treatment

- Air Quality and HVAC Sanitization

- Food Processing Hygiene

- Medical Device Reprocessing

- Household Cleaning

- Industrial Sanitation

- Biohazard Decontamination

By End-Use Industry

- Healthcare Facilities

- Residential and Household

- Commercial Buildings

- Food & Beverage Processing

- Pharmaceutical & Biotechnology Manufacturing

- Water & Wastewater Treatment

- Industrial Manufacturing

- Agriculture & Livestock

- Transportation & Logistics

- Government & Public Infrastructure

By Distribution Channel

- Direct Sales / Institutional Contracts

- Retail Stores

- Hypermarkets and Supermarkets

- Pharmacies and Drug Stores

- E-commerce Platforms

- Specialty Cleaning Suppliers

- Wholesale and Distributor Networks

Regional Insights

North America

North America accounted for approximately 34% of the global disinfectant market in 2025, making it the largest regional market. The United States dominates regional demand due to extensive healthcare infrastructure, advanced sanitation standards, and strong institutional procurement systems. Hospitals, pharmaceutical facilities, food processing plants, and commercial real estate sectors are major contributors to disinfectant consumption. Canada is also witnessing strong demand growth driven by healthcare hygiene regulations and increasing adoption of environmentally sustainable disinfectant formulations.

Europe

Europe represented nearly 27% of global disinfectant market revenue in 2025. Germany, the United Kingdom, and France are the leading regional markets due to strong healthcare spending and strict environmental compliance standards. Demand for eco-friendly and low-toxicity disinfectants is rising significantly across Europe as governments tighten restrictions on hazardous chemical formulations. Food processing and pharmaceutical manufacturing industries continue to generate substantial institutional demand across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and accounted for nearly 25% of global revenue in 2025. China remains the largest market in the region because of its extensive manufacturing sector, healthcare expansion, and urbanization. India is expected to record one of the highest growth rates globally due to rising healthcare investments, improving public hygiene awareness, and government sanitation initiatives. Japan and South Korea continue to generate strong demand for premium disinfectant technologies and automated sanitation systems.

Latin America

Latin America is witnessing steady growth in disinfectant demand, particularly in Brazil and Mexico. Expanding healthcare infrastructure, food processing activities, and commercial sanitation standards are supporting regional market expansion. Export-oriented manufacturing industries are increasingly investing in industrial hygiene systems to comply with international safety standards, boosting demand for institutional disinfectants across the region.

Middle East & Africa

The Middle East & Africa region is benefiting from rising investments in healthcare facilities, public infrastructure, airports, and hospitality projects. GCC countries including Saudi Arabia and the UAE are strengthening public sanitation programs and healthcare modernization initiatives, supporting strong institutional disinfectant demand. South Africa remains one of the largest African markets due to healthcare infrastructure expansion and growing industrial sanitation requirements.

Key Players in the Disinfectant Market

- 3M Company

- Reckitt Benckiser Group plc

- Ecolab Inc.

- The Clorox Company

- STERIS plc

- Kimberly-Clark Corporation

- SC Johnson & Son Inc.

- Procter & Gamble Company

- Diversey Holdings Ltd.

- GOJO Industries Inc.

- Johnson & Johnson

- Whiteley Corporation

- Medline Industries LP

- BD (Becton, Dickinson and Company)

- Bio-Cide International Inc.