Digital Piano Market Size

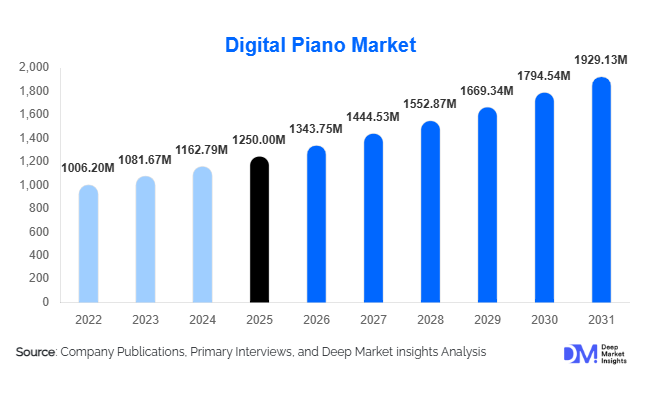

According to Deep Market Insights, the global digital piano market size was valued at USD 1,250 million in 2025 and is projected to grow from USD 1,343.75 million in 2026 to reach USD 1,929.13 million by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The digital piano market growth is primarily driven by increasing demand for compact and affordable alternatives to acoustic pianos, rising interest in music education, and continuous technological advancements in sound modeling and connectivity features.

Key Market Insights

- Portable and smart-enabled digital pianos are gaining traction, driven by growing adoption among beginners and hobbyists.

- Asia-Pacific dominates the market, supported by strong manufacturing capabilities and rising middle-class demand.

- Residential users account for the largest share, fueled by increasing home-based learning trends.

- Mid-range digital pianos lead pricing segments, balancing affordability with advanced features.

- Technological integration, including AI-assisted learning apps and Bluetooth connectivity, is reshaping the user experience.

- Online retail channels are rapidly expanding, supported by increasing digital adoption and e-commerce penetration.

What are the latest trends in the digital piano market?

Smart Learning Integration and App Connectivity

Digital pianos are increasingly being integrated with mobile applications and cloud-based learning platforms. Features such as real-time feedback, guided tutorials, and gamified learning experiences are transforming how users engage with instruments. This trend is particularly appealing to beginners and younger demographics, who prefer interactive and self-paced learning. Manufacturers are also introducing subscription-based ecosystems that combine hardware with software, enabling recurring revenue models and stronger customer retention.

Advancements in Sound Modeling Technology

Technological innovation in sound engines is narrowing the gap between digital and acoustic pianos. Modeling-based sound generation and hybrid systems are enabling more realistic tonal quality and dynamic response. High polyphony, improved speaker systems, and advanced key actions are enhancing performance quality, making digital pianos more appealing to professional musicians and institutions. This trend is driving growth in premium and hybrid segments.

What are the key drivers in the digital piano market?

Growing Demand for Home-Based Music Learning

The increasing popularity of home-based hobbies and online learning has significantly boosted demand for digital pianos. Consumers are investing in musical instruments as part of personal development and leisure activities. The availability of affordable entry-level models and online tutorials has further accelerated adoption among beginners.

Cost and Maintenance Advantages over Acoustic Pianos

Digital pianos offer a cost-effective alternative to traditional acoustic pianos, with lower upfront costs and minimal maintenance requirements. Features such as headphone compatibility, portability, and built-in recording capabilities make them suitable for urban environments, further driving market growth.

Technological Advancements in User Experience

Continuous innovation in weighted key mechanisms, sound sampling, and connectivity features is enhancing the overall playing experience. Integration with smart devices and music software is expanding the functionality of digital pianos, attracting both amateur and professional users.

What are the restraints for the global market?

Preference for Acoustic Authenticity

Despite technological advancements, some professional musicians continue to prefer acoustic pianos for their superior tonal richness and tactile feedback. This perception limits the adoption of digital pianos in high-end performance settings.

Price Sensitivity in Emerging Markets

While demand is growing globally, affordability remains a challenge in developing regions. Import duties, currency fluctuations, and limited purchasing power restrict the adoption of mid-range and premium models, slowing overall market penetration.

What are the key opportunities in the digital piano industry?

Expansion in Emerging Markets

Rapid urbanization, rising disposable incomes, and growing interest in Western music are creating significant opportunities in Asia, Latin America, and Africa. Localized product offerings and competitive pricing strategies can help manufacturers capture these untapped markets.

Integration with Digital Education Ecosystems

The rise of online music education platforms presents opportunities for manufacturers to develop integrated solutions combining hardware and software. Partnerships with educational institutions and edtech platforms can further expand market reach and create new revenue streams.

Innovation in Hybrid and Premium Segments

Hybrid digital pianos that replicate acoustic mechanisms are gaining popularity among professionals and institutions. Innovations in sound technology, silent practice modes, and customizable acoustics are expected to drive growth in high-end segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1250 Million |

| Market Size in 2026 | USD 1343.75 Million |

| Market Size in 2031 | USD 1929.13 Million |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Portable digital pianos continue to dominate the market, accounting for approximately 38% of the global share in 2025. The leadership of this segment is primarily driven by its strong alignment with evolving consumer preferences for affordability, portability, and space efficiency. Increasing urbanization, particularly in the Asia-Pacific and Europe, has resulted in smaller living spaces, making compact instruments more desirable. Additionally, the rapid growth of beginner and hobbyist users, supported by online music learning platforms, has significantly boosted demand for portable models. Console digital pianos maintain a stable position among home users who prioritize aesthetics and furniture-style integration, particularly in North America and Europe. Stage pianos, although niche, are gaining traction among professional performers and studio musicians due to their advanced sound customization and portability for live performances. Meanwhile, hybrid digital pianos are emerging as a high-growth segment within the premium category, driven by demand for acoustic-like touch and sound among advanced players and institutions.

Technology Insights

Sample-based sound generation leads the market with around 55% share, primarily due to its cost efficiency and scalability across entry-level and mid-range products. The widespread adoption of this technology is driven by manufacturers’ ability to replicate acoustic piano sounds at a lower production cost, making it accessible to a broader consumer base. However, modeling-based sound engines are witnessing rapid growth, especially in premium and professional-grade instruments, as they provide superior tonal accuracy, dynamic responsiveness, and real-time sound modulation. This segment is being propelled by increasing demand from advanced musicians and performance artists seeking authenticity. Hybrid sound systems, combining both sampling and modeling technologies, are emerging as a key innovation area, enabling manufacturers to differentiate their offerings and cater to evolving user expectations for realism and customization.

Connectivity Insights

Smart-enabled digital pianos account for nearly 42% of the market, reflecting a strong shift toward digitally integrated musical ecosystems. The growth of this segment is driven by rising adoption of Bluetooth connectivity, mobile app integration, and cloud-based learning platforms. Consumers, particularly younger demographics, are increasingly seeking instruments that offer interactive learning experiences, real-time feedback, and compatibility with digital audio workstations. Basic connectivity models, including MIDI and USB interfaces, continue to dominate the entry-level segment due to affordability considerations. Meanwhile, advanced IoT-enabled pianos with AI-assisted features and cloud synchronization are gaining traction among tech-savvy users and professionals, indicating a clear trend toward smart and connected instruments.

Key Mechanism Insights

Fully weighted keys dominate the market with approximately 60% share, driven by the growing emphasis on replicating the tactile experience of acoustic pianos. This segment’s leadership is supported by increasing awareness among learners and educators regarding the importance of proper finger technique and muscle development. As a result, even mid-range digital pianos are incorporating weighted key mechanisms. Semi-weighted and unweighted keys remain relevant in entry-level models, catering primarily to beginners and casual users who prioritize affordability and ease of use over realism. However, the long-term trend indicates a gradual shift toward fully weighted systems as consumer expectations evolve.

Price Range Insights

Mid-range digital pianos (USD 500–1500) lead the market with around 47% share, as they offer an optimal balance between affordability and advanced functionality. This segment is driven by growing middle-class populations, particularly in emerging markets, who seek high-quality instruments without premium pricing. Entry-level models continue to drive volume sales, especially among first-time buyers and students, supported by increasing accessibility through online retail channels. On the other hand, premium digital pianos are experiencing steady growth due to rising demand for high-performance instruments among professionals and institutions, with higher profit margins supported by advanced features such as hybrid sound engines and superior build quality.

Distribution Channel Insights

Offline retail channels account for approximately 58% of total sales, maintaining their dominance due to the experiential nature of musical instrument purchases. Consumers often prefer to physically test key actions, sound quality, and build before making a purchase decision. This trend is particularly strong in premium and mid-range segments. However, online channels are rapidly expanding, driven by increasing e-commerce penetration, competitive pricing, and the availability of detailed product comparisons and reviews. The growth of direct-to-consumer (D2C) sales models and brand-owned digital platforms is further accelerating online adoption, particularly among younger and tech-savvy consumers.

End-Use Insights

Residential users dominate the market with about 52% share, driven by the rising popularity of music as a hobby and the expansion of online learning platforms. The COVID-19 pandemic has had a lasting impact on consumer behavior, with more individuals investing in home-based activities, including music learning. Institutional demand from schools, universities, and music academies is growing steadily, supported by government initiatives promoting arts education and the scalability advantages of digital pianos over acoustic alternatives. The professional segment, while smaller in volume, represents a high-value market driven by advancements in stage pianos and hybrid models, as well as increasing demand from music production studios and live performance settings.

Explore more data points, trends and opportunities Download Free Sample Report

Digital Piano Market Segmentations

By Product Type

- Console Digital Pianos

- Portable Digital Pianos

- Stage Digital Pianos

- Hybrid Digital Pianos

By Technology

- Sample-Based Sound Generation

- Modeling-Based Sound Generation

- Hybrid Sound Engines

By Price Range

- Entry-Level (Below USD 500)

- Mid-Range (USD 500–1500)

- Premium (Above USD 1500)

By Distribution Channel

- Offline Retail

- Online Retail

By End-Use

- Residential

- Institutional

- Professional

Regional Insights

Asia-Pacific

Asia-Pacific leads the digital piano market with approximately 42% share in 2025, making it the largest and fastest-growing regional market. China dominates regional demand, contributing nearly 18% of global consumption, driven by rising disposable incomes, an expanding middle-class population, and a strong cultural emphasis on music education. Government-supported arts programs and increasing enrollment in music schools further reinforce demand. Japan serves as both a major consumer and a global innovation hub, with leading manufacturers driving technological advancements. India is emerging as a high-growth market, supported by rapid urbanization, a growing youth population, increasing exposure to Western music, and rising adoption of online learning platforms. Additionally, the region benefits from strong manufacturing ecosystems, enabling cost-effective production and global exports.

North America

North America holds around 25% market share, with the United States being the primary contributor. The region’s growth is driven by high disposable income levels, strong consumer spending on recreational activities, and a well-established music culture. Demand is particularly strong in the premium and professional segments, supported by advanced music production industries and live performance ecosystems. The increasing popularity of home studios and digital content creation is also boosting demand for stage and hybrid digital pianos. Furthermore, the presence of established distribution networks and a growing preference for technologically advanced products are key drivers of regional growth.

Europe

Europe accounts for approximately 22% of the global market, with major contributions from Germany, the UK, and France. The region’s growth is driven by its strong heritage in classical music and well-established institutional frameworks for music education. Government funding for arts and cultural programs supports demand from schools and academies. Additionally, European consumers exhibit a high preference for premium and aesthetically designed instruments, driving demand for console and hybrid digital pianos. Sustainability considerations and stringent regulatory standards are also influencing product innovation and purchasing decisions in the region.

Latin America

Latin America represents a smaller but steadily growing market, led by Brazil and Mexico. The region’s growth is primarily driven by increasing urbanization, rising middle-class income levels, and growing interest in music education and entertainment. Demand is concentrated in entry-level and mid-range segments due to price sensitivity among consumers. Expanding online retail infrastructure and increasing the availability of affordable digital pianos are further supporting market penetration. Additionally, cultural trends and the popularity of music-related content on digital platforms are contributing to rising adoption.

Middle East & Africa

The Middle East and Africa region contributes around 6–7% of the global market, with growth concentrated in urban centers such as the UAE and South Africa. The region’s expansion is driven by increasing disposable incomes, cultural diversification, and growing interest in Western music and entertainment. Investments in retail infrastructure and the expansion of specialty music stores are improving product accessibility. In the Middle East, high-income consumers are driving demand for premium digital pianos, while in Africa, entry-level models are gaining traction due to affordability. Additionally, the growing presence of international brands and distributors is supporting market development across the region.

Key Players in the Digital Piano Market

- Yamaha Corporation

- Roland Corporation

- Kawai Musical Instruments

- Casio Computer Co.

- Korg Inc.

- Nord Keyboards

- Kurzweil Music Systems

- Dexibell

- Artesia Pro

- Williams Pianos

- Medeli Electronics

- Donner Music

- Alesis

- Ringway Tech

- Guangzhou Pearl River Piano Group