Digital Pen Market Size

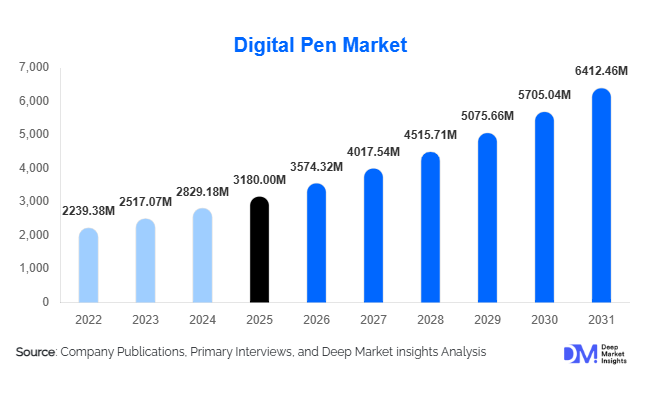

According to Deep Market Insights, the global digital pen market size was valued at USD 3,180 million in 2025 and is projected to grow from USD 3,574.32 million in 2026 to reach USD 6,412.46 million by 2031, expanding at a CAGR of 12.4% during the forecast period (2026–2031). The digital pen market growth is primarily driven by the rapid adoption of stylus-enabled tablets and 2-in-1 devices, increasing digitization of education and enterprise workflows, and growing demand for precise digital input tools across creative and professional applications. Advancements in pressure sensitivity, palm rejection, AI handwriting recognition, and cloud collaboration technologies are further strengthening adoption globally.

Key Market Insights

- Digital learning ecosystems are accelerating stylus adoption, with educational institutions increasingly deploying tablet-based learning environments.

- OEM bundling strategies are reshaping purchasing behavior, as device manufacturers integrate digital pens within broader hardware ecosystems.

- Asia-Pacific dominates global demand, supported by large-scale electronics manufacturing and education digitization initiatives.

- Enterprise digitization and hybrid work models are expanding use cases for annotation, documentation, and collaborative workflows.

- Creative professionals remain a high-value segment, driving premium digital pen innovation through demand for precision and responsiveness.

- AI-powered handwriting recognition and smart note automation are emerging as major technological differentiators.

What are the latest trends in the digital pen market?

AI-Enabled Writing and Smart Productivity Tools

Artificial intelligence integration is transforming digital pens from simple input accessories into intelligent productivity devices. Modern digital pens increasingly support handwriting-to-text conversion, language translation, meeting summarization, and contextual annotation recognition. Enterprise users are adopting stylus-based workflows for document editing and collaborative ideation, while students benefit from automated note organization. Software ecosystems linked to cloud platforms allow handwritten notes to synchronize instantly across devices, improving workflow continuity. AI-assisted features are also enabling searchability of handwritten content, making digital pens more valuable in professional environments where documentation efficiency is critical.

Expansion of Stylus-Compatible Device Ecosystems

Device manufacturers are expanding stylus compatibility across tablets, laptops, and interactive displays. The rise of 2-in-1 laptops and large-format collaborative screens is significantly increasing addressable demand. Digital pens are increasingly bundled with premium devices to enhance productivity positioning and ecosystem lock-in. Improvements in latency reduction, pressure sensitivity, and battery efficiency have narrowed the experience gap between digital and traditional writing tools. As remote collaboration becomes standard, stylus-enabled annotation during virtual meetings is emerging as a core productivity feature across industries.

What are the key drivers in the digital pen market?

Growth of Hybrid Work and Paperless Enterprises

The transition toward hybrid work environments has accelerated demand for digital annotation and document collaboration tools. Professionals increasingly rely on stylus-enabled devices to review contracts, annotate presentations, and brainstorm ideas during virtual meetings. Enterprises adopting paperless workflows view digital pens as essential productivity accessories, supporting secure documentation and workflow digitization while preserving natural handwriting interaction.

Rising Adoption in Digital Education

Education systems worldwide are integrating tablets into classrooms, creating sustained demand for digital pens. Subjects requiring handwriting, such as mathematics, engineering, and design, benefit significantly from stylus-based input. Government-backed smart classroom initiatives and EdTech investments are driving institutional procurement, creating predictable long-term demand cycles for manufacturers.

What are the restraints for the global market?

Device Compatibility Limitations

Many digital pens operate within proprietary ecosystems, restricting interoperability across devices and brands. Consumers often need multiple styluses for different platforms, reducing convenience and slowing broader adoption. Fragmented standards remain a key barrier to universal stylus deployment.

High Pricing of Premium Stylus Devices

Advanced digital pens with pressure sensitivity and AI capabilities are priced significantly higher than conventional accessories. Price sensitivity in emerging markets limits penetration despite strong growth in compatible device shipments. Manufacturers must balance innovation with affordability to expand adoption.

What are the key opportunities in the digital pen industry?

Government-Led Digital Education Programs

National education digitization initiatives represent a major opportunity for market participants. Governments investing in tablet-based learning environments create large-scale procurement opportunities for digital pens. Institutional contracts provide stable revenue streams and enable manufacturers to scale production efficiently. Emerging economies implementing smart classroom programs are expected to become major demand centers over the next decade.

Healthcare and Industrial Documentation Applications

Healthcare professionals increasingly require secure electronic documentation solutions that preserve handwriting workflows. Digital pens enable accurate patient record annotation and prescription input while maintaining compliance standards. Similarly, engineering and industrial sectors are adopting stylus-enabled systems for design sketches, inspections, and field documentation, opening new B2B growth avenues.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3180.00 Million |

| Market Size in 2026 | USD 3574.32 Million |

| Market Size in 2031 | USD 6412.46 Million |

| CAGR | 12.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The digital pen market demonstrates strong diversification across product categories, with active digital pens emerging as the dominant segment, accounting for nearly 46% of global demand. The leadership of active digital pens is primarily driven by their advanced technological capabilities, including high-pressure sensitivity levels, tilt recognition, palm rejection functionality, and low-latency precision input. These features enable seamless handwriting replication and accurate drawing performance, making them highly suitable for professional, educational, and enterprise environments. Increasing integration with premium tablets, laptops, and hybrid devices further accelerates adoption, as manufacturers position stylus-enabled devices as productivity-enhancing tools for both consumers and professionals.Passive stylus pens continue to maintain a stable presence in entry-level applications due to their affordability, universal compatibility, and ease of use without requiring internal electronics or battery power.

Their adoption remains strong among casual users and emerging markets where cost sensitivity plays a major role in purchasing decisions. Meanwhile, smart pens equipped with optical tracking and memory storage capabilities are gaining significant traction across education and enterprise environments. These devices enable offline writing capture and later synchronization with digital platforms, supporting hybrid workflows that combine traditional handwriting with digital storage and collaboration.Electromagnetic resonance (EMR) pens remain highly preferred within professional creative workflows due to superior accuracy, minimal latency, and battery-free operation. Designers, architects, engineers, and illustrators increasingly rely on EMR technology for precision-intensive tasks such as digital illustration, technical drafting, and 3D modeling. The leading segment growth is therefore driven by rising demand for natural writing experiences, professional-grade creative tools, and expanding stylus compatibility across next-generation computing devices.

Application Insights

Writing and note-taking applications represent the largest application segment, contributing approximately 34% of total market demand. The segment’s leadership is primarily supported by accelerating digitization across enterprises and educational institutions seeking efficient documentation, cloud synchronization, and paperless workflows. Digital pens enable real-time note capture, searchable handwriting, and collaborative sharing, significantly improving productivity in academic and professional environments. The widespread adoption of digital classrooms and remote learning platforms further strengthens demand for stylus-enabled note-taking solutions.Drawing and graphic design applications are expanding rapidly as digital content creation industries experience substantial growth across animation, gaming, advertising, and social media production. Artists and designers increasingly prefer stylus-based interfaces due to enhanced control and creative flexibility compared to traditional input devices.

Business documentation and collaborative annotation applications are also gaining momentum, particularly with the continued adoption of hybrid and remote work models that require efficient digital review, markup, and workflow collaboration tools.Healthcare documentation is emerging as an important application area as hospitals and clinics transition toward electronic medical records and digital prescription systems. Digital pens allow practitioners to maintain familiar handwriting workflows while improving data accuracy and accessibility. Additionally, engineering and industrial design sectors are increasingly incorporating stylus-based prototyping and visualization tools to streamline design iterations and enhance workflow efficiency. The leading segment growth is therefore driven by widespread digital transformation initiatives, remote collaboration trends, and increasing reliance on intuitive human-computer interaction technologies.

Distribution Channel Insights

OEM bundled sales dominate distribution channels, accounting for roughly 36% of total shipments, as device manufacturers increasingly integrate stylus compatibility into premium tablets, laptops, and detachable computing devices. Bundled offerings enhance product value propositions while encouraging users to adopt stylus functionality as part of their primary computing experience. The growth of this channel is supported by strategic partnerships between hardware manufacturers and digital pen technology providers, enabling seamless ecosystem integration.Online retail channels are witnessing rapid expansion as consumers increasingly prefer direct purchasing options supported by competitive pricing, product comparisons, and wider availability of accessories. E-commerce platforms enable manufacturers to reach global audiences efficiently while facilitating product education through reviews and demonstrations.

Electronics retail stores continue to play a crucial role in premium product positioning, allowing consumers to experience stylus responsiveness and device compatibility firsthand before purchase decisions.Institutional procurement channels remain highly significant, particularly for education systems and enterprise deployments that rely on bulk purchasing agreements and long-term digital infrastructure planning. Governments and organizations increasingly procure stylus-enabled devices as part of digital transformation programs, supporting sustained channel growth. The leading channel growth driver is therefore the expansion of integrated device ecosystems combined with institutional-scale digital adoption initiatives.

End-User Insights

Consumer users account for approximately 38% of total market demand, supported by rising tablet adoption, digital creativity trends, and increasing use of stylus tools for productivity, entertainment, and personal organization. Consumers are increasingly leveraging digital pens for journaling, sketching, media editing, and remote communication, contributing to consistent segment expansion. Enhanced user experience and improved handwriting recognition technologies further strengthen consumer adoption.Educational institutions represent the fastest-growing end-user segment, driven by widespread implementation of digital classrooms, e-learning platforms, and government-supported education technology initiatives. Digital pens facilitate interactive learning, digital assignments, and real-time feedback, enabling educators to replicate traditional classroom engagement within digital environments.

Enterprises are steadily expanding stylus usage across documentation workflows, collaborative editing, and meeting annotations as organizations transition toward paperless operations.Creative professionals remain a high-value niche segment due to demand for premium features such as pressure sensitivity, tilt control, and ultra-low latency performance. Meanwhile, healthcare institutions are emerging as a new adoption category as digital recordkeeping becomes standardized and regulatory compliance encourages secure digital documentation. The leading segment growth driver across end users is the global shift toward productivity-focused digital ecosystems that prioritize natural input interfaces.

Explore more data points, trends and opportunities Download Free Sample Report

Digital Pen Market Segmentations

By Technology Type

- Active Digital Pens

- Passive Stylus Pens

- Smart Pens with Optical Tracking

- Electromagnetic Resonance (EMR) Pens

- Bluetooth-Enabled Digital Pens

By Application

- Writing & Note-taking

- Drawing & Graphic Design

- Education & E-learning

- Business & Documentation

- Healthcare Documentation

- Industrial Design & Engineering

By Distribution Channel

- Online Retail

- Electronics Retail Stores

- Institutional Procurement

- OEM Bundled Sales

By End User

- Consumer/Personal Use

- Educational Institutions

- Enterprises & Corporate Offices

- Healthcare Institutions

- Creative Professionals

Regional Insights

North America

North America accounted for nearly 32% of the global digital pen market share in 2025, led primarily by the United States, which benefits from early technology adoption and strong digital infrastructure. Regional growth is driven by widespread penetration of tablets and 2-in-1 laptops across both consumer and enterprise environments. Corporate initiatives focused on paperless workflows and digital collaboration significantly accelerate adoption, particularly within finance, consulting, healthcare, and education sectors. The presence of leading technology companies and a mature creative industry ecosystem further strengthens demand for advanced stylus solutions. Canada is also witnessing increasing adoption supported by government-backed digital learning investments and expanding remote education infrastructure, reinforcing steady regional growth.

Europe

Europe represents approximately 21% of global demand, with Germany, the United Kingdom, and France serving as key adoption hubs. Regional growth is largely supported by enterprise digital transformation initiatives aimed at improving operational efficiency and sustainability through reduced paper usage. Strong creative design industries across Western Europe contribute significantly to demand for professional-grade stylus technologies. Additionally, European Union education digitization programs and funding initiatives continue to promote adoption of stylus-enabled devices within schools and universities. Increasing regulatory emphasis on digital documentation and secure data management also drives enterprise deployment across public sector organizations.

Asia-Pacific

Asia-Pacific dominates the global market with about 38% share and remains the fastest-growing regional market. Growth is fueled by large-scale consumer electronics manufacturing, expanding middle-class populations, and rapid digitalization across education and enterprise sectors. China leads both production and consumer adoption due to strong domestic device manufacturing capabilities and growing demand for digital productivity tools. Japan and South Korea demonstrate high adoption among professional designers, engineers, and technology-driven enterprises that prioritize precision input technologies. India is emerging as one of the fastest-growing markets, supported by large-scale digital education initiatives, expanding internet penetration, and increasing affordability of stylus-compatible tablets. Rising startup ecosystems and remote work adoption further accelerate regional expansion.

Latin America

Latin America is witnessing gradual but consistent adoption led by Brazil and Mexico. Regional growth is primarily supported by expanding remote learning infrastructure and increasing accessibility of affordable stylus-compatible devices. Governments and educational institutions are investing in digital inclusion programs aimed at improving learning outcomes through technology adoption. Enterprise digitization initiatives, particularly within banking, retail, and public administration sectors, are also contributing to growing demand. Improving e-commerce penetration and rising consumer awareness of productivity devices are expected to further support long-term regional market development.

Middle East & Africa

The Middle East and Africa region is experiencing steady growth driven by ongoing technology modernization and smart education initiatives. Countries such as the United Arab Emirates and Saudi Arabia are investing heavily in digital classrooms and knowledge-based economic diversification programs, which significantly increase demand for stylus-enabled devices. Institutional procurement across government and education sectors remains a major growth driver, supported by national digital transformation strategies. In Africa, improving connectivity infrastructure and expanding access to affordable digital devices are gradually encouraging adoption. Increasing use of digital collaboration tools across enterprise and public sector organizations is expected to strengthen regional market expansion over the forecast period.

Key Players in the Digital Pen Market

- Apple Inc.

- Samsung Electronics

- Microsoft Corporation

- Wacom Co., Ltd.

- Lenovo Group Ltd.

- HP Inc.

- Dell Technologies

- Huawei Technologies

- Logitech International

- ASUS

- Acer Inc.

- Xiaomi Corporation

- Sony Corporation

- Hanvon Technology

- STAEDTLER Digital