Digital Gift Cards Market Size

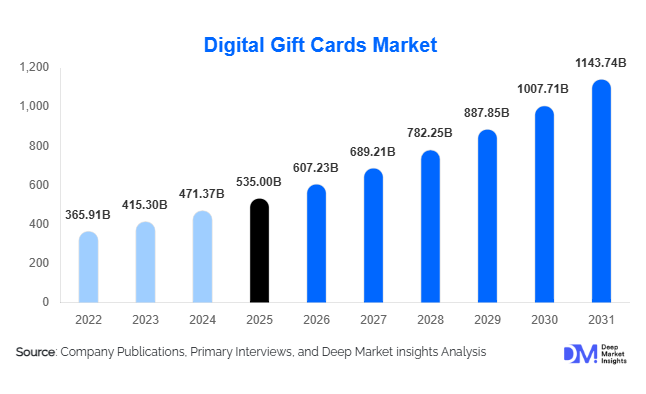

According to Deep Market Insights, the global Digital Gift Cards Market size was valued at USD 535 billion in 2025 and is projected to grow from USD 607.23 billion in 2026 to reach approximately USD 1,143.74 billion by 2031, expanding at a CAGR of 13.5% during the forecast period (2026–2031). The market growth is primarily driven by the rapid expansion of digital payment ecosystems, increasing penetration of mobile wallets, rising adoption of e-commerce platforms, and growing corporate use of digital gift cards for employee engagement, loyalty programs, and promotional campaigns.

Key Market Insights

- Digital gift cards are increasingly integrated into mobile wallets and super apps, improving instant accessibility and redemption convenience for consumers.

- Corporate adoption is accelerating, with enterprises using digital gift cards for employee rewards, customer retention, and performance incentives.

- Retail and e-commerce dominate global usage, leveraging digital gift cards to drive customer acquisition and repeat purchases.

- Asia-Pacific is the fastest-growing region due to rapid fintech expansion, UPI-like systems, and rising smartphone penetration.

- AI and personalization technologies are reshaping the market, enabling targeted gifting experiences and higher conversion rates.

- Cross-border digital gifting is expanding, especially across gaming, travel, and subscription-based platforms.

What are the latest trends in the Digital Gift Cards Market?

AI-Driven Personalization and Smart Gifting

Digital gift card platforms are increasingly using artificial intelligence to personalize recommendations based on consumer behavior, purchase history, and demographic data. This is enabling highly targeted gifting experiences where users can automatically receive curated gift suggestions. Retailers and fintech platforms are also leveraging predictive analytics to optimize gifting campaigns, improving engagement and redemption rates. Personalized gifting messages, occasion-based automation, and AI-driven cross-sell recommendations are becoming standard features across leading platforms.

Mobile Wallet and Super App Integration

Integration of digital gift cards into mobile wallets and super apps is transforming consumer accessibility. Platforms such as digital wallets and banking apps now allow users to store, send, and redeem gift cards instantly. QR-based redemption, NFC payments, and in-app gifting are improving user experience significantly. This trend is especially strong in Asia-Pacific, where super apps dominate digital transactions, making gift cards a native feature of daily financial activity.

Blockchain-Enabled Security and Fraud Prevention

Blockchain technology is being adopted to improve transparency, traceability, and fraud protection in digital gift card systems. Tokenized gift cards reduce duplication risks and unauthorized redemption, enhancing consumer trust. Companies are also investing in advanced fraud-detection systems and encrypted APIs to secure transactions across global networks.

What are the key drivers in the Digital Gift Cards Market?

Expansion of Digital Commerce Ecosystems

The rapid growth of e-commerce platforms, subscription services, and online marketplaces is a major driver of digital gift card adoption. Consumers increasingly prefer instant, contactless payment and gifting solutions. Digital gift cards are widely used during festive seasons, promotional campaigns, and online retail events, significantly boosting transaction volumes globally.

Corporate Incentive and Loyalty Program Growth

Enterprises are increasingly adopting digital gift cards as part of employee engagement and customer loyalty strategies. Compared to traditional rewards, digital gift cards offer scalability, instant delivery, and measurable analytics. They are widely used in performance bonuses, referral programs, and customer retention campaigns across industries such as BFSI, IT, and retail.

Rising Adoption of Mobile Wallets and Fintech Platforms

The expansion of mobile wallets and fintech ecosystems is significantly boosting market growth. Digital gift cards are increasingly embedded within payment apps, enabling seamless purchase and redemption. The rise of cashless economies in emerging markets is accelerating adoption, particularly in India, China, Brazil, and Southeast Asia.

What are the restraints for the global market?

Fraud and Cybersecurity Risks

Digital gift cards are vulnerable to fraud, phishing, and unauthorized redemption activities. Cybersecurity threats can undermine consumer trust and increase operational costs for issuers. Companies must invest heavily in encryption, authentication systems, and fraud detection technologies to mitigate these risks.

Regulatory Fragmentation Across Regions

Different countries impose varying regulations on prepaid instruments, taxation rules, and digital payment compliance standards. This lack of global standardization creates challenges for cross-border expansion and increases compliance costs for international providers.

What are the key opportunities in the Digital Gift Cards industry?

Expansion of Cross-Border Digital Gifting

Globalization and international workforce mobility are driving demand for cross-border digital gift cards. Gaming, travel, and subscription-based services are particularly benefiting from multi-currency and globally redeemable gift card systems. Companies that can simplify international compliance and currency conversion are well-positioned for growth.

Growth of Enterprise API-Based Gifting Solutions

Enterprises are increasingly integrating gift card systems directly into CRM, HR, and marketing platforms through APIs. This creates opportunities for scalable B2B gifting solutions that support automation, analytics, and real-time distribution across global organizations.

Integration with Fintech and Embedded Finance Ecosystems

Digital gift cards are becoming a core part of embedded finance strategies within fintech platforms. Mobile wallets, neobanks, and super apps are integrating gifting capabilities to increase user engagement, transaction frequency, and platform retention.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 535 Billion |

| Market Size in 2026 | USD 607.23 Billion |

| Market Size in 2031 | USD 1143.74 Billion |

| CAGR | 13.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Closed-loop digital gift cards continue to dominate the global market, accounting for nearly 64% share in 2025. Their leadership is primarily driven by strong integration within retailer ecosystems, gaming platforms, food delivery apps, and subscription-based services. These cards create a closed spending loop that significantly enhances customer retention, strengthens brand loyalty, and drives repeat purchases, making them highly preferred by large retail chains and digital-first brands. The increasing use of closed-loop systems in loyalty programs and promotional campaigns further reinforces their dominance.

The rapid expansion of digital commerce ecosystems and retailer-owned mobile applications is accelerating closed-loop adoption, as companies seek full control over consumer spending behavior and data analytics. Open-loop digital gift cards, such as Visa and Mastercard-backed products, are gaining traction due to their flexibility and universal acceptance across merchants. These are increasingly used in financial incentives, payroll-linked benefits, and cross-border gifting scenarios. Meanwhile, reloadable and hybrid digital gift cards are emerging strongly in enterprise reward programs, offering long-term usability, recurring funding options, and better engagement tracking for corporate users.

Application Insights

Personal gifting remains the largest application segment, contributing approximately 35% of total market demand in 2025, largely driven by seasonal festivals, birthdays, weddings, and social occasions. The simplicity of instant delivery and personalization has made digital gift cards a preferred choice for consumers globally. Increasing digitization of social interactions and the rising preference for instant, contactless gifting experiences are fueling personal gifting demand.

Employee rewards and corporate incentives represent the fastest-growing application segment, supported by rapid enterprise digital transformation and hybrid work models. Loyalty programs, cashback rewards, gaming credits, and subscription-based gifting are also expanding rapidly, especially within digital entertainment and e-commerce ecosystems. These applications benefit from data-driven targeting and automated distribution systems, improving efficiency and engagement outcomes.

Distribution Channel Insights

Online marketplaces and brand-owned platforms dominate distribution channels, accounting for over 65% of global market share. These platforms offer instant delivery, promotional pricing, and seamless integration with digital wallets, making them the most preferred channel among consumers and enterprises. The rapid rise of mobile-first consumer behavior and embedded payment ecosystems is accelerating the shift toward digital-first distribution models. Mobile wallets and fintech applications are the fastest-growing channels due to their convenience, instant redemption capabilities, and integration with daily financial transactions. Retail aggregator platforms and telecom super apps are also expanding rapidly, particularly in Asia-Pacific, where super app ecosystems dominate digital commerce behavior.

Consumer Type Insights

Individual consumers represent the largest user base, driven by personal gifting, seasonal celebrations, and social occasions. Enterprises are rapidly increasing their adoption of employee engagement, customer loyalty programs, and promotional campaigns. SMEs are emerging as strong adopters due to cost-effective digital reward systems and simplified deployment models, while government agencies are increasingly using digital gift cards for welfare distribution, subsidies, and social benefit programs. The expansion of digital public service delivery and corporate digital engagement strategies is significantly increasing multi-sector adoption.

Age Group Insights

Consumers aged 25–44 years dominate the market due to high digital literacy, strong purchasing power, and frequent use of e-commerce platforms. Younger users aged 18–24 years are driving strong growth in gaming, entertainment, and social gifting categories, supported by influencer marketing and mobile-first engagement. The 45–60 age group prefers retail, travel, and family-oriented gifting solutions, while the above-60 segment is gradually adopting simplified digital gifting via mobile wallets and assisted digital platforms. Increasing digital adoption across all age groups, especially through simplified mobile interfaces and assisted onboarding systems, is expanding the addressable user base.

Explore more data points, trends and opportunities Download Free Sample Report

Digital Gift Cards Market Segmentations

By Product Type

- Closed-Loop Digital Gift Cards

- Open-Loop Digital Gift Cards

- Reloadable Digital Gift Cards

- Hybrid and Multi-Use Digital Gift Cards

By Application

- Personal Gifting

- Employee Rewards and Incentives

- Customer Loyalty and Cashback Programs

- Gaming and Digital Entertainment

- Subscription and Streaming Services

- Refunds and Compensation Programs

By Distribution Channel

- Online Marketplaces

- Brand-Owned Websites and Mobile Apps

- Mobile Wallets and Fintech Platforms

- Retail Aggregator Platforms

- Telecom and Super App Ecosystems

By Consumer Type

- Individual Consumers

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- Government and Public Institutions

By End-Use Industry

- Retail and E-commerce

- Food Service and Restaurants

- Travel and Hospitality

- Gaming and Entertainment

- BFSI

- Healthcare and Wellness

- Education and E-learning

Regional Insights

North America

North America holds the largest market share at approximately 41% in 2025, led by the United States. The region benefits from strong digital payment infrastructure, high e-commerce penetration, and widespread corporate adoption of digital rewards systems. Retail giants, fintech companies, and payment processors are deeply integrated into the digital gifting ecosystem. High consumer spending power, an advanced fintech ecosystem, and a strong corporate incentive culture are driving sustained demand for digital gift cards.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a CAGR exceeding 16%, driven by China, India, Japan, South Korea, and Southeast Asia. The region is characterized by mobile-first economies, super app ecosystems, and rapid fintech adoption. India’s UPI infrastructure and China’s digital wallet dominance are central to market expansion. Rapid smartphone penetration, expansion of digital payment ecosystems, and rising middle-class disposable income are fueling strong adoption across both urban and semi-urban markets.

Europe

Europe accounts for nearly 22% of global demand, with strong contributions from the UK, Germany, and France. The region is characterized by high regulatory compliance, strong digital banking systems, and a growing preference for sustainable and ethical consumption patterns. Retail digitization and subscription-based service growth are key demand drivers. Regulatory support for secure digital payments, rising sustainability-focused consumer behavior, and strong adoption of subscription economy models are driving regional growth.

Latin America

Brazil and Mexico are the leading markets in Latin America, supported by expanding fintech ecosystems and rising e-commerce penetration. Digital gift cards are increasingly used in online retail, gaming, and mobile commerce platforms, particularly among younger demographics. Rapid fintech expansion, increasing financial inclusion, and growing mobile commerce adoption are driving regional market penetration.

Middle East & Africa

The UAE and Saudi Arabia lead regional demand, supported by strong digital transformation initiatives, high smartphone penetration, and luxury retail consumption. Africa is witnessing increasing adoption through mobile-first payment systems and expanding digital retail infrastructure, particularly in South Africa, Nigeria, and Kenya. Government-led digital transformation programs, expansion of mobile payment ecosystems, and rising youth-driven digital consumption are accelerating regional adoption.