Digital Ballasts Market Size

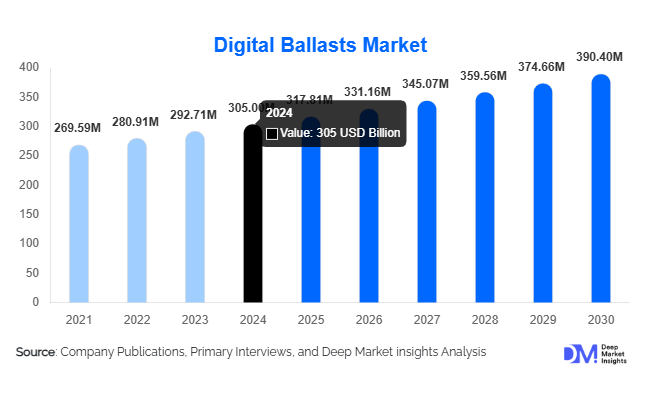

According to Deep Market Insights, the global digital ballasts market size was valued at USD 305.00 million in 2025 and is projected to grow from USD 317.81 million in 2026 to reach USD 390.40 million by 2031, expanding at a CAGR of 4.2% during the forecast period (2026–2031). The market growth is primarily driven by rising demand for energy-efficient lighting solutions, increasing adoption of smart and IoT-enabled lighting systems, and growing infrastructure development in emerging economies.

Key Market Insights

- Energy efficiency is the primary driver of digital ballast adoption, as these systems reduce power consumption and operational costs compared to traditional magnetic ballasts.

- High-frequency and LED-compatible digital ballasts dominate the market, particularly in commercial and industrial applications, due to superior performance and longer lamp life.

- Asia-Pacific is the fastest-growing regional market, driven by rapid urbanization, industrial expansion, and smart city projects in China, India, and Japan.

- Government incentives and regulations promoting energy-efficient lighting solutions in North America and Europe are driving market adoption in public infrastructure and commercial sectors.

- Smart and IoT-enabled digital ballasts are emerging as a critical trend, offering remote monitoring, predictive maintenance, and integration with connected lighting systems.

Digital Ballasts Market Latest Trends

Smart and IoT-Integrated Ballasts

Digital ballasts are increasingly being integrated with IoT-enabled control systems. These smart ballasts allow for remote monitoring, automated dimming, and energy management, improving efficiency and lowering operational costs. Industrial and commercial sectors are adopting such systems to meet sustainability goals and reduce maintenance downtime. Smart ballasts can also provide real-time data on lamp performance, enabling predictive maintenance and reducing replacement costs. The trend aligns with the global push for smart building infrastructure, especially in developed regions such as North America and Europe.

LED Compatibility Driving Adoption

LED-compatible digital ballasts are becoming a dominant choice in commercial and residential sectors. With global adoption of LED lighting increasing due to energy efficiency and environmental considerations, ballasts capable of supporting LED lamps are witnessing strong demand. Upgrading older fluorescent and HID lighting systems with LED-compatible digital ballasts ensures compatibility, reduces energy consumption, and extends lamp lifespan, which has positioned this segment as a market leader globally.

Digital Ballasts Market Drivers

Rising Energy Efficiency and Regulatory Compliance

Government regulations in North America, Europe, and Asia-Pacific are promoting energy-efficient lighting solutions, driving the adoption of digital ballasts. Programs aimed at reducing carbon emissions and achieving ESG goals are encouraging commercial, industrial, and municipal customers to replace legacy magnetic ballasts with digital alternatives.

Infrastructure Expansion and Urbanization

Rapid urbanization in Asia-Pacific, Latin America, and the Middle East is increasing demand for energy-efficient lighting in commercial, industrial, and public infrastructure projects. Digital ballasts are being integrated into smart city initiatives, street lighting upgrades, and large-scale commercial retrofits, driving sustained market growth.

Technological Advancements

Innovations in programmable, dimmable, and IoT-enabled ballasts are creating new opportunities for manufacturers. These advanced products allow users to control lighting intensity, reduce maintenance costs, and integrate with smart building management systems, appealing to modern commercial and industrial applications.

Digital Ballasts Market Restraints

High Initial Investment

Despite long-term energy savings, digital ballasts require a higher upfront investment compared to traditional magnetic ballasts. This can limit adoption among cost-sensitive customers and smaller enterprises, especially in emerging markets.

Compatibility Challenges with Legacy Systems

Older lighting systems may require retrofitting or complete lamp replacement to integrate digital ballasts. This increases installation complexity and costs, potentially slowing down market penetration in regions with widespread legacy infrastructure.

Digital Ballasts Market Key Opportunities

Government Initiatives and Energy Efficiency Programs

Governments worldwide are implementing programs to encourage the adoption of energy-efficient lighting. Digital ballast manufacturers can leverage these incentives to expand installations in public infrastructure projects, including street lighting, airports, and municipal buildings, creating a stable demand pipeline.

Emerging Regional Demand

Rapid urbanization and industrialization in the Asia-Pacific and Latin America are creating significant demand for digital ballasts. Countries like China, India, and Brazil are investing heavily in smart city projects and commercial building upgrades, providing opportunities for local and international manufacturers to capture market share.

Integration with Smart and Connected Lighting Systems

Digital ballasts integrated with IoT and smart lighting solutions are increasingly sought after in commercial and industrial sectors. These systems allow for energy monitoring, automated dimming, and predictive maintenance, which is appealing to large enterprises and smart building projects. Companies investing in R&D for IoT-enabled solutions are well-positioned to capture high-margin contracts.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 305 Million |

| Market Size in 2026 | USD 317.81 Million |

| Market Size in 2031 | USD 390.40 Million |

| CAGR | 4.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Electronic ballasts dominate the market, accounting for approximately 45% of the 2025 market. Their high efficiency, reliability, and compatibility with multiple lamp types make them the preferred choice for commercial and industrial applications. Programmable and dimmable variants are gaining traction due to energy-saving benefits and flexibility in smart lighting projects, while HID-specific ballasts cater to niche outdoor and industrial lighting applications.

Application Insights

The commercial sector leads the global demand for digital ballasts, representing around 40% of the market in 2025. Industrial applications are rapidly growing due to factory modernization, warehouse expansions, and automated lighting systems. Residential adoption is emerging with smart home trends, particularly in North America and Europe, while public infrastructure applications, such as street lighting and municipal buildings, continue to drive steady demand globally.

Distribution Channel Insights

Direct B2B sales dominate the market, accounting for 60% of 2025 revenue, primarily for large-scale commercial and industrial installations. Retail and e-commerce channels are growing, particularly for residential and small commercial projects, driven by digital marketing, online product availability, and easier access to technical support. Strategic partnerships and local manufacturing also play a key role in expanding market reach in emerging economies.

End-Use Insights

Commercial and industrial applications remain the largest end-use segments, driven by cost savings, regulatory compliance, and smart infrastructure integration. Residential adoption is gaining traction due to the rise of smart homes and consumer awareness about energy efficiency. Export-driven demand is notable, with Asia-Pacific emerging as a key supplier to North America, Europe, and Latin America. Industrial lighting alone accounted for around USD 1,200 million in 2025, projected to grow at a CAGR of 8.5% through 2031.

Explore more data points, trends and opportunities Download Free Sample Report

Digital Ballasts Market Segmentations

By Product Type

- Electronic Ballasts

- Programmable Ballasts

- Dimmable Ballasts

By Technology

- High-Frequency Digital Ballasts

- Low-Frequency Digital Ballasts

- Smart & IoT-Enabled Digital Ballasts

By Lamp Type

- Fluorescent Lamp Ballasts

- LED-Compatible Ballasts

- HID Lamp Ballasts

By End Use

- Commercial

- Industrial

- Residential

- Public Infrastructure & Street Lighting

By Distribution Channel

- Direct B2B Sales

- Retail & E-Commerce

Regional Insights

North America

North America accounted for approximately 28% of the global market in 2025. The U.S. and Canada lead demand due to stringent energy efficiency regulations, commercial building upgrades, and smart city projects. Retrofitting old lighting systems and public infrastructure modernization are key growth drivers.

Europe

Europe holds about 25% of the global market, led by Germany, France, and the U.K. High adoption is driven by strict energy codes, green building certifications, and corporate ESG initiatives. The region also emphasizes smart and IoT-enabled lighting systems.

Asia-Pacific

Asia-Pacific is the fastest-growing market, particularly China, India, and Japan, with a CAGR of 9.2%. Urbanization, industrialization, and large-scale infrastructure projects are driving significant adoption. Emerging smart cities and government incentives further accelerate growth.

Middle East & Africa

Demand is led by urban development and smart infrastructure projects in the UAE, Saudi Arabia, and South Africa. Energy efficiency and sustainable lighting solutions are gaining traction in commercial and industrial segments.

Latin America

Brazil and Mexico are leading the adoption in the region due to industrial retrofits and commercial building modernization. Government-backed energy efficiency initiatives are creating incremental opportunities for digital ballast deployment.

Key Players in the Digital Ballasts Market

- Philips Lighting

- OSRAM GmbH

- GE Lighting

- Toshiba Lighting & Technology

- Havells India Ltd

- Tridonic

- Panasonic Lighting

- Zumtobel Group

- Advance Transformer

- Signify

- Sylvania

- Helvar

- Fulham Co.

- Iwasaki Electric

- Acme Electric