Cylinder Stand Market Size

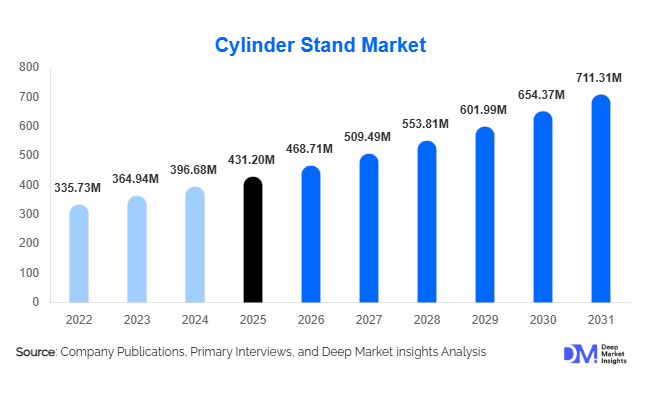

According to Deep Market Insights, the global cylinder stand market size was valued at USD 431.2 million in 2025 and is projected to grow from USD 468.71 million in 2026 to reach USD 711.31 million by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). Market growth is primarily driven by rising industrial gas consumption, expansion of healthcare infrastructure, and increasing enforcement of workplace safety regulations worldwide. Cylinder stands are essential safety and storage equipment designed to stabilize compressed gas cylinders, prevent workplace accidents, and ensure regulatory compliance across industrial, medical, and commercial environments.

Key Market Insights

- Industrial gas usage expansion across manufacturing, fabrication, and energy sectors continues to drive steady demand for cylinder storage safety equipment.

- Healthcare infrastructure investments following global oxygen supply modernization initiatives are accelerating adoption of medical-grade cylinder stands.

- Asia-Pacific dominates global demand, supported by strong manufacturing output and rapid infrastructure development.

- Mobile and ergonomic cylinder stands are gaining popularity, improving operational flexibility in hospitals and industrial facilities.

- Steel-based stands remain the preferred material due to durability, affordability, and high load-bearing capacity.

- Regulatory compliance requirements from occupational safety agencies are transforming cylinder stands from optional accessories into mandatory equipment.

What are the latest trends in the cylinder stand market?

Shift Toward Mobile and Modular Storage Solutions

Industries are increasingly adopting mobile cylinder stands and modular rack systems that allow flexible movement and efficient space utilization. Hospitals and fabrication workshops prefer wheeled solutions that enable safe transportation of cylinders without manual lifting risks. Modular designs allow scalability as facilities expand gas usage capacity, reducing infrastructure redesign costs. Manufacturers are introducing adjustable frames and expandable racks capable of accommodating different cylinder sizes, improving long-term usability and lowering replacement frequency.

Adoption of Corrosion-Resistant and Safety-Engineered Designs

Modern cylinder stands increasingly incorporate powder-coated steel, stainless steel construction, and anti-slip stabilization mechanisms to improve durability and compliance with safety standards. Demand is rising for products capable of operating in harsh environments such as offshore energy facilities, chemical plants, and humid hospital environments. Enhanced safety features such as chain-lock systems, anti-tip bases, and ergonomic handling structures are becoming standard design requirements, particularly in developed markets where compliance enforcement is strict.

What are the key drivers in the cylinder stand market?

Growing Industrial Gas Consumption

The rapid expansion of manufacturing industries including automotive, metal fabrication, electronics, and construction has significantly increased demand for compressed industrial gases such as oxygen, nitrogen, and acetylene. As gas usage rises, safe storage infrastructure becomes essential, directly boosting adoption of cylinder stands across industrial facilities. Expansion of export-oriented manufacturing economies in Asia further strengthens long-term demand.

Healthcare Infrastructure Expansion

Global healthcare systems are investing heavily in medical gas storage and oxygen delivery infrastructure. Hospitals, diagnostic centers, and emergency care facilities require secure positioning of cylinders to comply with safety standards. Rising healthcare spending in emerging economies and hospital modernization initiatives in developed countries are accelerating procurement of medical cylinder stands.

Increasing Workplace Safety Regulations

Occupational safety authorities worldwide are tightening guidelines regarding compressed gas storage. Insurance providers and compliance auditors increasingly mandate proper cylinder stabilization equipment. This regulatory shift has transformed cylinder stands into compliance-driven purchases, ensuring recurring replacement demand across industries.

What are the restraints for the global market?

Commodity Nature and Price Competition

Cylinder stands are often perceived as standardized industrial accessories, leading buyers to prioritize price over innovation. This limits product differentiation and compresses manufacturer profit margins, particularly in cost-sensitive markets where local producers compete aggressively.

Raw Material Price Volatility

Steel represents a major portion of manufacturing costs. Fluctuations in global steel prices directly affect pricing stability and profitability. Smaller manufacturers face challenges maintaining margins during raw material cost spikes, especially under long-term supply contracts.

What are the key opportunities in the cylinder stand industry?

Healthcare Gas Infrastructure Modernization

Expansion of hospitals and emergency preparedness infrastructure worldwide presents strong growth opportunities. Governments are investing in oxygen storage capacity and modular medical facilities, creating sustained demand for certified medical cylinder stands. Suppliers capable of delivering hygienic, corrosion-resistant designs are expected to benefit significantly.

Smart and Integrated Storage Systems

Emerging applications in semiconductor manufacturing and specialty gas handling are creating demand for intelligent storage solutions integrated with monitoring capabilities. IoT-enabled tracking systems that monitor cylinder inventory and safety status are gaining attention among advanced industrial buyers, opening premium product opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 431.2 Million |

| Market Size in 2026 | USD 468.71 Million |

| Market Size in 2031 | USD 711.31 Million |

| CAGR | 8.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Mobile cylinder trolleys and stands dominate the global cylinder stand market, accounting for nearly 32% of total market share in 2025, primarily driven by the increasing need for operational mobility, workplace safety compliance, and efficient cylinder handling across industrial and healthcare environments. The leading position of this segment is supported by growing adoption in manufacturing facilities where frequent cylinder movement between workstations is required to maintain production continuity. Additionally, stricter occupational safety standards encouraging secure transportation and reduced manual handling risks have accelerated the replacement of traditional storage methods with mobile solutions.

Single-cylinder stands continue to maintain strong demand in small-scale workshops, clinics, and laboratories where space constraints and limited gas consumption favor compact storage formats. Meanwhile, multi-cylinder storage racks are witnessing increasing deployment in large industrial plants and centralized gas distribution facilities handling high gas volumes, particularly within welding, metal fabrication, and chemical processing operations. Wall-mounted cylinder stands are gaining traction in laboratories and modern healthcare environments where floor space optimization and organized infrastructure layouts are critical operational priorities. Heavy-duty industrial racks continue to experience steady growth due to expanding large-scale manufacturing operations that require high-capacity storage systems capable of supporting safety compliance and long-term durability.

Material Insights

Steel cylinder stands lead the market with approximately 68% share in 2025, driven by their superior structural strength, affordability, and ability to withstand heavy industrial usage. The dominance of steel-based products is largely attributed to their high load-bearing capacity and compatibility with diverse industrial environments, making them the preferred choice for manufacturing, oil & gas, and logistics applications. Increasing investments in industrial safety infrastructure have further strengthened adoption, as steel stands provide enhanced stability and long service life, reducing maintenance and replacement costs.

Stainless steel variants hold a significant position within healthcare, pharmaceutical, and laboratory applications where corrosion resistance, hygiene standards, and sterilization compatibility are essential. Hospitals and research facilities increasingly prioritize stainless steel solutions to meet infection-control regulations and long-term durability requirements. Aluminum and composite materials are gradually emerging in portable and lightweight applications, particularly in emergency medical response systems and mobile industrial operations. However, widespread adoption remains limited due to higher material costs and lower structural robustness compared to traditional steel solutions, although technological advancements in lightweight engineering are expected to support future penetration.

End-Use Industry Insights

Manufacturing and metal fabrication represent the largest end-use segment, contributing over 40% of total market demand, supported by continuous welding activities and sustained industrial gas consumption across automotive, construction, and heavy engineering industries. The leading position of this segment is driven by rising automation levels and expanding production capacities that require organized gas storage systems to ensure uninterrupted operations and worker safety. Increasing adoption of industrial safety certifications and compliance-driven procurement policies further reinforces demand for standardized cylinder stands within manufacturing facilities.

Healthcare is emerging as the fastest-growing end-use segment, expanding at nearly 10% CAGR as hospitals upgrade oxygen delivery infrastructure, expand intensive care capacity, and strengthen emergency preparedness systems. The long-term impact of healthcare infrastructure modernization programs and growing investments in medical gas management systems continues to create sustained demand for secure cylinder storage solutions. Oil & gas facilities require explosion-resistant and high-stability storage systems to support hazardous operating environments, while research laboratories and semiconductor manufacturing facilities are developing into niche but high-value demand centers due to their reliance on specialty gases. Additionally, export-oriented manufacturing economies are driving equipment purchases as industrial output expansion increases the need for safe gas handling systems.

Distribution Channel Insights

Direct industrial procurement dominates the distribution landscape, accounting for nearly half of total sales, as large enterprises increasingly purchase cylinder stands through long-term supplier contracts aligned with workplace safety and compliance budgets. Bulk procurement strategies allow organizations to standardize equipment specifications while reducing operational risk and procurement costs. The leading position of direct sales is further supported by customized product requirements and integrated industrial safety solutions offered by manufacturers.

Distributor networks continue to play a critical role in regional markets, particularly among small and medium-sized enterprises that rely on localized supply chains and technical consultation services. Simultaneously, B2B e-commerce platforms are rapidly gaining traction by providing transparent pricing, product comparisons, and faster delivery timelines, enabling buyers to streamline procurement processes. OEM supply agreements are also expanding steadily, especially within healthcare infrastructure projects and industrial equipment installations where cylinder stands are supplied as part of integrated system packages, contributing to stable long-term revenue channels for manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

Cylinder Stand Market Segmentations

By Product Type

- Single Cylinder Stands

- Dual Cylinder Stands

- Multi-Cylinder Storage Stands

- Mobile Cylinder Trolleys/Stands

- Wall-Mounted Cylinder Stands

- Heavy-Duty Industrial Cylinder Racks

By Material Type

- Steel Cylinder Stands

- Aluminum Cylinder Stands

- Polymer/Composite Cylinder Stands

- Hybrid Material Stands

By End-Use Industry

- Healthcare & Hospitals

- Manufacturing & Metal Fabrication

- Oil & Gas & Energy

- Residential & Commercial LPG Usage

- Laboratories & Research Institutions

- Fire Protection & Safety Infrastructure

By Distribution Channel

- Direct Industrial Procurement

- OEM Supply Contracts

- Distributor & Industrial Retail

- E-commerce & B2B Platforms

Regional Insights

Asia-Pacific

Asia-Pacific leads the global cylinder stand market with approximately 38% share in 2025, supported by rapid industrialization, expanding healthcare infrastructure, and growing adoption of industrial safety practices across emerging economies. China dominates regional demand due to its vast manufacturing ecosystem and large-scale industrial gas consumption across steel, automotive, and electronics sectors. India is emerging as the fastest-growing market with nearly 11% CAGR, driven by healthcare expansion, increasing LPG penetration, infrastructure development, and government initiatives promoting industrial safety compliance. Japan and South Korea contribute significantly through advanced manufacturing and semiconductor industries requiring precision gas storage systems. Additionally, rising foreign investments, export-driven production growth, and urban industrial expansion continue to strengthen regional demand momentum.

North America

North America accounts for nearly 26% of global demand, supported by stringent workplace safety regulations, mature industrial infrastructure, and high replacement demand cycles. The United States leads adoption due to continuous modernization of healthcare facilities, strong enforcement of occupational safety standards, and widespread adoption of standardized industrial equipment. Increasing automation in manufacturing and growing investments in energy and specialty gas applications further support regional growth. The presence of established industrial gas suppliers and advanced logistics networks also enhances product accessibility and consistent replacement demand.

Europe

Europe holds roughly 22% market share, led by Germany, France, and the United Kingdom, where strict regulatory enforcement and strong emphasis on worker safety drive adoption of certified cylinder storage solutions. The region benefits from well-established industrial manufacturing clusters and advanced healthcare systems requiring compliant gas handling infrastructure. Sustainability initiatives and modernization of industrial facilities are encouraging companies to upgrade legacy storage equipment with safer and more durable solutions. Additionally, growing investments in renewable energy, research laboratories, and specialty manufacturing sectors are contributing to stable long-term demand growth.

Latin America

Latin America represents about 7% of the global market, with Brazil and Mexico acting as primary growth engines due to expanding manufacturing activities and increasing commercial LPG adoption. Industrial development programs, improving healthcare accessibility, and rising investments in construction and automotive production are strengthening regional demand. Gradual improvement in workplace safety awareness and modernization of industrial facilities are also encouraging adoption of standardized cylinder storage equipment across the region.

Middle East & Africa

The Middle East & Africa region contributes close to 7% market share, supported by strong oil & gas investments, expanding healthcare infrastructure, and industrial diversification initiatives across GCC countries. Growth is driven by increasing demand for safe gas handling solutions in petrochemical operations and energy projects. Government-led economic diversification strategies aimed at developing manufacturing and healthcare sectors are creating new opportunities for cylinder stand adoption. Additionally, rising infrastructure development and medical facility expansion across Africa are expected to gradually accelerate regional market penetration over the forecast period.

Key Players in the Cylinder Stand Market

- Justrite Safety Group

- DENIOS AG

- Eagle Manufacturing Company

- Vestil Manufacturing Corporation

- Gas Cylinder Source Inc.

- Armorgard Ltd.

- Nilkamal Material Handling

- Quantum Storage Systems

- Saf-T-Cart Inc.

- Stronghold Manufacturing

- Nexel Industries

- Little Giant (Brennan Equipment)

- Global Industrial Company

- Stanley Black & Decker

- Equipto Electronics Corporation