Cutlery Holder Market Size

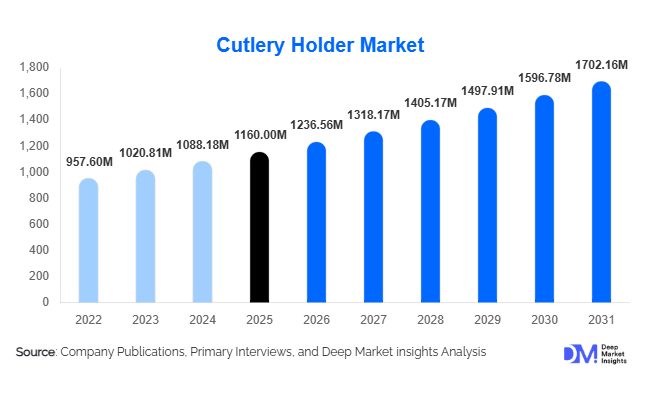

According to Deep Market Insights, the global cutlery holder market size was valued at USD 1,160 million in 2025 and is projected to grow from USD 1,236.56 million in 2026 to reach USD 1,702.16 million by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). Market growth is primarily driven by increasing adoption of modular kitchens, rising consumer focus on kitchen organization and hygiene, and expanding demand from the hospitality and foodservice sectors worldwide. The growing popularity of aesthetically designed kitchen accessories, combined with rapid expansion of e-commerce retail channels, is enabling manufacturers to reach broader consumer bases globally. Additionally, sustainability trends encouraging the use of bamboo, recycled plastics, and durable stainless-steel materials are reshaping product innovation and purchasing decisions.

Key Market Insights

- Kitchen organization trends are accelerating global demand, supported by rising urbanization and smaller living spaces requiring efficient storage solutions.

- Residential households dominate market consumption, accounting for the largest share due to modular kitchen adoption and home improvement spending.

- Asia-Pacific leads global production and consumption, driven by strong manufacturing capacity and expanding middle-class demand.

- E-commerce platforms are the fastest-growing distribution channel, enabling wider product variety and competitive pricing.

- Sustainable materials such as bamboo and recycled plastics are gaining traction as consumers shift toward eco-friendly kitchenware.

- Hospitality and institutional kitchens are emerging growth drivers, increasing demand for durable commercial-grade cutlery holders.

What are the latest trends in the cutlery holder market?

Shift Toward Sustainable and Eco-Friendly Kitchen Accessories

Sustainability has become a defining trend across the kitchenware industry, influencing the cutlery holder market significantly. Consumers increasingly prefer environmentally responsible materials such as bamboo, biodegradable composites, and recycled plastics. Manufacturers are responding by introducing eco-certified products that reduce environmental impact while maintaining durability and functionality. European and North American markets particularly favor sustainable kitchen accessories, encouraging brands to redesign product portfolios around recyclable packaging and renewable materials. This shift is also strengthening brand differentiation in a highly competitive market where product functionality alone offers limited competitive advantage.

Design-Led Innovation and Modular Storage Solutions

Modern consumers seek kitchen accessories that combine functionality with aesthetics. As modular kitchens gain popularity globally, cutlery holders are being designed to integrate seamlessly into drawers, countertops, and wall-mounted storage systems. Expandable organizers, multi-compartment layouts, and space-saving configurations are becoming standard features. Premium brands are introducing minimalist designs aligned with contemporary kitchen interiors, while smart drainage systems and antimicrobial coatings enhance hygiene. These innovations are expanding the role of cutlery holders from simple storage tools to design-oriented kitchen essentials.

What are the key drivers in the cutlery holder market?

Rapid Expansion of Modular Kitchens

The global rise of modular kitchens is a major growth driver for the cutlery holder market. Urban households increasingly prioritize organized kitchen layouts that maximize storage efficiency. Drawer organizers and compartmentalized holders have become essential components of modern kitchen installations. Growth in residential construction, apartment living, and renovation activities is fueling sustained demand for integrated storage accessories worldwide.

Growth of the Global Foodservice Industry

The expansion of restaurants, quick-service chains, hotels, and catering services has significantly increased demand for commercial-grade cutlery holders. Foodservice operators require hygienic and durable utensil storage solutions capable of handling high-volume usage. Emerging economies across Asia-Pacific and the Middle East are witnessing rapid restaurant expansion, contributing to consistent demand growth in institutional kitchen accessories.

What are the restraints for the global market?

Limited Product Differentiation and Pricing Pressure

The market remains highly fragmented with numerous regional and international manufacturers offering similar products. Limited technological complexity results in intense price competition, particularly in plastic-based products. This reduces profit margins and creates challenges for premium positioning unless supported by strong branding or innovative design features.

Volatility in Raw Material Prices

Fluctuations in prices of plastic resins, stainless steel, and wood directly impact manufacturing costs. Smaller producers often struggle to absorb cost increases, leading to pricing instability. Supply chain disruptions and commodity price volatility remain ongoing challenges that can temporarily slow market expansion.

What are the key opportunities in the cutlery holder industry?

Expansion of Eco-Friendly Product Lines

The growing global emphasis on sustainability presents significant opportunities for manufacturers introducing biodegradable and renewable-material cutlery holders. Bamboo products, in particular, are gaining popularity due to durability and natural antimicrobial properties. Companies investing in sustainable manufacturing practices can capture premium consumer segments and strengthen brand loyalty.

Growth of Direct-to-Consumer and Online Retail

E-commerce growth is transforming distribution strategies within the kitchenware industry. Direct-to-consumer channels enable brands to showcase diverse designs and reach international customers without extensive retail infrastructure. Digital marketing, influencer-led promotion, and customization options are improving consumer engagement and boosting online sales volumes.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1160 Million |

| Market Size in 2026 | USD 1236.56 Million |

| Market Size in 2031 | USD 1702.16 Million |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Drawer cutlery organizers dominate the global cutlery holder market, accounting for nearly 34% of total market share in 2025, primarily driven by the rapid expansion of modular kitchen installations and growing consumer emphasis on structured storage solutions. The leading position of this segment is supported by increasing urban apartment living, where space optimization and efficient compartmentalization are essential. Modern households are increasingly adopting integrated kitchen systems that prioritize cleanliness, accessibility, and ergonomic design, making drawer-based organizers a preferred solution. Additionally, manufacturers are introducing adjustable compartments, anti-slip materials, and expandable formats that enhance functionality and customization, further strengthening segment demand.Countertop and sink-side holders continue to maintain steady adoption, particularly in traditional kitchens and rental housing environments where built-in storage is limited. These products appeal to consumers seeking convenience and immediate accessibility without permanent installation. Meanwhile, portable cutlery caddies are witnessing accelerating demand across foodservice environments, catering businesses, outdoor dining setups, and quick-service restaurants, supported by the global expansion of takeaway culture and casual dining formats. The growing focus on kitchen organization, combined with lifestyle shifts toward compact living and multifunctional storage solutions, continues to reinforce the long-term dominance of drawer organizers within the product landscape.

Material Insights

Plastic cutlery holders hold the largest share of the global market, contributing approximately 46% of total revenue in 2025. The leadership of this segment is primarily driven by cost efficiency, lightweight construction, wide product variety, and scalability in mass manufacturing. Plastic materials enable flexible molding designs, vibrant color options, and affordability, making them highly attractive for price-sensitive residential consumers and emerging markets. The segment also benefits from strong retail penetration across supermarkets, discount stores, and online platforms, ensuring widespread availability.Stainless steel cutlery holders are experiencing robust growth, particularly within commercial kitchens and institutional environments where durability, corrosion resistance, and hygiene standards are critical purchasing factors. The increasing emphasis on food safety compliance and long product life cycles in restaurants and hospitality establishments is accelerating adoption of metal-based solutions. Simultaneously, bamboo and other eco-friendly materials are gaining popularity as premium alternatives aligned with sustainability-driven consumer behavior. Rising environmental awareness, government regulations encouraging recyclable materials, and brand positioning around eco-conscious living are gradually reshaping material preferences, pushing manufacturers toward biodegradable and renewable raw materials.

Distribution Channel Insights

E-commerce platforms accounted for nearly 29% of global sales in 2025 and represent the fastest-growing distribution channel, supported by rapid digitalization of retail and increasing consumer confidence in online purchasing. The leading driver for this segment is the convenience offered by digital marketplaces, where consumers can easily compare product features, pricing, user reviews, and design variations before making purchasing decisions. The availability of doorstep delivery, promotional discounts, and extensive product assortments has significantly accelerated online adoption across both developed and emerging markets.Offline channels, including supermarkets, hypermarkets, and specialty kitchenware stores, continue to play a crucial role, particularly in regions where tactile product evaluation remains important. Physical retail outlets benefit from impulse purchasing behavior and bundled kitchenware promotions. In developing economies, organized retail expansion and improving supply chain infrastructure are supporting continued relevance of brick-and-mortar distribution. The growing integration of omnichannel strategies—where brands combine online visibility with offline retail presence—is further strengthening overall market penetration.

End-Use Insights

Residential households represent the largest end-use segment, contributing approximately 58% of total market demand. The leading driver behind this dominance is the increasing consumer focus on home organization, kitchen aesthetics, and efficient storage management. Rising disposable incomes, growth in home renovation activities, and the influence of social media-driven interior design trends are encouraging consumers to invest in functional kitchen accessories. Urbanization and smaller living spaces are also prompting households to adopt structured storage products that maximize usability without increasing kitchen footprint.The HoReCa (Hotels, Restaurants, and Cafés) sector is the fastest-growing application segment, expanding at over 7% annually. Rapid restaurant proliferation, tourism recovery, and the expansion of quick-service restaurant chains are driving demand for durable and easy-to-clean cutlery organization systems. Institutional kitchens, including hospitals, corporate cafeterias, and educational facilities, are generating consistent demand due to high-volume food preparation requirements and strict hygiene standards. Growth in large-scale foodservice operations globally continues to create opportunities for heavy-duty and high-capacity cutlery storage solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Cutlery Holder Market Segmentations

By Product Type

- Countertop Cutlery Holders

- Drawer Cutlery Organizers

- Wall-Mounted Cutlery Holders

- Portable/Tabletop Cutlery Caddies

- Sink-Side Cutlery Drying Holders

By Material

- Plastic

- Stainless Steel

- Aluminum

- Bamboo / Wooden Cutlery Holders

- Ceramic Cutlery Holders

- Silicone / Rubber Composite Holders

By Distribution Channel

- Online Retail / E-Commerce

- Supermarkets and Hypermarkets

- Specialty Kitchenware Stores

- Home Improvement Stores

- Institutional and Wholesale Supply

By End Use

- Residential Households

- Hotels and Restaurants

- Catering and Event Services

- Office Pantries

- Institutional Kitchens

Regional Insights

Asia-Pacific

Asia-Pacific leads the global cutlery holder market with approximately 38% market share in 2025, supported by both strong manufacturing capabilities and expanding consumer demand. China remains the dominant production hub due to cost-efficient manufacturing ecosystems, integrated supply chains, and large export volumes. Regional growth is primarily driven by rapid urbanization, rising middle-class populations, and increasing adoption of modular kitchens across metropolitan areas. In India and Southeast Asia, improving living standards and expanding residential construction activities are accelerating household spending on kitchen organization products. Additionally, the rise of e-commerce platforms and affordable product availability is enabling deeper market penetration into tier-2 and tier-3 cities. Japan and South Korea contribute significantly through demand for premium, minimalist, and design-oriented kitchen accessories, supported by strong consumer preference for high-quality home organization solutions.

North America

North America accounts for nearly 27% of global demand, led by the United States, where strong consumer purchasing power and established home improvement culture support sustained market expansion. Regional growth is driven by increasing investments in kitchen remodeling, rising adoption of smart storage solutions, and growing awareness of home organization trends. Consumers increasingly prioritize premium-quality, aesthetically refined kitchen accessories that align with modern interior design standards. Sustainability initiatives and demand for eco-friendly household products are encouraging adoption of bamboo and recyclable-material cutlery holders. Furthermore, the strong presence of organized retail networks and advanced e-commerce infrastructure continues to enhance product accessibility and innovation adoption across the region.

Europe

Europe represents around 24% of the global market, with Germany, the United Kingdom, France, and Italy serving as key demand centers. Regional growth is strongly influenced by sustainability regulations, environmentally conscious consumer behavior, and preference for long-lasting household products. European consumers place significant emphasis on product aesthetics, minimalist design, and material quality, encouraging manufacturers to develop premium and eco-friendly offerings. Increasing renovation of older residential kitchens, combined with rising adoption of compact urban living solutions, is further stimulating demand for organized storage accessories. The region also benefits from a mature hospitality sector that requires durable and hygienic kitchen organization products.

Middle East & Africa

The Middle East & Africa market is experiencing steady expansion, primarily driven by rapid growth in hospitality and tourism infrastructure. Countries such as the UAE and Saudi Arabia are investing heavily in hotels, restaurants, and large-scale entertainment developments, which is increasing demand for commercial kitchen equipment and accessories. Rising urban populations, expanding expatriate communities, and growing adoption of modern retail formats are also supporting residential demand. Additionally, increasing disposable income levels and lifestyle modernization are encouraging consumers to adopt organized kitchen solutions aligned with contemporary housing developments.

Latin America

Latin America demonstrates moderate yet stable growth, with Brazil and Mexico leading regional demand. Urbanization, improving economic stability, and expansion of organized retail chains are key drivers supporting kitchenware consumption. Growth in middle-income households and rising interest in home improvement products are encouraging adoption of practical kitchen organization solutions. Increasing penetration of online retail platforms is also improving product availability across secondary cities. Although price sensitivity remains a key market characteristic, manufacturers are expanding affordable product portfolios to capture rising consumer demand while maintaining steady long-term regional expansion.