Cut Flower Market Size

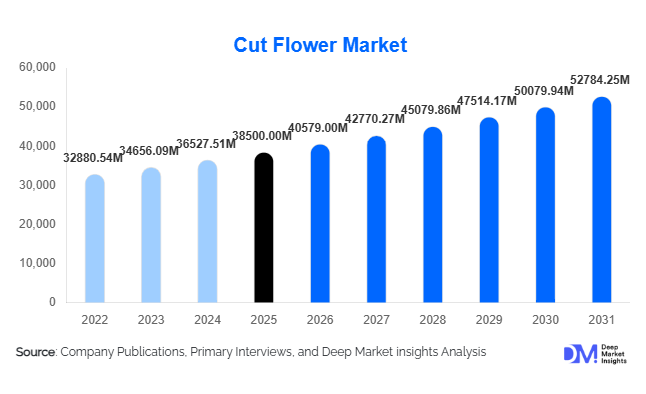

According to Deep Market Insights, the global cut flower market size was valued at USD 38,500 million in 2025 and is projected to grow from USD 40,579.00 million in 2026 to reach USD 52,784.25 million by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The cut flower market growth is primarily driven by rising global demand for decorative and gifting purposes, expanding wedding and event expenditures, increasing household spending on aesthetic home décor, and the rapid expansion of organized retail and e-commerce floral platforms.

The industry operates within a highly globalized supply chain, with production concentrated in export-oriented countries such as the Netherlands, Colombia, Ecuador, Kenya, China, and India, while demand is strongest across North America and Europe. Technological advancements in greenhouse cultivation, hydroponics, cold-chain logistics, and digital distribution channels are enhancing flower quality, extending vase life, and reducing supply chain losses. The growing consumer inclination toward premium, exotic, and sustainably sourced flowers is further reshaping competitive positioning across major producing regions.

Key Market Insights

- Roses account for nearly 32% of global revenue, maintaining dominance due to year-round demand across weddings, gifting, and festive occasions.

- Greenhouse cultivation represents approximately 60% of global production, driven by climate control, consistent quality, and export compliance.

- Europe leads with nearly 38% market share, supported by the Netherlands’ role as the global trading hub.

- North America holds around 26% of global demand, with the U.S. being the largest importing country worldwide.

- Asia-Pacific is the fastest-growing region, with India and China expanding at a 7–8% CAGR due to rising middle-class spending and wedding demand.

- Online floral retail is growing above 8% CAGR, outpacing traditional florist channels through subscription and direct-to-consumer models.

What are the latest trends in the cut flower market?

Sustainable and Certified Flower Production

Sustainability has become a defining trend in the cut flower industry, particularly across Europe and North America. Retailers and institutional buyers increasingly require certifications related to fair trade, carbon neutrality, water management, and ethical labor practices. Exporters in Kenya, Colombia, and Ecuador are investing in renewable energy-powered greenhouses, water recycling systems, and biodegradable packaging. Supermarket chains are also integrating sustainability labeling to guide environmentally conscious consumers. This shift toward responsible sourcing is allowing premium growers to command price premiums of 10–15% while strengthening long-term supply contracts with multinational retailers.

Digitalization and Subscription-Based Floral Services

E-commerce platforms and subscription-based flower delivery models are transforming traditional distribution structures. Consumers increasingly prefer online ordering with same-day or next-day delivery, especially in urban centers. Subscription services offering weekly or monthly bouquets are generating predictable recurring revenue streams and reducing demand volatility. AI-powered inventory forecasting and route optimization are helping companies reduce wastage, which can otherwise reach 20–30% in perishable flower supply chains. Social media marketing and influencer-driven floral aesthetics are further stimulating impulse purchases and premium bouquet demand.

What are the key drivers in the cut flower market?

Rising Wedding and Event Industry Expenditure

The global wedding and events industry continues to expand, with floral décor representing 8–12% of total event budgets in developed markets. Destination weddings, luxury corporate events, and large-scale cultural festivals are driving high-volume demand for roses, lilies, orchids, and specialty flowers. Floral arrangements are increasingly customized, raising average per-event spending and supporting mid- to premium-tier varieties.

Urbanization and Lifestyle Aesthetics

Rapid urbanization and rising disposable income are encouraging household spending on decorative products. Flowers are increasingly used for home décor, workspace enhancement, and gifting occasions throughout the year. Social media platforms showcasing interior aesthetics have normalized frequent flower purchases beyond traditional holidays, strengthening repeat demand cycles.

What are the restraints for the global market?

High Perishability and Supply Chain Risks

Cut flowers are highly perishable, requiring strict temperature-controlled logistics from farm to retail. Any disruption in air freight, customs clearance, or cold storage can result in significant losses. Export-dependent countries face heightened vulnerability to transportation bottlenecks and geopolitical trade disruptions.

Volatile Freight and Energy Costs

Air cargo expenses and greenhouse gas emissions significantly influence profit margins. Rising fuel prices and electricity tariffs in major producing nations directly impact production costs, creating pricing pressures across global markets.

What are the key opportunities in the cut flower industry?

Emerging Demand in Asia-Pacific and the Middle East

Growing middle-class populations in India, China, Indonesia, the UAE, and Saudi Arabia are fueling increased demand for wedding décor, hospitality installations, and corporate gifting. Luxury tourism growth in Dubai and Southeast Asia is expanding premium flower consumption. Local greenhouse investments in these regions are creating import substitution opportunities while reducing supply lead times.

Technology-Driven Greenhouse Expansion

Investment in hydroponics, vertical farming, AI-driven irrigation systems, and climate-controlled greenhouses is enhancing productivity and yield consistency. Countries promoting protected cultivation under agricultural modernization programs are encouraging domestic production, reducing import dependency, and improving export competitiveness.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 38500 Million |

| Market Size in 2026 | USD 40579 Million |

| Market Size in 2031 | USD 52784.25 Million |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Roses continue to dominate the global cut flower market, accounting for nearly 32% of total revenue in 2025. Their leadership is primarily driven by universal cultural symbolism, strong seasonal spikes during Valentine’s Day and Mother’s Day, and high-volume demand from weddings and corporate gifting. The standardized grading system for roses, strong export infrastructure in Colombia, Ecuador, and Kenya, and year-round greenhouse cultivation further reinforce their global leadership. Additionally, premium long-stem and specialty-colored rose varieties command higher margins, strengthening revenue contribution within both retail and event segments.

Carnations and chrysanthemums hold a stable position within the mid-range category due to their affordability, longer vase life, and resilience during transportation. These flowers are widely preferred by supermarkets and mass retailers, supporting their strong volume sales globally. Lilies, tulips, orchids, and gerberas represent the premium and decorative segments, particularly favored in luxury hospitality installations and high-end events. Meanwhile, exotic flowers such as peonies and hydrangeas are witnessing growing demand in high-income markets across North America, Europe, and Japan, driven by social media trends and bespoke floral arrangements. Although premium flowers deliver higher per-unit profitability, the mid-range mass-market segment accounts for approximately 45% of overall sales, benefiting from high retail turnover and supermarket penetration.

Application Insights

Weddings and social events remain the largest application segment, accounting for nearly 28% of global demand in 2025. The segment’s leadership is supported by rising global wedding expenditures, destination ceremonies, and increasing floral budgets that often represent 8–12% of total event costs in developed markets. Premium flower selections, customized installations, and thematic décor have further expanded average spending per event.

Personal household decorative use holds approximately 25% market share, driven by urbanization, rising disposable incomes, and lifestyle-driven interior aesthetics. Social media trends and increased work-from-home arrangements have normalized frequent flower purchases for home ambiance enhancement. Corporate gifting and institutional décor are expanding steadily, particularly through subscription-based floral arrangements for offices, hotels, and commercial spaces. Sympathy and funeral services remain consistent demand drivers in Europe and North America, ensuring year-round stability. Seasonal festivals, including Valentine’s Day, Mother’s Day, Lunar New Year, and regional cultural celebrations, generate substantial short-term revenue spikes, contributing significantly to annual turnover.

Distribution Channel Insights

Traditional florists lead the market with approximately 35% share in 2025, supported by customization capabilities, direct relationships with event planners, and expertise in premium arrangements. Their ability to provide bespoke services and last-minute deliveries ensures continued dominance, particularly in weddings and corporate events.

Supermarkets and hypermarkets maintain a strong presence in the mid-range segment, leveraging bundled bouquet offerings, competitive pricing, and impulse purchasing behavior. However, online channels are the fastest-growing distribution segment, expanding at over 8% CAGR. Growth is fueled by digital marketing, same-day delivery infrastructure, subscription-based models, and AI-driven demand forecasting that reduces spoilage. Wholesale auctions remain central to international trade flows, especially in the Netherlands, where auction systems provide global price discovery and large-scale procurement access for retailers worldwide.

End-Use Industry Insights

Retail consumers account for nearly 40% of total market demand, making them the largest end-use group. Growth in this segment is driven by gifting traditions, lifestyle-driven décor purchases, and the increasing penetration of online flower subscriptions. Event management companies represent a substantial portion of demand due to large-scale installations for weddings, conferences, and exhibitions.

The hospitality industry, encompassing hotels, luxury resorts, cruise lines, and premium restaurants, is among the fastest-growing end-use sectors, expanding at an approximate 6–7% CAGR. Hospitality-driven demand is particularly strong in tourism hubs such as Dubai, Paris, New York, and Bali, where floral aesthetics are integral to brand positioning. Corporate offices and institutional buyers are increasingly adopting recurring subscription models for workspace decoration. Export-driven demand remains critical to market stability, with over 40% of global production traded internationally, led by imports from the United States, Germany, and the United Kingdom.

Explore more data points, trends and opportunities Download Free Sample Report

Cut Flower Market Segmentations

By Product Type

- Roses

- Carnations

- Chrysanthemums

- Lilies

- Tulips

- Gerberas

- Orchids

- Others

By Application

- Weddings & Social Events

- Personal/Household Decorative Use

- Corporate Gifting & Institutional Décor

- Festivals & Cultural Celebrations

- Sympathy & Funeral Services

By Distribution Channel

- Traditional Florists

- Supermarkets & Hypermarkets

- Online & E-commerce Platforms

- Wholesale Flower Auctions

- Direct-to-Event Planners/Corporate Buyers

By End-Use Industry

- Retail Consumers (B2C)

- Event Management Companies

- Hospitality (Hotels, Resorts, Cruise Lines)

- Corporate Offices & Institutions

- Religious Institutions

By Price Tier

- Premium/Exotic Varieties

- Mid-Range Varieties

- Mass-Market/Standard Varieties

Regional Insights

Europe

Europe accounts for nearly 38% of global demand in 2025, making it the largest regional market. The Netherlands acts as the global trading hub, supported by advanced greenhouse infrastructure, automated auction systems, and strong export logistics. Germany represents the largest consumer market in Europe, driven by high per capita flower spending and strong retail supermarket penetration. The U.K. and France also demonstrate robust retail demand, supported by established gifting traditions and sustainability-focused consumer behavior. Regulatory emphasis on fair-trade certification, carbon neutrality, and eco-friendly packaging further drives premium imports and sustainable production investments across the region.

North America

North America holds approximately 26% market share, led by the United States, which contributes nearly 85% of regional demand and stands as the world’s largest importer of cut flowers. High disposable income, strong gifting culture, and large-scale wedding expenditures drive consistent consumption. Colombia and Ecuador supply the majority of U.S. imports due to favorable trade agreements and geographic proximity. Canada follows with steady growth supported by retail chains and expanding e-commerce floral services. Rising corporate subscriptions and event management spending further strengthen regional growth prospects.

Asia-Pacific

Asia-Pacific contributes around 22% of global demand and is the fastest-growing region, expanding at approximately 7–8% CAGR in emerging markets. China and India lead production and domestic consumption due to large populations and strong festival-driven demand. India’s rapid growth is fueled by an expanding wedding industry and increasing adoption of organized retail floral chains. Japan maintains one of the highest per capita flower consumption rates globally, driven by cultural traditions and strong demand for premium floral aesthetics. Urbanization, rising middle-class income, and improving cold-chain infrastructure are major regional growth drivers.

Middle East & Africa

The Middle East & Africa region accounts for approximately 8% of global demand. Kenya is one of the world’s largest exporters, benefiting from favorable climatic conditions and strong trade ties with Europe. In the Middle East, the UAE and Saudi Arabia are key demand centers, driven by luxury hospitality expansion, large-scale events, and high per capita income. Mega-events, tourism diversification strategies, and rapid hotel construction are accelerating premium flower consumption in the region.

Latin America

Latin America represents roughly 6% of global demand, with Colombia and Ecuador dominating export production. Favorable climate conditions, skilled labor, and strong logistics links to North America make the region highly competitive in global trade. Brazil is witnessing gradual growth in domestic consumption, supported by urban retail expansion, increasing middle-class spending, and rising adoption of organized floral retail formats. Regional trade agreements and agricultural export incentives continue to support production growth and foreign exchange earnings.

Key Players in the Cut Flower Market

- Dümmen Orange

- Syngenta Flowers

- Selecta One

- Beekenkamp Group

- Kariki Group

- Finlay Flowers

- Oserian Development Company

- Multiflora

- Queens Group

- Ball Horticultural Company

- Flamingo Horticulture

- Rosebud Limited

- Florensis

- Marginpar

- Dos Gringos