Cotton Market Size

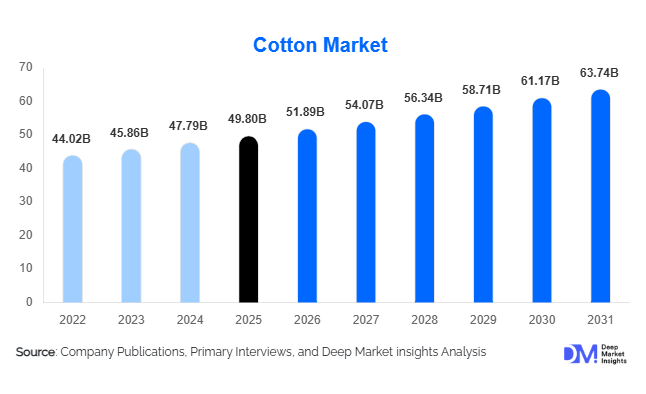

According to Deep Market Insights, the global cotton market size was valued at USD 49.8 billion in 2025 and is projected to grow from USD 51.89 billion in 2026 to reach USD 63.74 billion by 2031, expanding at a CAGR of 4.2% during the forecast period (2026–2031). The cotton market growth is primarily driven by rising demand for sustainable natural fibers, expansion of textile manufacturing capacity across Asia-Pacific, increasing adoption of organic and certified cotton, and growing applications in healthcare, hygiene, and industrial textiles.

Key Market Insights

- Cotton remains the dominant natural fiber globally, supported by strong demand from the apparel, home textiles, and technical textile industries.

- Sustainable and traceable cotton sourcing is becoming a major industry trend, as apparel brands increasingly adopt ESG-focused procurement strategies.

- Asia-Pacific dominates the global cotton market, accounting for more than 53% of total market share, led by China, India, Bangladesh, Pakistan, and Vietnam.

- Organic cotton is among the fastest-growing segments, driven by consumer preference for environmentally sustainable and biodegradable fabrics.

- Brazil and the United States continue to lead cotton exports, while Bangladesh and Vietnam remain major import-driven textile manufacturing hubs.

- Technological integration in cotton farming and textile manufacturing, including AI-based crop monitoring, automated spinning, and precision irrigation, is improving productivity and supply chain efficiency.

What are the latest trends in the cotton market?

Sustainable and Organic Cotton Demand Accelerating

The cotton industry is increasingly shifting toward sustainable production and certified sourcing models. Global apparel brands are expanding commitments toward Better Cotton Initiative (BCI), organic cotton, and recycled cotton procurement to meet ESG targets and consumer sustainability expectations. Fashion retailers are adopting traceability systems and blockchain-enabled supply chain transparency to verify cotton origins and compliance with ethical sourcing regulations. Organic cotton cultivation is expanding significantly across India, Türkiye, and Africa as governments and textile manufacturers invest in eco-friendly textile supply chains. Sustainable cotton is also gaining momentum in premium home textiles, luxury bedding, and wellness-focused apparel categories where consumers are willing to pay premium prices for environmentally responsible products.

Technology Adoption Across Cotton Farming and Processing

Advanced agricultural technologies are increasingly being deployed across cotton-producing regions to improve yield quality, optimize water usage, and reduce production risks. AI-powered crop monitoring systems, satellite-based farm analytics, automated irrigation, genetically improved seed varieties, and drone-assisted pest management are helping farmers improve operational efficiency. Textile manufacturers are simultaneously investing in automated spinning machinery, digital weaving systems, and water-efficient dyeing technologies to reduce operational costs and improve sustainability performance. Digital procurement platforms are also becoming more prominent, allowing textile mills and apparel manufacturers to directly source cotton from growers and traders while improving price transparency and supply reliability.

What are the key drivers in the cotton market?

Growing Demand for Sustainable Natural Fibers

Increasing environmental concerns regarding synthetic fibers and microplastic pollution are significantly boosting global demand for cotton as a biodegradable and renewable fiber. Consumers are increasingly prioritizing sustainable apparel and eco-friendly textiles, encouraging apparel brands to expand cotton-based product portfolios. Cotton’s comfort, breathability, softness, and recyclability continue to support its premium positioning across fashion, home textile, and healthcare applications. Regulatory frameworks promoting sustainable textile sourcing in Europe and North America are further accelerating long-term cotton demand growth.

Expansion of Textile Manufacturing in the Asia-Pacific

Asia-Pacific remains the largest cotton-consuming region globally due to its dominant textile manufacturing industry. Countries such as India, Bangladesh, Vietnam, and Pakistan are witnessing substantial investments in spinning mills, garment manufacturing, and textile export infrastructure. Rising labor costs in China are encouraging apparel brands to diversify sourcing toward alternative Asian manufacturing hubs, increasing regional cotton consumption. Government initiatives supporting textile exports and industrial modernization are also strengthening demand for raw cotton and cotton yarn across the region.

What are the restraints for the global market?

Competition from Synthetic Fibers

The cotton market faces strong competition from synthetic fibers such as polyester and nylon, which offer lower production costs, stable pricing, and scalability advantages. Fast fashion manufacturers often prefer synthetic blends to improve cost efficiency and reduce dependency on weather-sensitive agricultural supply chains. Polyester continues to dominate mass-market apparel production, limiting cotton’s penetration in low-cost clothing segments.

Climate Change and Water Dependency Challenges

Cotton cultivation remains vulnerable to unpredictable weather conditions, droughts, pest infestations, and water scarcity. Cotton is a water-intensive crop, and changing rainfall patterns in key producing countries such as India, Pakistan, and parts of Africa continue to create yield volatility. Rising environmental scrutiny regarding pesticide use and water consumption also presents regulatory and operational challenges for cotton producers globally. Climate-related disruptions can significantly impact global cotton supply and pricing stability.

What are the key opportunities in the cotton industry?

Growth of Organic and Recycled Cotton

The rapid expansion of sustainable fashion presents significant opportunities for organic and recycled cotton producers. Consumers are increasingly demanding environmentally responsible apparel, while major fashion brands are committing to carbon reduction and circular economy goals. This is encouraging investment in organic farming, recycled cotton processing technologies, and traceability platforms. Premium pricing for sustainable cotton products is also improving profitability opportunities for certified producers and textile manufacturers.

Healthcare and Technical Textile Expansion

The growing use of cotton in healthcare and technical textile applications is creating new revenue streams for manufacturers. Cotton-based medical textiles, absorbent cotton, hygiene products, wound care materials, and nonwoven fabrics are witnessing strong demand growth due to rising healthcare expenditures and increasing hygiene awareness globally. Technical textile applications such as filtration fabrics, industrial cloth, and protective apparel are also supporting diversification opportunities for cotton processors and fabric manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 49.8 Billion |

| Market Size in 2026 | USD 51.89 Billion |

| Market Size in 2031 | USD 63.74 Billion |

| CAGR | 4.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Raw lint cotton continues to dominate the global cotton market, accounting for nearly 61% of total market revenue in 2025, primarily due to its extensive utilization across spinning mills, weaving facilities, and textile manufacturing operations worldwide. The segment’s leadership is strongly supported by rising apparel production volumes, increasing global textile exports, and expanding demand for natural fibers in premium clothing and home furnishing applications. Countries such as China, India, Bangladesh, and Vietnam remain the largest consumers of raw lint cotton because of their large-scale yarn spinning and garment manufacturing industries. The growing shift away from synthetic fibers toward biodegradable and breathable textile materials is further strengthening demand for raw lint cotton globally. Conventional cotton continues to account for the majority of global production volumes due to its well-established supply chain infrastructure, large-scale commercial cultivation, and lower production costs compared to organic alternatives. However, organic cotton represents the fastest-growing product category, driven by sustainability initiatives introduced by global apparel brands, stricter environmental regulations, and rising consumer preference for eco-friendly textiles. Major fashion retailers are increasingly integrating certified organic cotton into product portfolios to support ESG commitments and reduce carbon footprints.

Cottonseed products, including cottonseed oil, cottonseed meal, and cotton linters, remain important secondary revenue streams for cotton producers and processors. Cottonseed oil continues witnessing stable demand from the food processing industry, while cottonseed meal is widely utilized in livestock feed applications due to its high protein content. In addition, processed cotton products such as cotton yarn, woven fabrics, knitted textiles, and nonwoven cotton materials are experiencing growing demand from apparel manufacturing, home furnishing, healthcare, and technical textile industries. Rising investments in textile processing infrastructure across Asia-Pacific and Latin America are further strengthening growth prospects for value-added cotton products.

Application Insights

The apparel and garments segment remains the leading application area within the global cotton market, accounting for approximately 58% of total cotton demand in 2025. The segment’s dominance is primarily driven by cotton’s superior comfort, softness, breathability, moisture absorption capability, and skin-friendly characteristics, making it highly preferred for casualwear, denim, sportswear, children’s clothing, innerwear, and athleisure apparel. Rising global fashion consumption, expanding middle-class populations, and increasing demand for sustainable clothing are further accelerating cotton utilization across the apparel sector. Premium and luxury apparel manufacturers are also increasingly adopting organic and traceable cotton sourcing strategies to align with sustainability-focused consumer preferences.

Home textiles represent another major application segment, supported by increasing residential construction activities, rising disposable incomes, and strong growth in the hospitality industry. Cotton-based bed linen, towels, curtains, upholstery fabrics, and premium bedding products continue witnessing substantial demand due to their durability, softness, and comfort characteristics. The expansion of luxury hotels, serviced apartments, and vacation rental properties globally is further contributing to higher consumption of cotton home furnishing products.

Industrial and technical textile applications are also expanding steadily, particularly across medical textiles, filtration fabrics, protective clothing, industrial canvas materials, and automotive interior textiles. The healthcare industry is emerging as a particularly important growth driver for cotton demand due to increasing utilization of absorbent cotton, surgical gauze, wound care products, and hygiene-related textiles. Personal care and hygiene applications, including cotton pads, sanitary products, baby care products, and cosmetic cotton products, are witnessing accelerated growth due to rising hygiene awareness, increasing healthcare expenditure, and expanding personal wellness trends globally.

Distribution Channel Insights

Direct B2B sales channels dominate the global cotton market distribution landscape, accounting for more than 52% of total market transactions in 2025. Large textile mills, spinning companies, and garment manufacturers typically engage in long-term procurement agreements with growers, cooperatives, ginning companies, and commodity traders to ensure consistent supply availability, stable pricing structures, and quality assurance. The dominance of direct procurement channels is particularly strong in major textile-producing countries such as China, India, Bangladesh, Vietnam, and Pakistan, where vertically integrated textile supply chains require uninterrupted access to raw cotton.

Commodity exchanges continue playing a critical role in global cotton pricing and futures trading, especially in export-oriented markets such as the United States, Brazil, and India. Cotton futures contracts help market participants hedge against price volatility caused by weather conditions, geopolitical disruptions, changing textile demand, and fluctuations in export-import dynamics. The increasing globalization of the textile trade has further strengthened the importance of commodity exchanges within international cotton pricing mechanisms.

Digital procurement platforms are rapidly gaining traction within the cotton industry as textile manufacturers increasingly prioritize supply chain transparency, traceability, and operational efficiency. Online sourcing platforms enable buyers to directly connect with suppliers globally, compare pricing benchmarks, monitor shipment schedules, and verify sustainability certifications. Blockchain-enabled traceability systems are also emerging across cotton procurement networks, particularly among premium apparel brands focused on ethical sourcing and ESG compliance. Additionally, export trading companies continue serving as essential intermediaries within global cotton supply chains by facilitating international trade logistics, financing, warehousing, and quality certification services.

End-Use Industry Insights

Textile manufacturing remains the largest end-use industry for cotton, accounting for more than 64% of global cotton consumption in 2025. The segment’s dominance is supported by increasing apparel production, expanding textile exports, and growing consumer demand for natural and sustainable fabrics. Cotton continues to serve as a primary raw material across spinning, weaving, knitting, and garment manufacturing operations globally. Rising investments in textile manufacturing infrastructure across Asia-Pacific, particularly in India, Bangladesh, Vietnam, and Indonesia, are significantly strengthening long-term cotton demand. The apparel and fashion industry continues to be a major driver of cotton consumption due to strong demand for casualwear, denim products, athleisure, sustainable fashion, and premium clothing categories. Global fashion brands are increasingly integrating cotton-based fabrics into eco-conscious product lines to meet rising consumer demand for biodegradable and skin-friendly materials. The rapid expansion of fast fashion retail channels and e-commerce apparel sales is also supporting higher cotton consumption volumes.

Healthcare applications are emerging as one of the fastest-growing end-use industries for cotton, driven by increasing demand for medical cotton, surgical textiles, hygiene products, wound care materials, and absorbent cotton products. Rising healthcare infrastructure investments, aging populations, and growing hygiene awareness globally are contributing to sustained demand growth in this segment. Additionally, the hospitality and home furnishing industries are expanding cotton usage across premium bedding, bath linen, towels, and upholstery applications due to increasing tourism activity and luxury accommodation development worldwide. Automotive interior textiles and industrial fabric applications are also emerging as niche but steadily growing end-use categories. Cotton-based blended fabrics are increasingly utilized in automotive seating, insulation materials, and industrial protective applications due to their durability, comfort, and sustainability advantages.

Explore more data points, trends and opportunities Download Free Sample Report

Cotton Market Segmentations

By Product Type

- Raw Lint Cotton

- Organic Cotton

- Conventional Cotton

- Cottonseed Products

- Processed Cotton Products

By Application

- Apparel & Garments

- Home Textiles

- Industrial & Technical Textiles

- Personal Care & Hygiene Products

- Medical & Healthcare Textiles

By Distribution Channel

- Direct B2B Sales

- Commodity Exchanges

- Export Trading Companies

- Online Procurement Platforms

- Textile Mills & Cooperatives

By End-Use Industry

- Textile Manufacturing

- Apparel & Fashion

- Healthcare

- Hospitality & Home Furnishing

- Automotive & Industrial Applications

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global cotton market with approximately 53% market share in 2025, supported by its position as the world’s largest textile manufacturing and cotton consumption hub. China remains one of the largest producers and consumers of cotton globally due to its extensive spinning, weaving, and apparel manufacturing industries. India benefits from vast cultivation acreage, favorable climatic conditions, government support programs, and expanding textile exports under initiatives aimed at strengthening domestic manufacturing capabilities. Bangladesh and Vietnam continue witnessing significant growth in cotton imports due to the rapid expansion of export-oriented garment manufacturing industries supplying global fashion brands. Pakistan also remains a major cotton-consuming market because of its integrated textile and apparel export sector.

The region’s growth is being driven by rising disposable incomes, urbanization, expanding middle-class populations, strong apparel export demand, and increasing investments in textile manufacturing infrastructure. Favorable government initiatives supporting textile industrialization, low labor costs, and the relocation of global apparel sourcing away from China toward South and Southeast Asia are further accelerating regional market expansion. Asia-Pacific is also benefiting from increasing adoption of automated spinning technologies, AI-based textile production systems, and sustainable cotton sourcing programs, making it the fastest-growing regional market during the forecast period.

North America

North America accounted for nearly 21% of the global cotton market in 2025, led primarily by the United States, which remains one of the world’s largest cotton exporters. The region benefits from highly mechanized farming operations, advanced irrigation infrastructure, strong agricultural productivity, and sophisticated supply chain systems. American cotton exports are deeply integrated into Asian textile manufacturing supply chains, particularly across China, Vietnam, Bangladesh, and Türkiye.

Regional market growth is being driven by technological advancements in precision agriculture, increasing adoption of sustainable farming practices, and rising demand for traceable cotton products among apparel brands. The United States is also witnessing increased investments in AI-powered crop monitoring, automated harvesting systems, and water-efficient farming technologies aimed at improving yield consistency and export competitiveness. Mexico is emerging as an important regional growth market due to rising demand from apparel manufacturing, automotive textiles, and nearshoring trends that are strengthening textile production capacities across North America.

Europe

Europe represents a mature but sustainability-driven cotton market characterized by strong demand for organic, traceable, and ethically sourced textile materials. Germany, Italy, France, Spain, and Türkiye are among the major cotton-consuming countries within the region. European apparel brands are increasingly prioritizing sustainable cotton procurement due to tightening environmental regulations, carbon reduction targets, and growing consumer demand for eco-friendly fashion products.

The region’s market growth is being driven by expanding sustainable fashion trends, rising adoption of circular textile economy initiatives, and increasing investments in recycled and organic cotton processing. Türkiye plays a particularly important role within the European cotton value chain due to its large textile manufacturing base and strong apparel export relationships with European fashion retailers. Additionally, premium home furnishing demand, luxury textile production, and stringent ESG compliance standards continue strengthening cotton consumption across Europe.

Latin America

Brazil dominates the Latin American cotton market and has emerged as one of the world’s leading cotton exporters due to large-scale mechanized farming operations, favorable climatic conditions, and export-oriented production strategies. The country has significantly expanded cotton cultivation acreage and invested heavily in advanced agricultural technologies, enabling strong productivity growth and international competitiveness.

Regional market growth is being supported by increasing global demand for high-quality cotton exports, rising investments in agricultural modernization, and improving trade connectivity with Asia-Pacific textile markets. Argentina and Paraguay are also expanding cotton cultivation activities to strengthen export opportunities and diversify agricultural revenue streams. Latin America is benefiting from growing international demand for sustainably produced cotton, particularly from European and North American apparel brands seeking diversified sourcing destinations.

Middle East & Africa

The Middle East & Africa region is emerging as a high-growth cotton production and export hub, supported by increasing international investments in agricultural modernization, irrigation infrastructure, and textile manufacturing development. African countries including Benin, Mali, Côte d’Ivoire, Burkina Faso, and Egypt are significantly expanding cotton production and exports to meet rising global textile demand.

The region’s growth is being driven by favorable agricultural conditions, low production costs, expanding government support programs, and rising foreign direct investments in farming and textile processing infrastructure. Egypt continues to maintain strong demand for extra-long staple cotton used in premium luxury textiles globally. Gulf countries such as the UAE and Saudi Arabia are also increasing investments in textile manufacturing, cotton trading infrastructure, and industrial diversification programs aimed at reducing dependence on oil-based revenues. In addition, improving logistics connectivity and increasing trade partnerships with Asian textile manufacturers are strengthening the region’s position within the global cotton supply chain.

Key Players in the Cotton Market

- Cargill Incorporated

- Louis Dreyfus Company

- Olam Group

- ECOM Agroindustrial Corp.

- Calcot Ltd.

- Plains Cotton Cooperative Association (PCCA)

- Viterra

- Allenberg Cotton Company

- Namoi Cotton Ltd.

- Sinotex Group

- Weiqiao Textile Company

- Shandong Ruyi Group

- Alok Industries

- Vardhman Textiles

- Nahar Spinning Mills