Cordless Vacuum Cleaner Market Size

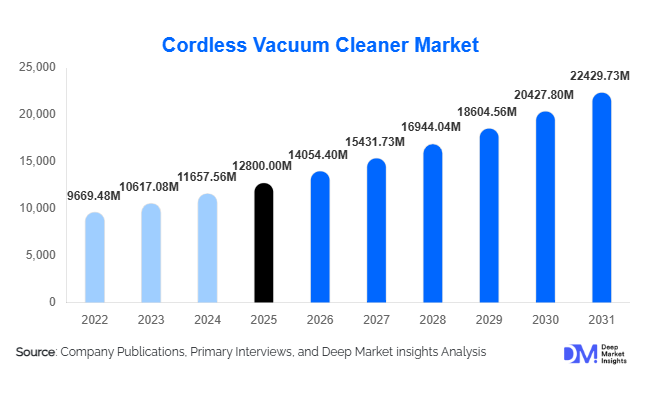

According to Deep Market Insights, the global cordless vacuum cleaner market size was valued at USD 12,800 million in 2025 and is projected to grow from USD 14,054.40 million in 2026 to reach USD 22,429.73 million by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The cordless vacuum cleaner market is experiencing growth primarily driven by rising demand for convenient, portable cleaning solutions, advancements in battery technology, and increasing consumer awareness of hygiene and indoor air quality. The transition toward smart homes and connected appliances is further accelerating adoption, particularly in developed economies. Additionally, the expansion of e-commerce channels and the growing availability of mid-range and premium products are supporting broader market penetration globally.

Key Market Insights

- Stick vacuum cleaners dominate the market, driven by their lightweight design, versatility, and strong suction performance.

- Lithium-ion batteries account for the majority share, enabling longer runtime, faster charging, and improved durability.

- North America leads the global market, supported by high disposable incomes and strong smart home adoption.

- Asia-Pacific is the fastest-growing region, fueled by urbanization and rising middle-class demand in China and India.

- Online retail channels are rapidly expanding, offering price transparency, product comparisons, and convenience.

- Technological advancements, including AI-enabled navigation and smart connectivity, are reshaping product innovation.

What are the latest trends in the cordless vacuum cleaner market?

Smart and Connected Cleaning Solutions

The integration of smart technologies is transforming the cordless vacuum cleaner market. Manufacturers are increasingly incorporating IoT-enabled features such as mobile app control, voice assistant compatibility, and real-time performance monitoring. Robotic cordless vacuum cleaners with AI-driven navigation systems are gaining traction, particularly in urban households. These innovations enhance user convenience and efficiency, allowing automated cleaning schedules and adaptive cleaning patterns. The trend is particularly strong in North America and Europe, where smart home ecosystems are well established. Additionally, brands are focusing on user-friendly interfaces and software updates to improve long-term functionality, making smart vacuums a central component of connected living environments.

Shift Toward Premium and Multi-Functional Devices

Consumers are increasingly opting for premium cordless vacuum cleaners that offer enhanced features such as high suction power, HEPA filtration, and multi-surface cleaning capabilities. Multi-functional designs that convert from stick to handheld units are gaining popularity, providing greater versatility. This premiumization trend is supported by rising disposable incomes and growing awareness of indoor air quality. Manufacturers are also introducing modular accessories, including pet hair attachments and advanced filtration systems, catering to specific consumer needs. This shift toward high-performance products is driving higher average selling prices and improving profit margins across the industry.

What are the key drivers in the cordless vacuum cleaner market?

Growing Demand for Convenience and Portability

Modern lifestyles, characterized by busy schedules and compact living spaces, are driving demand for easy-to-use cleaning appliances. Cordless vacuum cleaners eliminate the limitations of power cords, offering greater mobility and flexibility. This convenience is particularly appealing in urban households and small apartments, where traditional vacuum cleaners may be less practical. The ability to quickly clean multiple surfaces without setup constraints has made cordless models a preferred choice among consumers globally.

Advancements in Battery Technology

Significant improvements in lithium-ion battery technology have addressed key limitations of earlier cordless models. Enhanced energy density, faster charging times, and longer operational life have made cordless vacuum cleaners more reliable and efficient. These advancements have expanded their usability beyond small spaces to larger residential and commercial environments. Continuous R&D investments in battery innovation, including emerging solid-state technologies, are expected to further strengthen this growth driver.

What are the restraints for the global market?

High Initial Cost of Premium Models

Despite their advantages, cordless vacuum cleaners often come with higher upfront costs compared to traditional corded models. Premium devices with advanced features can be particularly expensive, limiting adoption in price-sensitive markets. This cost barrier is especially evident in developing regions, where consumers may prioritize affordability over advanced functionality.

Battery Degradation and Replacement Costs

Battery performance tends to decline over time, affecting runtime and overall efficiency. Replacement batteries can be costly, adding to the total cost of ownership. This issue is particularly relevant for heavy users in commercial settings, where frequent usage accelerates battery wear. Addressing battery longevity and reducing replacement costs remain key challenges for manufacturers.

What are the key opportunities in the cordless vacuum cleaner industry?

Expansion in Emerging Markets

Emerging economies in the Asia-Pacific, Latin America, and Africa present significant growth opportunities. Rising disposable incomes, increasing urbanization, and improving living standards are driving demand for modern home appliances. Manufacturers that introduce cost-effective, durable products tailored to local preferences can capture substantial market share. Government initiatives promoting electrification and improved housing infrastructure further support market expansion in these regions.

Technological Innovation and Sustainability

Innovation in battery efficiency, motor performance, and sustainable materials offers strong growth potential. The development of eco-friendly products, including recyclable components and energy-efficient designs, aligns with global environmental regulations and consumer preferences. Additionally, integrating AI and automation into cordless vacuum cleaners can create differentiated products, attracting tech-savvy consumers and enhancing brand competitiveness.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12800 Million |

| Market Size in 2026 | USD 14054.40 Million |

| Market Size in 2031 | USD 22429.73 Million |

| CAGR | 9.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Stick vacuum cleaners continue to lead the global cordless vacuum cleaner market, accounting for approximately 38% of total market share in 2025. The primary driver behind this dominance is their ergonomic and lightweight design, combined with high functional versatility. These devices can seamlessly transition between floor cleaning and handheld usage, making them ideal for multi-surface applications in residential settings. Additionally, advancements in motor efficiency and suction power have enabled stick vacuums to deliver performance comparable to traditional corded models, further accelerating adoption. Their compatibility with modular attachments, such as crevice tools, pet hair brushes, and upholstery cleaners, enhances usability, making them the preferred choice globally. Meanwhile, robotic cordless vacuum cleaners are emerging as a high-growth sub-segment, driven by increasing demand for automation and smart home integration, particularly in urban households.

Battery Type Insights

Lithium-ion batteries dominate the cordless vacuum cleaner market with an estimated 82% share in 2025, primarily due to their superior energy density and longer lifecycle performance. The leading driver for this segment is the growing need for extended runtime and consistent suction power, especially in larger homes and commercial applications. Lithium-ion technology enables faster charging cycles, reduced memory effect, and improved durability, making it the preferred choice for manufacturers and consumers alike. Additionally, declining battery costs and continuous R&D investments have made lithium-ion solutions more accessible across mid-range product categories. In contrast, nickel-based batteries are witnessing declining demand due to inefficiencies and shorter lifespans, while solid-state batteries represent an emerging opportunity, with the potential to revolutionize safety standards and energy storage capabilities in the long term.

Distribution Channel Insights

Online retail channels account for approximately 44% of total market sales in 2025, making them the leading distribution segment. The key driver for this dominance is the rapid expansion of e-commerce ecosystems and direct-to-consumer (D2C) strategies adopted by manufacturers. Consumers increasingly prefer online platforms due to the convenience of home delivery, availability of detailed product comparisons, user reviews, and competitive pricing. Flash sales, discounts, and bundled offerings further enhance the attractiveness of online channels. Additionally, digital marketing and influencer-driven promotions are playing a significant role in shaping purchasing decisions. Despite this, offline retail remains relevant, particularly in developing markets, where consumers value in-store demonstrations, personalized assistance, and immediate product availability.

End-Use Insights

The residential segment dominates the cordless vacuum cleaner market, contributing over 70% of total demand in 2025. The primary driver for this segment is the rapid pace of urbanization combined with increasing consumer focus on convenience and hygiene. Smaller living spaces, busy lifestyles, and the need for quick cleaning solutions have made cordless vacuum cleaners an essential household appliance. Additionally, rising disposable incomes and growing awareness of indoor air quality are encouraging consumers to invest in advanced cleaning technologies. The commercial segment, including hospitality, healthcare, and office spaces, is the fastest-growing segment with a CAGR exceeding 11%. Growth in this segment is driven by the need for efficient, portable, and time-saving cleaning solutions, especially in environments requiring frequent and large-scale cleaning operations.

Explore more data points, trends and opportunities Download Free Sample Report

Cordless Vacuum Cleaner Market Segmentations

By Product Type

- Stick Vacuum Cleaners

- Handheld Vacuum Cleaners

- Robotic Cordless Vacuum Cleaners

- Upright Cordless Vacuum Cleaners

- Canister Cordless Vacuum Cleaners

By Battery Type

- Lithium-ion Batteries

- Nickel-based Batteries (NiMH/NiCd)

- Solid-State Batteries

By Distribution Channel

- Online Retail

- Specialty Stores

- Hypermarkets/Supermarkets

- Electronics Retail Chains

By End-Use

- Residential

- Commercial – Offices

- Commercial – Hospitality

- Commercial – Healthcare

- Commercial – Retail Spaces

Regional Insights

North America

North America is expected to hold approximately 32% of the global cordless vacuum cleaner market share by 2025, with the United States being the dominant contributor. The key driver of regional growth is the high adoption of smart home technologies and strong consumer preference for premium appliances. The region benefits from high disposable incomes, enabling consumers to invest in advanced cordless vacuum models with AI-enabled features and superior performance. Additionally, the presence of leading market players and continuous product innovation further strengthens demand. Canada also contributes significantly, driven by increasing awareness of energy-efficient appliances and sustainability-focused consumption patterns.

Europe

Europe accounts for around 28% of the global market share, led by Germany, the UK, and France. The primary driver for growth in this region is the stringent regulatory framework promoting energy efficiency and environmental sustainability. Consumers are increasingly inclined toward eco-friendly appliances with low energy consumption and recyclable components. Additionally, high urban density and smaller living spaces in European cities are boosting demand for compact and lightweight cordless vacuum cleaners. Premiumization trends are also strong in this region, with consumers willing to pay higher prices for technologically advanced and environmentally responsible products.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the cordless vacuum cleaner market, driven by countries such as China, Japan, and India. The leading growth driver is rapid urbanization combined with expanding middle-class income levels. China dominates both production and consumption due to its strong manufacturing ecosystem and large domestic market. India is witnessing accelerated demand growth due to increasing awareness of modern home appliances and improving living standards. Additionally, the rapid expansion of e-commerce platforms and the availability of affordable product variants are significantly boosting market penetration. Government initiatives supporting domestic manufacturing further contribute to regional growth.

Latin America

Latin America, led by Brazil and Mexico, is experiencing moderate growth in the cordless vacuum cleaner market. The primary driver is the expansion of organized retail and e-commerce infrastructure, which is improving product accessibility across urban and semi-urban areas. Rising consumer awareness regarding hygiene and modern appliances is also contributing to demand. However, economic volatility and price sensitivity remain key challenges, limiting the adoption of premium products. Manufacturers are increasingly focusing on cost-effective models to cater to this region’s demand dynamics.

Middle East & Africa

The Middle East & Africa region is gradually expanding, with the UAE and South Africa as key markets. The major driver for growth is increasing urban development and rising adoption of modern household appliances. In the Middle East, high disposable incomes and a strong preference for premium lifestyle products are supporting demand for advanced cordless vacuum cleaners. In Africa, improving living standards and infrastructure development are driving gradual adoption. Additionally, growth in the hospitality sector across the region is creating demand for efficient and portable cleaning solutions in commercial applications.