Consumer Electronics Stores Market Size

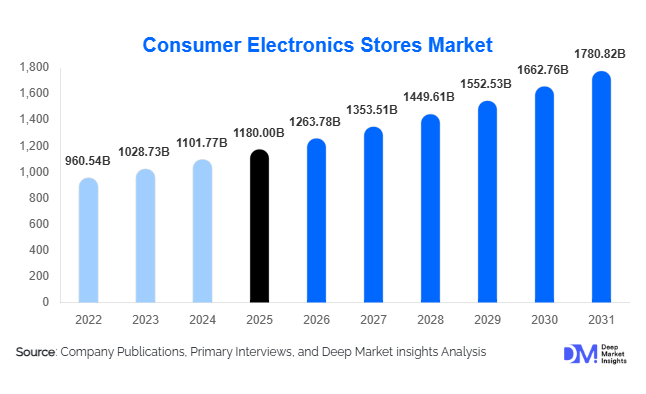

According to Deep Market Insights, the global consumer electronics stores market size was valued at USD 1,180 billion in 2025 and is projected to grow from USD 1,263.78 billion in 2026 to reach USD 1,780.82 billion by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for smart devices, rapid urbanization, and the growing importance of omnichannel retail strategies. Rising disposable incomes, particularly in emerging economies, along with shorter replacement cycles for electronics such as smartphones, laptops, and home appliances, are further accelerating demand. Additionally, experiential retail formats and in-store digital integrations are enhancing customer engagement, making physical electronics stores a vital component of the global retail ecosystem despite the growth of e-commerce.

Key Market Insights

- Omnichannel retailing is transforming the market, with retailers integrating online and offline experiences to improve customer convenience and engagement.

- Smartphones and connected devices dominate sales, driven by rapid innovation cycles and increasing digital dependency.

- Asia-Pacific leads the global market, supported by large consumer bases, rising incomes, and expanding organized retail infrastructure.

- Experiential retail formats are gaining popularity, with stores offering product demonstrations, smart home simulations, and personalized consultations.

- Financing and EMI options are boosting sales, making high-value electronics accessible to a wider customer base.

- Technological integration in stores, including AI-based recommendations and smart inventory systems, is enhancing operational efficiency and customer experience.

What are the latest trends in the consumer electronics stores market?

Rise of Omnichannel and Phygital Retail

The convergence of online and offline retail channels is one of the most prominent trends shaping the consumer electronics stores market. Retailers are investing heavily in omnichannel capabilities, enabling customers to browse products online, check in-store availability, and opt for click-and-collect services. This hybrid approach enhances customer convenience and reduces friction in the buying journey. Stores are increasingly functioning as experience centers where customers can physically interact with products before making a purchase decision. Integration of digital tools such as mobile apps, QR codes, and virtual assistants is further bridging the gap between physical and digital retail environments, ensuring a seamless customer experience.

Experiential and Smart Retail Environments

Consumer electronics stores are evolving into immersive environments designed to showcase technology in real-life scenarios. Retailers are creating smart home zones, gaming arenas, and interactive demo areas that allow customers to experience products firsthand. This trend is particularly effective for high-value purchases such as smart TVs, home automation systems, and premium appliances. Additionally, the use of augmented reality (AR) and artificial intelligence (AI) within stores is enabling personalized product recommendations and enhancing customer engagement. These innovations not only improve conversion rates but also strengthen brand loyalty by offering differentiated in-store experiences.

What are the key drivers in the consumer electronics stores market?

Rapid Technological Innovation and Product Cycles

Continuous advancements in consumer electronics, including 5G-enabled smartphones, AI-powered devices, and IoT-based home automation systems, are driving frequent product upgrades. Consumers are increasingly seeking the latest technologies, leading to shorter replacement cycles and higher store footfall. Physical stores play a critical role in enabling hands-on experiences for such advanced products, reinforcing their importance in the retail ecosystem.

Rising Disposable Income and Urbanization

Growing middle-class populations, particularly in emerging markets such as India, China, and Southeast Asia, are significantly boosting demand for consumer electronics. Urbanization is facilitating access to organized retail formats, where consumers can explore a wide range of products under one roof. This socio-economic shift is driving higher spending on premium and smart devices, contributing to overall market expansion.

What are the restraints for the global market?

Intense Competition from E-commerce Platforms

The rapid growth of e-commerce platforms poses a significant challenge to traditional electronics stores. Online retailers often offer competitive pricing, extensive product selections, and convenience, attracting price-sensitive consumers. This has forced physical retailers to adopt aggressive discounting strategies, impacting profit margins and operational sustainability.

High Operational and Real Estate Costs

Operating large-format electronics stores requires substantial investments in real estate, staffing, and inventory management. High rental costs in prime urban locations, coupled with rising labor expenses, can limit profitability and expansion, particularly for smaller players. These cost pressures necessitate efficient store management and strategic location planning.

What are the key opportunities in the consumer electronics stores market?

Expansion into Emerging Markets and Tier II/III Cities

Emerging economies present significant growth opportunities due to rising disposable incomes and increasing digital adoption. Expansion into Tier II and Tier III cities, particularly in Asia-Pacific and Latin America, allows retailers to tap into underserved markets with growing demand for consumer electronics. Establishing franchise models and smaller store formats can facilitate cost-effective expansion and long-term market penetration.

Integration of Smart Technologies and IoT Ecosystems

The growing adoption of smart home technologies presents an opportunity for retailers to offer integrated solutions and bundled products. Stores can differentiate themselves by providing demonstrations of connected ecosystems, such as smart lighting, security systems, and home automation. This not only enhances customer understanding but also increases average transaction values through cross-selling opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1180 Billion |

| Market Size in 2026 | USD 1263.78 Billion |

| Market Size in 2031 | USD 1780.82 Billion |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Category Insights

Smartphones and tablets dominate the consumer electronics stores market, accounting for approximately 32% of total revenue in 2025. This segment continues to lead primarily due to high replacement frequency, rapid technological advancements (5G, AI-enabled devices), and universal adoption across income groups. Consumers increasingly prefer in-store experiences for premium smartphones to assess features such as camera quality, display, and ecosystem compatibility, further strengthening store-led sales. Additionally, frequent product launches and brand-driven upgrade cycles sustain consistent footfall in retail outlets. Home entertainment systems, including smart TVs, streaming devices, and gaming consoles, represent the second-largest segment. Growth in this category is driven by rising digital content consumption, OTT platform penetration, and demand for immersive home experiences. Larger screen sizes, 4K/8K resolution adoption, and gaming culture expansion are further accelerating demand. Retail stores play a key role by offering demo zones that enable customers to experience audiovisual quality before purchase.

Wearable devices are emerging as a high-growth segment, supported by increasing health awareness, fitness tracking trends, and integration with smartphones and healthcare ecosystems. Meanwhile, accessories such as headphones, chargers, and peripherals contribute steady revenue streams due to their recurring purchase nature, high margins, and cross-selling potential. Retailers often bundle accessories with primary devices, enhancing average transaction value and profitability.

Store Format Insights

Multi-brand retail chains hold the largest market share, approximately 38% in 2025, driven by their ability to offer wide product assortments, competitive pricing, and one-stop shopping convenience. These stores benefit from strong supplier relationships, economies of scale, and the ability to attract diverse customer segments. Their dominance is further reinforced by promotional campaigns, financing options, and in-store expertise. Exclusive brand stores are gaining traction, particularly in premium segments, as they provide curated brand experiences, direct customer engagement, and better control over pricing and product positioning. Leading global brands are increasingly investing in flagship stores to strengthen brand identity and showcase innovation.

Independent retailers and specialty stores continue to serve local and niche markets, particularly in semi-urban and rural areas, where personalized service and proximity remain key advantages. Warehouse clubs and cash-and-carry formats cater to bulk buyers and price-sensitive consumers, leveraging volume-based pricing strategies to remain competitive.

Sales Channel Insights

Omnichannel retailers dominate the market with around 45% share, reflecting the growing preference for integrated shopping experiences that combine online convenience with offline assurance. The ability to browse online, compare prices, and complete purchases in-store (or vice versa) has become a key differentiator. Retailers leveraging click-and-collect models, real-time inventory tracking, and unified customer data platforms are achieving higher customer retention and conversion rates.

Offline-only stores, while gradually declining in relative share, remain relevant for consumers seeking hands-on product experience, immediate availability, and personalized assistance. The ongoing integration of digital tools such as AI-based recommendations, in-store kiosks, and mobile-enabled billing systems is transforming traditional stores into digitally enabled retail environments.

End-Use Insights

Individual consumers (B2C) account for approximately 82% of the market, driven by widespread demand for personal electronics such as smartphones, laptops, and home appliances. Increasing digital lifestyles, remote work trends, and entertainment consumption are key factors supporting sustained demand in this segment. The corporate and institutional segment, although smaller, is witnessing robust growth at a CAGR of 8–9%, fueled by enterprise digital transformation, hybrid work models, and increasing investments in IT infrastructure. Bulk purchases of laptops, networking equipment, and conferencing devices are contributing to this growth.

Emerging applications across healthcare, education, and hospitality sectors are further expanding market scope. For instance, hospitals are adopting connected devices for patient monitoring, educational institutions are investing in digital classrooms, and hotels are upgrading in-room entertainment systems, collectively driving incremental demand for consumer electronics through retail channels.

Explore more data points, trends and opportunities Download Free Sample Report

Consumer Electronics Stores Market Segmentations

By Product Category

- Smartphones & Tablets

- Computers & Laptops

- Home Entertainment Systems

- Home Appliances

- Wearable Devices

- Accessories

By Store Format

- Multi-brand Retail Chains

- Exclusive Brand Stores

- Independent Retailers

- Specialty Electronics Stores

- Warehouse Clubs / Cash & Carry Stores

By Sales Channel

- Offline-Only Stores

- Omnichannel Retailers (Online + Offline Integration)

SBy tore Size

- Large Format Stores (>10,000 sq ft)

- Mid-size Stores (2,000–10,000 sq ft)

- Small Format Stores (<2,000 sq ft)

By Customer Type

- Individual Consumers (B2C)

- Institutional Buyers (B2B)

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global consumer electronics stores market with a share of approximately 46% in 2025. China leads the region due to its large consumer base, strong domestic manufacturing ecosystem, and extensive organized retail networks. India is the fastest-growing market, driven by rapid urbanization, rising disposable incomes, an expanding middle-class population, and government initiatives such as digitalization and local manufacturing support. Additionally, increasing penetration of organized retail in Tier II and Tier III cities is unlocking new demand. Japan and South Korea contribute through high technology adoption, premium product demand, and mature retail ecosystems, supported by innovation-driven consumer behavior.

North America

North America accounts for around 22% of the market, with the United States being the primary contributor. Growth in this region is driven by high consumer purchasing power, early adoption of advanced technologies, and strong omnichannel retail infrastructure. The presence of major retail chains and continuous product innovation supports steady demand. Additionally, increasing interest in smart home devices and connected ecosystems is boosting in-store sales. Canada contributes through stable economic conditions, high digital penetration, and well-established retail networks, ensuring consistent market growth.

Europe

Europe holds approximately 18% market share, with key countries including Germany, the United Kingdom, and France. The region’s growth is driven by strong demand for premium and energy-efficient electronics, stringent regulatory standards, and increasing environmental awareness. Consumers are prioritizing sustainable and energy-rated appliances, encouraging retailers to expand eco-friendly product offerings. Additionally, well-developed retail infrastructure and high urbanization levels support steady market expansion across Western Europe, while Eastern Europe presents emerging growth opportunities.

Middle East & Africa

This region represents about 7% of the global market. The UAE and Saudi Arabia lead due to high disposable incomes, strong demand for premium electronics, and rapid adoption of smart home technologies. Government-led diversification initiatives and smart city projects are further driving demand for advanced electronics. In Africa, countries such as South Africa and Nigeria are emerging markets, supported by growing urban populations, improving retail infrastructure, and increasing access to affordable consumer electronics. However, growth is moderated by price sensitivity and supply chain challenges in certain regions.

Latin America

Latin America also holds around 7% market share, led by Brazil and Mexico. Market growth is driven by improving economic conditions, expanding middle-class population, and increasing digital adoption. Rising demand for smartphones and home entertainment devices is a key growth driver. Additionally, the expansion of organized retail chains and improved access to financing options are supporting higher consumer spending on electronics. Despite economic volatility, the region presents long-term growth potential due to its large and relatively underpenetrated consumer base.

Key Players in the Consumer Electronics Stores Market

- Best Buy Co., Inc.

- MediaMarktSaturn Retail Group

- JD.com, Inc.

- Suning.com Co., Ltd.

- Walmart Inc.

- Costco Wholesale Corporation

- Fnac Darty

- Elkjøp Nordic AS

- Bic Camera Inc.

- Yamada Denki Co., Ltd.

- Reliance Retail Limited

- Croma (Tata Group)

- Currys plc

- Euronics International

- Harvey Norman Holdings Ltd