Computer Cleaners Market Size

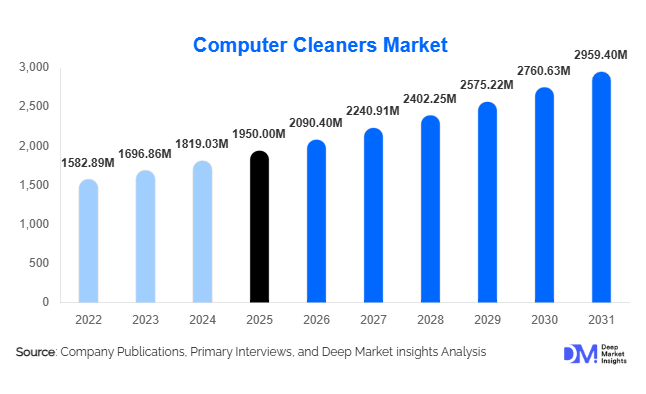

According to Deep Market Insights, the global computer cleaners market size was valued at USD 1,950 million in 2025 and is projected to grow from USD 2,090.40 million in 2026 to reach USD 2,959.40 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The market growth is primarily driven by increasing global device penetration, rising awareness regarding preventive maintenance of electronic devices, and the rapid expansion of data center infrastructure. The growing reliance on laptops, desktops, gaming systems, and enterprise IT hardware has created sustained demand for specialized cleaning solutions that enhance device performance and longevity.

Key Market Insights

- Compressed air cleaners dominate product demand, owing to their efficiency in removing dust from sensitive internal components without physical contact.

- Online retail channels lead distribution, supported by e-commerce growth, product accessibility, and competitive pricing.

- North America holds the largest market share, driven by high IT infrastructure density and enterprise spending.

- Asia-Pacific is the fastest-growing region, fueled by increasing digitalization and rising computer penetration in emerging economies.

- Eco-friendly and non-toxic cleaning solutions are gaining traction, driven by regulatory pressures and consumer awareness.

- Data center expansion is a major growth catalyst, creating demand for high-performance and anti-static cleaning solutions.

What are the latest trends in the computer cleaners market?

Shift Toward Eco-Friendly Cleaning Solutions

Environmental concerns and regulatory frameworks are pushing manufacturers toward sustainable product development. Companies are increasingly introducing biodegradable, non-toxic, and refillable cleaning solutions to reduce environmental impact. Aerosol-free air dusters and plant-based cleaning liquids are gaining traction, particularly in Europe and North America. This shift is also influencing packaging innovations, with brands adopting recyclable materials and reduced plastic usage. Sustainability certifications and eco-labeling are becoming key differentiators, especially for institutional buyers and environmentally conscious consumers.

Growth of Multi-Functional Cleaning Kits

Consumers are showing a growing preference for all-in-one cleaning kits that combine multiple tools such as brushes, microfiber cloths, gels, and cleaning solutions. These kits provide convenience and cost efficiency, making them popular among both residential users and corporate buyers. Manufacturers are focusing on ergonomic designs and portability, enabling easy use across multiple devices, including laptops, keyboards, and gaming systems. The trend is particularly strong in online retail channels, where bundled offerings are marketed as value-added solutions.

What are the key drivers in the computer cleaners market?

Rising Global Device Ownership

The increasing adoption of laptops, desktops, and peripherals across households and enterprises is a primary driver of the computer cleaners market. Remote work trends, digital education, and gaming have significantly expanded the installed base of computing devices. As usage intensifies, devices are more prone to dust accumulation and performance degradation, driving the need for regular cleaning and maintenance solutions.

Expansion of Data Centers and Cloud Infrastructure

The rapid growth of cloud computing, AI workloads, and big data analytics has led to significant investments in data center infrastructure. These facilities require high levels of cleanliness to ensure optimal performance and prevent hardware failures. Specialized cleaning solutions, including anti-static sprays and compressed air products, are increasingly used for maintaining servers and networking equipment, contributing to sustained market demand.

What are the restraints for the global market?

Availability of Low-Cost Alternatives

A significant portion of consumers relies on household cleaning methods or low-cost substitutes instead of specialized products. This behavior is particularly prevalent in price-sensitive regions, limiting market penetration for premium cleaning solutions. The perception that specialized cleaners are non-essential further restricts adoption among certain consumer segments.

Regulatory Restrictions on Aerosol Products

Environmental regulations targeting aerosol emissions and chemical compositions pose challenges for manufacturers. Compliance with these regulations often requires reformulation and increased production costs. Restrictions on propellants used in compressed air cleaners may also limit product availability in certain regions, affecting overall market growth.

What are the key opportunities in the computer cleaners industry?

Data Center-Specific Cleaning Solutions

The expansion of hyperscale data centers presents a high-value opportunity for manufacturers. These facilities require specialized cleaning products that minimize electrostatic discharge and contamination risks. Companies that develop precision cleaning solutions tailored for servers and high-performance computing equipment can tap into a growing and recurring demand segment.

Emerging Market Expansion

Rapid digitalization in Asia-Pacific, Latin America, and parts of Africa is creating new demand for computer cleaning products. Increasing computer penetration in education, SMEs, and government initiatives is driving market growth. Localized production, affordable pricing strategies, and strong distribution networks can help companies capture these emerging opportunities effectively.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1950 Million |

| Market Size in 2026 | USD 2090.40 Million |

| Market Size in 2031 | USD 2959.40 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Compressed air cleaners lead the computer cleaners market with approximately 32% share in 2025, primarily driven by their superior ability to remove dust and debris from sensitive internal components such as cooling fans, circuit boards, and heat sinks without physical contact. This non-invasive cleaning capability makes them indispensable in high-performance environments such as data centers, enterprise IT systems, and gaming hardware. Additionally, increasing awareness regarding overheating issues and hardware failure prevention has further accelerated the adoption of compressed air solutions. Cleaning liquids and sprays hold the second-largest share, supported by growing demand for screen-safe and anti-static formulations for monitors, laptops, and peripherals. Cleaning kits are rapidly gaining traction due to their bundled value proposition, offering convenience and cost-effectiveness for both residential and professional users. Meanwhile, gels, wipes, and microfiber-based tools cater to niche yet essential use cases, particularly for precision cleaning and portability, ensuring steady demand across multiple user segments.

Application Insights

Preventive maintenance dominates the application segment, accounting for nearly 35% of the global market share, driven by the increasing shift from reactive to proactive device management strategies. Organizations and individual users are recognizing the cost benefits of regular cleaning in minimizing downtime, reducing repair costs, and extending device lifespan. This trend is particularly strong in enterprise IT environments where uninterrupted operations are critical. Internal component cleaning represents a significant portion of demand, especially in data centers and industrial computing systems, where dust accumulation can directly impact thermal efficiency and system reliability. External surface cleaning continues to maintain steady demand, supported by heightened awareness of hygiene and device aesthetics in both consumer and office environments. The growing importance of workplace cleanliness and shared device usage is further reinforcing demand across this segment.

Distribution Channel Insights

Online retail leads the distribution landscape, contributing approximately 40% of total market sales, driven by the rapid expansion of e-commerce platforms and changing consumer purchasing behavior. The availability of a wide product range, competitive pricing, user reviews, and doorstep delivery has made online channels the preferred choice for both individual consumers and small businesses. Additionally, subscription-based models and bulk purchase options are gaining traction among enterprises. Offline retail channels, including electronics stores, supermarkets, and specialty IT outlets, continue to play a crucial role, particularly in regions with lower e-commerce penetration. These channels benefit from immediate product availability and customer trust. Direct sales channels are highly significant in the B2B segment, where enterprises, data centers, and institutions procure cleaning solutions in bulk through contractual agreements, ensuring consistent demand and long-term supplier relationships.

End-Use Insights

Corporate offices and IT enterprises represent the largest end-use segment, contributing approximately 30% of total market demand, driven by the need to maintain operational efficiency and minimize equipment downtime. The increasing number of computing devices per employee and the adoption of hybrid work models have further strengthened demand in this segment. The data center segment is the fastest-growing end-use category, supported by global investments in cloud computing, artificial intelligence, and digital infrastructure. These facilities require high-performance cleaning solutions to maintain optimal operating conditions and prevent costly system failures. Residential consumers form a substantial demand base, fueled by rising laptop and desktop penetration, remote work trends, and growing awareness of device maintenance. Emerging segments such as gaming and esports are also witnessing strong growth, as high-performance systems require frequent cleaning to sustain performance, thereby driving demand for premium and specialized cleaning products.

Explore more data points, trends and opportunities Download Free Sample Report

Computer Cleaners Market Segmentations

By Product Type

- Compressed Air Cleaners

- Cleaning Liquids & Sprays

- Cleaning Gels & Putty

- Cleaning Wipes

- Cleaning Kits

- Cleaning Brushes & Tools

By Application

- Internal Component Cleaning

- External Surface Cleaning

- Preventive Maintenance

- Deep Cleaning / Restoration

By Distribution Channel

- Online Retail

- Electronics and Specialty Stores

- Supermarkets/Hypermarkets

- Direct Sales (B2B Procurement)

By End-Use Industry

- Residential / Individual Consumers

- Corporate Offices & IT Enterprises

- Data Centers & Cloud Infrastructure

- Healthcare Institutions

- Educational Institutions

- Manufacturing & Industrial Facilities

- Gaming & Esports Industry

Regional Insights

North America

North America holds the largest share of the computer cleaners market at approximately 35% in 2025, with the United States accounting for the majority of regional demand. Growth in this region is driven by high device penetration, advanced IT infrastructure, and strong enterprise spending on maintenance solutions. The presence of hyperscale data centers, cloud service providers, and technology companies significantly contributes to sustained demand for specialized cleaning products. Additionally, high consumer awareness regarding device performance optimization and preventive maintenance supports market expansion. The region also benefits from early adoption of eco-friendly cleaning technologies and premium product offerings.

Europe

Europe accounts for around 20% of the global market, with major contributions from Germany, the United Kingdom, and France. The region’s growth is strongly influenced by stringent environmental regulations, which are driving innovation in sustainable and non-toxic cleaning solutions. Increasing consumer awareness regarding electronic waste reduction and device longevity is further supporting demand. The presence of a well-established industrial and corporate sector, along with rising investments in digital infrastructure, is also contributing to steady market growth. Additionally, Europe’s focus on circular economy practices is encouraging the adoption of maintenance products that extend device lifecycles.

Asia-Pacific

Asia-Pacific represents approximately 30% of the market and is the fastest-growing region, with a CAGR exceeding 8.5%. China, India, and Japan are the key contributors, driven by rapid digitalization, increasing disposable incomes, and expanding IT ecosystems. Government initiatives promoting digital adoption, such as smart city programs and digital education, are significantly boosting demand for computing devices and associated maintenance products. India is emerging as a high-growth market due to rising laptop penetration, expansion of IT services, and growing SME digitization. Additionally, the region’s strong manufacturing base and increasing e-commerce penetration are facilitating wider product availability and affordability.

Latin America

Latin America holds about 7% of the market share, led by Brazil and Mexico. Growth in this region is driven by increasing adoption of consumer electronics, expanding internet penetration, and the rapid growth of e-commerce platforms. The rising middle-class population and improving access to affordable computing devices are further contributing to demand. Additionally, the gradual expansion of corporate IT infrastructure and small business digitization is supporting steady market growth, although price sensitivity remains a key factor influencing product adoption.

Middle East & Africa

The Middle East & Africa region accounts for approximately 8% of the global market. Growth is primarily driven by increasing investments in IT infrastructure, digital transformation initiatives, and the expansion of data centers in countries such as the UAE and Saudi Arabia. Government-led programs aimed at economic diversification and technological advancement are playing a crucial role in boosting demand for computing devices and maintenance solutions. Additionally, rising adoption of smart technologies and increasing enterprise IT spending are contributing to market growth. While the region is still developing in terms of overall market size, it presents significant long-term growth potential due to ongoing infrastructure development and increasing digital adoption.

Key Players in the Computer Cleaners Market

- 3M

- Illinois Tool Works (ITW)

- Falcon Safety Products

- Dust-Off

- Endust for Electronics

- Fellowes Brands

- Techspray

- MG Chemicals

- CRC Industries

- Staples (Private Label)

- Office Depot (Private Label)

- Green Clean

- Hama GmbH

- AF International

- iKlear