Compostable Toothbrush Market Size

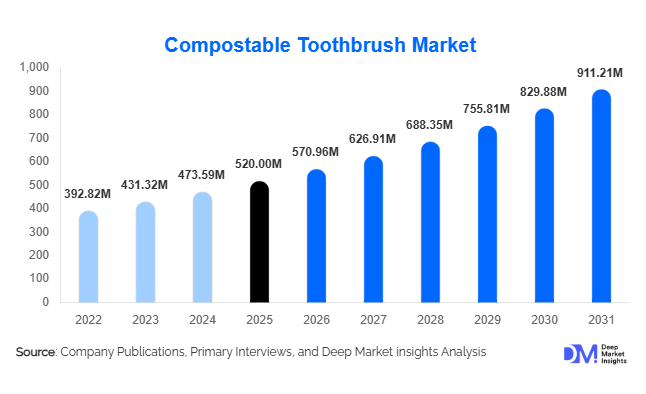

According to Deep Market Insights, the global compostable toothbrush market size was valued at USD 520 million in 2025 and is projected to grow from USD 570.96 million in 2026 to reach USD 911.21 million by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The compostable toothbrush market growth is primarily driven by increasing regulatory pressure on single-use plastics, rising consumer awareness regarding environmental sustainability, and expanding adoption of biodegradable personal care products across households and institutional sectors.

Key Market Insights

- Bamboo-based toothbrushes dominate the market, accounting for nearly 58% of total revenue in 2025 due to strong consumer perception of natural sustainability.

- Online retail channels lead distribution, contributing approximately 34% of global sales, driven by direct-to-consumer eco-brands and subscription models.

- North America holds the largest regional share (32%), supported by strong ESG commitments and premium consumer demand.

- Asia-Pacific is the fastest-growing region, expanding at over 12% CAGR due to rising middle-class adoption and export-driven production growth.

- Household consumers account for nearly 68% of demand, while hospitality and institutional procurement are the fastest-growing end-use segments.

- Technological advancements in biopolymers and fully compostable bristle systems are reshaping product innovation and premiumization strategies.

What are the latest trends in the compostable toothbrush market?

Shift Toward Fully Compostable Material Systems

Manufacturers are increasingly focusing on developing toothbrushes that are 100% compostable, including handles and bristles. While bamboo handles have achieved mainstream acceptance, bristles often remain partially biodegradable. Companies are investing in plant-based polymers such as PLA and castor oil–derived nylon alternatives to enhance full compostability. Certifications aligned with industrial compost standards are becoming critical for market differentiation, particularly in Europe and Japan. The transition from partially biodegradable to fully compostable systems is expected to significantly enhance product credibility and regulatory compliance.

Expansion of Subscription and Direct-to-Consumer Models

Subscription-based oral care models are gaining momentum, particularly in North America and Western Europe. Consumers increasingly prefer auto-replenishment systems that ensure timely toothbrush replacement every 3–4 months. Direct-to-consumer (DTC) brands leverage digital marketing, influencer campaigns, and sustainability storytelling to strengthen brand loyalty. E-commerce platforms now offer eco-certification labels and carbon footprint transparency, further supporting online adoption. This digital-first trend is reshaping pricing strategies and improving manufacturer margins through reduced reliance on intermediaries.

What are the key drivers in the compostable toothbrush market?

Stringent Plastic Reduction Regulations

Government initiatives aimed at reducing plastic waste are a primary growth driver. Regions such as Europe and parts of North America have implemented single-use plastic bans and extended producer responsibility (EPR) regulations. These policies compel manufacturers and institutional buyers to adopt biodegradable alternatives, directly accelerating compostable toothbrush demand. Public procurement guidelines increasingly prioritize sustainable products, creating long-term contracts for compliant manufacturers.

Growing Consumer Preference for Sustainable Personal Care

Consumers, particularly millennials and Gen Z, are actively shifting toward environmentally friendly daily-use products. Compostable toothbrushes align with this preference, offering a tangible reduction in plastic waste. Over 60% of eco-conscious consumers indicate willingness to pay a premium for sustainable oral care products. Social media campaigns and environmental awareness initiatives further amplify adoption.

What are the restraints for the global market?

Premium Pricing Compared to Plastic Alternatives

Compostable toothbrushes typically retail 30–70% higher than conventional plastic options. This pricing differential limits adoption in price-sensitive emerging markets. Scaling production and achieving material cost optimization remain necessary to improve affordability.

Limited Composting Infrastructure

Although products are labeled compostable, many regions lack industrial composting facilities. Inadequate disposal systems may reduce consumer trust and slow mass adoption, especially in developing countries.

What are the key opportunities in the compostable toothbrush industry?

Hospitality and Institutional Sustainability Programs

The global hospitality industry, valued at over USD 25 billion in annual amenities spending, is rapidly transitioning toward sustainable alternatives. Hotels, airlines, and cruise operators are replacing plastic toothbrushes with compostable variants to meet ESG commitments. Institutional procurement offers large-volume contracts and recurring revenue opportunities for manufacturers.

Emerging Market Penetration

Rising disposable income in countries such as India, Brazil, and Indonesia is creating new demand pools. Localization of manufacturing under initiatives such as “Make in India” and sustainable manufacturing incentives in China are lowering production costs and enhancing global competitiveness. Affordable product lines tailored to emerging markets represent a high-growth opportunity.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 520 Million |

| Market Size in 2026 | USD 570.96 Million |

| Market Size in 2031 | USD 911.21 Million |

| CAGR | 9.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

Bamboo-based toothbrushes dominate the compostable toothbrush market, contributing nearly 58% of global revenue in 2025. The leading position of bamboo is primarily driven by its rapid renewability (maturity cycle of 3–5 years), natural antimicrobial properties, and strong consumer association with sustainability. Bamboo is biodegradable under composting conditions and widely perceived as a zero-plastic alternative, making it highly attractive to environmentally conscious buyers. Additionally, well-established bamboo supply chains in China, Vietnam, and India ensure cost competitiveness and scalable manufacturing capacity, further reinforcing its leadership.

Bioplastic-based toothbrushes represent the fastest-growing material segment, supported by advancements in plant-derived polymers such as PLA and PHA. These materials provide improved durability and ergonomic molding capabilities while maintaining compostability standards. Growth is particularly strong in Europe and Japan, where regulatory frameworks encourage certified compostable plastics. Wood-based (non-bamboo) and composite plant-fiber alternatives maintain niche shares, primarily catering to premium brands seeking differentiation through aesthetics and specialized sustainability claims.

Bristle Type Insights

Castor oil–based nylon bristles lead the global market with approximately 46% market share in 2025. Their dominance is driven by the optimal balance between biodegradability and performance durability. Unlike fully plant-fiber bristles that may compromise strength, castor oil–derived nylon offers superior resilience, dentist-approved brushing efficiency, and consumer familiarity. This performance advantage has accelerated adoption across both household and institutional segments.

PLA bristles are gaining significant traction, particularly in Europe, where strict compostability certifications are influencing procurement standards. Meanwhile, charcoal-infused biodegradable bristles are popular among premium consumers due to perceived whitening benefits and antimicrobial positioning, allowing brands to command higher price premiums and expand into the value-added oral care segment.

Distribution Channel Insights

Online retail channels account for approximately 34% of total global revenue, making it the leading distribution segment. The primary driver behind this leadership is the rise of direct-to-consumer (DTC) eco-brands that leverage digital marketing, influencer partnerships, and subscription-based auto-replenishment models. Consumers increasingly prefer convenient quarterly replacement subscriptions aligned with dentist recommendations, boosting recurring sales and improving manufacturer margins.

Supermarkets and hypermarkets remain essential for mainstream penetration, especially in North America and Europe, where shelf placement alongside traditional oral care products enhances visibility. Specialty eco-stores serve environmentally conscious niche buyers, while institutional procurement through dental clinics, hotels, and airlines represents the fastest-growing channel. ESG-driven bulk purchasing agreements are significantly increasing institutional volumes, particularly in developed economies.

End-Use Insights

Household consumers represent the dominant end-use segment, accounting for nearly 68% of global demand, equivalent to over USD 350 million in 2025 revenue. The segment’s leadership is driven by rising awareness of plastic waste reduction, premiumization in daily-use products, and growing willingness among millennials and Gen Z consumers to pay for sustainable alternatives. Increased e-commerce penetration further strengthens household adoption.

The hospitality industry is the fastest-growing end-use segment, expanding at over 12% CAGR. Global hotel chains and airlines are phasing out plastic amenities to meet sustainability and ESG commitments, creating large-volume procurement opportunities. Healthcare and dental clinics are gradually transitioning toward compostable alternatives, particularly in Europe where regulatory pressure and sustainability mandates are stronger.

Explore more data points, trends and opportunities Download Free Sample Report

Compostable Toothbrush Market Segmentations

By Material Type

- Bamboo-Based Toothbrushes

- Bioplastic-Based Toothbrushes

- Wood-Based (Non-Bamboo) Toothbrushes

- Plant-Fiber Composite Toothbrushes

By Bristle Type

- Castor Oil–Based Nylon Bristles

- PLA (Polylactic Acid) Bristles

- Charcoal-Infused Biodegradable Bristles

- Fully Compostable Plant-Fiber Bristles

By Product Type

- Adult Compostable Toothbrushes

- Children’s Compostable Toothbrushes

- Travel/Portable Toothbrushes

- Electric Compostable Toothbrush Handles

By Distribution Channel

- Online Retail / E-Commerce

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Specialty Eco-Stores

- Institutional & Dental Procurement

By End-Use

- Household Consumers

- Hospitality Industry

- Healthcare & Dental Clinics

- Corporate & Institutional Sustainability Programs

Regional Insights

North America

North America leads the global market with a 32% share in 2025. The United States accounts for nearly 75% of regional demand, driven by high consumer awareness regarding plastic pollution, strong penetration of eco-friendly DTC brands, and well-established e-commerce infrastructure. Federal and state-level plastic reduction initiatives, combined with corporate ESG commitments from the hospitality and healthcare sectors, are key growth drivers. Canada also demonstrates steady expansion, supported by regulatory alignment with sustainability standards and increasing availability of compostable products in mainstream retail chains.

Europe

Europe holds approximately 29% of the global market share, with Germany, the U.K., and France as leading contributors. Germany alone represents nearly 22% of European demand, supported by stringent plastic waste regulations and a highly eco-conscious consumer base. The European Union’s circular economy action plans and extended producer responsibility (EPR) frameworks are strong structural drivers encouraging compostable alternatives. Additionally, Europe’s advanced composting infrastructure supports higher product credibility and consumer trust, accelerating adoption rates.

Asia-Pacific

Asia-Pacific accounts for approximately 27% of global revenue and is the fastest-growing region, expanding at over 12% CAGR. China dominates as both the largest manufacturing hub and an increasingly important domestic consumption market. Government-backed sustainable manufacturing initiatives and export-driven production growth significantly contribute to regional expansion. India exhibits the highest growth rate at nearly 14% CAGR, driven by rising middle-class environmental awareness, expanding e-commerce penetration, and policy support under domestic manufacturing programs. Japan contributes through innovation in biodegradable bristle technologies and high-quality sustainable consumer goods demand.

Latin America

Latin America represents around 7% of global demand, led by Brazil and Mexico. Growth drivers include expanding urban middle-class populations, increasing awareness of environmental issues, and gradual retail penetration of eco-friendly personal care products. While price sensitivity remains a restraint, premium urban consumers are supporting steady market expansion.

Middle East & Africa

The Middle East & Africa account for nearly 5% of global demand. The UAE leads adoption due to strong hospitality sector sustainability initiatives and high disposable income levels. South Africa represents the largest African consumer market, supported by growing environmental awareness and retail availability. Regional growth is primarily driven by tourism-linked institutional demand and increasing ESG commitments from multinational hotel operators operating within the region.

Key Players in the Compostable Toothbrush Market

- The Humble Co.

- Brush with Bamboo

- Colgate-Palmolive

- WooBamboo

- Hydrophil

- Georganics

- Environmental Toothbrush

- Mabboo

- The Green Root

- Pangea Organics

- Truthbrush

- The Bam & Boo

- Colibri

- Bambooth

- Mother’s Vault