Compostable Tableware Market Size

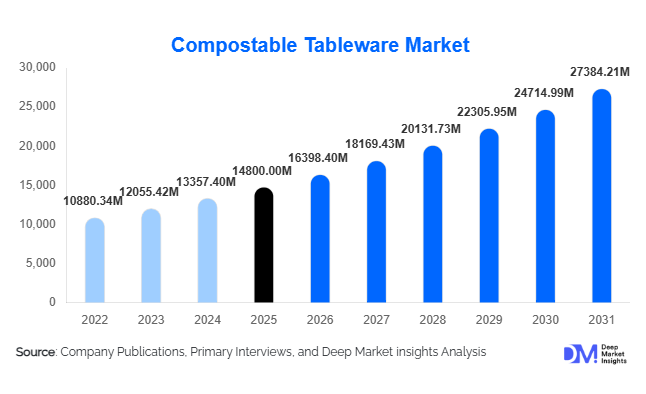

According to Deep Market Insights, the global compostable tableware market size was valued at USD 14,800 million in 2025 and is projected to grow from USD 16, 398.40 million in 2026 to reach USD 27,384.21 million by 2031, expanding at a CAGR of 10.8% during the forecast period (2026–2031). The compostable tableware market growth is primarily driven by stringent regulations on single-use plastics, increasing consumer awareness toward sustainable products, and the rapid expansion of the global foodservice and takeaway ecosystem.

Key Market Insights

- Global regulations banning single-use plastics are accelerating the adoption of compostable alternatives across food service and institutional sectors.

- Bagasse-based products dominate the market due to cost efficiency, durability, and widespread availability.

- Asia-Pacific leads the global market, driven by large-scale manufacturing in China and India and strong export demand.

- Foodservice remains the largest end-use segment, accounting for nearly half of global demand due to QSR expansion.

- B2B distribution channels dominate, with bulk procurement by restaurants, caterers, and institutions.

- Technological advancements in biodegradable materials are improving performance and reducing cost gaps with plastic alternatives.

What are the latest trends in the compostable tableware market?

Shift Toward Fiber-Based Materials

The market is witnessing a strong transition toward fiber-based materials such as bagasse, bamboo, and palm leaf. These materials offer superior strength, heat resistance, and compostability compared to traditional bioplastics. Manufacturers are increasingly investing in molded fiber technologies to produce high-quality, durable tableware suitable for hot and cold food applications. This trend is particularly prominent in North America and Europe, where regulatory compliance and consumer expectations are driving demand for natural-material products. Additionally, fiber-based products align well with circular economy initiatives, as they are derived from agricultural waste and reduce landfill dependency.

Customization and Branding in Food Packaging

Compostable tableware is evolving beyond functionality to become a branding tool for businesses. Restaurants, cafes, and food delivery platforms are increasingly opting for customized designs, embossed logos, and printed messaging on compostable products. This trend enhances brand visibility while reinforcing sustainability commitments. The rise of cloud kitchens and online food delivery has further amplified this demand, as packaging becomes a key touchpoint for customer experience. Manufacturers are responding by offering flexible customization options and low minimum order quantities, making branded compostable tableware accessible to both large chains and small businesses.

What are the key drivers in the compostable tableware market?

Stringent Environmental Regulations

Governments across the globe are implementing strict policies to curb plastic waste, including bans on single-use plastics and mandates for biodegradable alternatives. Regions such as Europe and North America have introduced comprehensive frameworks requiring foodservice providers to transition to compostable or recyclable materials. These regulations are creating a strong demand pipeline and encouraging manufacturers to scale production capacities. Compliance with standards such as EN13432 and ASTM D6400 has become essential for market participation, further formalizing the industry.

Expansion of the Global Foodservice Industry

The rapid growth of quick-service restaurants (QSRs), cafes, and food delivery platforms is significantly driving demand for disposable tableware. With increasing urbanization and changing lifestyles, consumers are relying more on takeaway and delivery services. Compostable tableware offers an eco-friendly solution for these high-volume applications. Large food chains are also adopting sustainable packaging as part of their ESG commitments, further boosting market growth. The rising penetration of cloud kitchens is expected to sustain this demand trajectory over the forecast period.

What are the restraints for the global market?

Higher Costs Compared to Conventional Plastics

Despite growing demand, compostable tableware products remain relatively expensive compared to traditional plastic alternatives. The cost differential, which can range between 20% and 50%, poses a significant challenge for adoption in price-sensitive markets. Small and medium-sized businesses, particularly in developing economies, often find it difficult to absorb these higher costs. While economies of scale and technological advancements are gradually reducing prices, cost competitiveness remains a key barrier to widespread adoption.

Limited Composting Infrastructure

The effectiveness of compostable tableware depends heavily on the availability of industrial composting facilities. In many regions, particularly in developing countries, such infrastructure is limited or underdeveloped. This results in compostable products being disposed of in landfills, reducing their environmental benefits. The lack of consumer awareness and proper waste segregation systems further exacerbates this issue, posing a challenge to the market’s long-term sustainability.

What are the key opportunities in the compostable tableware industry?

Growth in Food Delivery and Cloud Kitchens

The rapid expansion of food delivery platforms and cloud kitchens presents a significant growth opportunity for compostable tableware manufacturers. With millions of daily orders globally, the demand for sustainable packaging solutions is rising sharply. Companies that can offer lightweight, durable, and cost-effective compostable products tailored for delivery applications are well-positioned to capture this high-volume market segment. Partnerships with food aggregators and QSR chains can further enhance market penetration and brand visibility.

Advancements in Biodegradable Material Technologies

Technological innovation in biodegradable materials is creating new opportunities for product differentiation and performance enhancement. Developments in PLA blends, starch-based polymers, and hybrid materials are improving strength, heat resistance, and moisture barriers. These advancements are enabling compostable tableware to compete directly with plastic in terms of functionality. Companies investing in R&D and material innovation can tap into premium market segments and expand their application range across diverse end-use industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14800 Million |

| Market Size in 2026 | USD 16398.40 Million |

| Market Size in 2031 | USD 27384.21 Million |

| CAGR | 10.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Plates dominate the compostable tableware market, accounting for approximately 28% of the total market share in 2025, driven primarily by their universal applicability across multiple end-use industries. Their leadership is supported by high consumption volumes in foodservice, catering, and institutional settings where plates serve as a primary serving medium. The ease of manufacturing using molded fiber technologies, particularly from bagasse and paper pulp, significantly reduces production complexity and cost, making them commercially viable at scale. Additionally, plates offer superior structural strength and heat resistance, making them suitable for both hot and cold food applications. Bowls and containers are rapidly gaining traction due to the surge in takeaway and food delivery services, where spill-proof and compartmentalized packaging is essential. Meanwhile, cutlery and cups are witnessing steady growth as complementary products, often bundled with meal kits, with innovation focusing on durability and heat resistance to match plastic alternatives.

Application Insights

Foodservice applications represent the largest segment, contributing nearly 45% of the global market in 2025, primarily driven by the rapid expansion of quick-service restaurants (QSRs), cafes, and cloud kitchens. The segment’s dominance is reinforced by stringent regulatory mandates requiring sustainable alternatives to plastic, along with corporate sustainability commitments from global food chains. The high frequency of disposable usage in takeaway and delivery formats further amplifies demand. Catering and events are emerging as the fastest-growing applications, driven by increasing environmental compliance requirements for large-scale gatherings, corporate events, and social functions. Institutional applications, including schools, hospitals, and corporate offices, are also expanding steadily, supported by government procurement policies and sustainability targets. These segments are increasingly adopting compostable tableware to align with ESG goals and reduce environmental impact.

Distribution Channel Insights

B2B distribution channels dominate the market, accounting for approximately 65% of total sales in 2025, primarily due to bulk procurement by foodservice operators, catering companies, and institutional buyers. This segment benefits from long-term supply contracts, consistent order volumes, and cost efficiencies associated with large-scale purchasing. The dominance of B2B channels is further strengthened by regulatory compliance requirements, which often mandate businesses to adopt compostable solutions. On the other hand, B2C channels, including retail and e-commerce, are witnessing rapid growth as environmentally conscious consumers increasingly adopt sustainable products for household use. The rise of online marketplaces and direct-to-consumer platforms is enhancing accessibility and product visibility, particularly in developed regions, while also enabling smaller manufacturers to reach a broader customer base.

End-Use Industry Insights

The foodservice industry remains the primary end-use segment, with a market size exceeding USD 6,500 million in 2025 and a growth rate of around 11% CAGR. This dominance is driven by the high volume of disposable tableware usage in restaurants, QSRs, and takeaway outlets, coupled with increasing regulatory pressure to eliminate plastic waste. Catering and events represent the fastest-growing segment, expanding at approximately 12–13% CAGR, fueled by sustainability mandates for corporate events, weddings, and public gatherings. Institutional demand from schools, hospitals, and corporate offices is also increasing steadily, supported by government-led sustainability initiatives and procurement guidelines. Emerging applications in travel and hospitality, including airlines, railways, and hotels, are further contributing to market expansion, as these sectors adopt lightweight, eco-friendly disposables to enhance sustainability credentials while maintaining operational efficiency.

Explore more data points, trends and opportunities Download Free Sample Report

Compostable Tableware Market Segmentations

By Product Type

- Plates

- Bowls

- Cups & Glasses

- Cutlery

- Trays & Containers

- Straws & Stirrers

- Others

By Raw Material Type

- Bagasse

- Paper & Paperboard

- PLA

- Starch-based Polymers

- Bamboo

- Palm Leaf

- Wood-based Materials

- Others

By Compostability Type

- Industrial Compostable

- Home Compostable

By Application

- Foodservice

- Catering & Events

- Institutional

- Household/Retail

- Travel & Hospitality

By Distribution Channel

- B2B

- B2C

Regional Insights

North America

North America holds a significant share of approximately 30% of the global market in 2025, with the United States accounting for the majority of regional demand, exceeding USD 3,800 million. The region’s growth is primarily driven by stringent state-level regulations banning single-use plastics, particularly in states such as California and New York. High consumer awareness regarding environmental sustainability and strong adoption by large QSR chains further support market expansion. Additionally, well-established composting infrastructure and corporate ESG commitments are accelerating the transition toward compostable tableware. Canada is also witnessing steady growth, supported by nationwide policies promoting sustainable packaging and increasing institutional adoption.

Europe

Europe accounts for around 28% of the global market share, supported by comprehensive regulatory frameworks such as the EU Single-Use Plastics Directive. Countries including Germany, France, and the UK are leading the region, with Germany contributing nearly 20% of regional demand. The presence of advanced waste management and industrial composting infrastructure is a key driver, enabling effective disposal and recycling of compostable products. Additionally, strong consumer preference for eco-friendly products and widespread adoption by foodservice chains are fueling demand. Government incentives and sustainability certifications are further encouraging businesses to transition to compostable alternatives.

Asia-Pacific

Asia-Pacific leads the global market with approximately 32% share in 2025 and is also the fastest-growing region. China and India are the primary growth engines, with India registering a CAGR exceeding 13%. The region’s growth is driven by abundant availability of raw materials such as bagasse, low-cost manufacturing capabilities, and increasing government restrictions on plastic usage. Rapid urbanization, expanding middle-class populations, and the proliferation of food delivery platforms are further boosting demand. Additionally, Asia-Pacific serves as a major export hub, supplying compostable tableware to North America and Europe, thereby strengthening its global market position.

Latin America

Latin America is experiencing moderate growth, led by Brazil and Mexico, with a growth rate of around 9–10% CAGR. The region’s expansion is driven by increasing regulatory pressure to reduce plastic waste and growing urbanization, which is boosting demand for takeaway and food delivery services. Rising environmental awareness among consumers and gradual improvements in waste management infrastructure are also contributing to market growth. However, cost sensitivity remains a challenge, limiting faster adoption across smaller businesses.

Middle East & Africa

The Middle East and Africa region is witnessing gradual growth, driven by countries such as the UAE and South Africa. The hospitality and tourism sectors play a crucial role in driving demand, as hotels, airlines, and event organizers adopt sustainable practices to align with global environmental standards. Government initiatives promoting sustainability, particularly in the UAE, are encouraging the adoption of compostable tableware. Additionally, increasing international tourism and large-scale events are creating demand for eco-friendly disposable solutions. However, limited composting infrastructure in several parts of the region remains a key challenge to widespread adoption.

Key Players in the Compostable Tableware Market

- Huhtamaki Oyj

- Dart Container Corporation

- Georgia-Pacific LLC

- Vegware Ltd.

- Eco-Products Inc.

- Pactiv Evergreen Inc.

- Genpak LLC

- Biopak Pty Ltd

- Sabert Corporation

- Lollicup USA Inc.

- Be Green Packaging

- StalkMarket

- Natural Tableware

- Ecoware Solutions Pvt Ltd

- GreenGood USA