Commercial Kitchen Equipment and Appliances Market Size

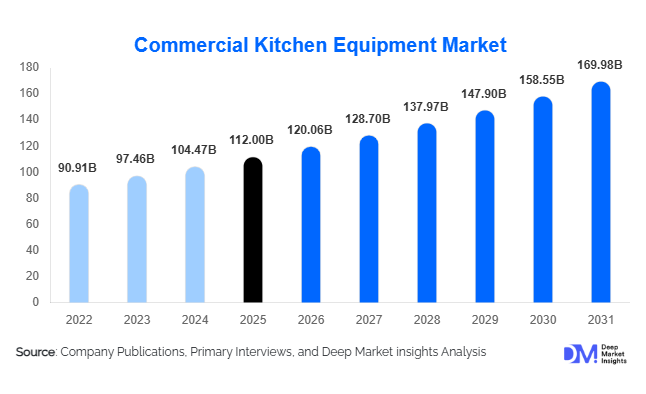

According to Deep Market Insights, the global commercial kitchen equipment and appliances market size was valued at USD 112.0 billion in 2025 and is projected to grow from USD 120.06 billion in 2026 to reach USD 169.98 billion by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The market growth is primarily driven by the rising demand from quick-service restaurants (QSRs), cloud kitchens, and institutional catering, alongside increasing adoption of smart, energy-efficient, and automated kitchen equipment in both developed and emerging economies.

Key Market Insights

- Cooking equipment dominates the market, accounting for 32% of the total market share in 2025, as it forms the core of food preparation and is frequently upgraded to meet operational and efficiency standards.

- Asia-Pacific is the largest regional market, contributing 38% of global demand, fueled by rapid urbanization, increasing disposable income, and growing QSR and hospitality sectors in China, India, and Japan.

- Electric equipment leads globally in fuel-type adoption (58% share) due to energy efficiency and compliance with environmental regulations.

- Quick-service restaurants (QSRs) remain the fastest-growing end-use segment, accounting for 28% of market demand, driven by the proliferation of delivery services and standardized kitchen setups.

- Smart and semi-automated equipment adoption is rising, with semi-automated appliances capturing 50% of the automation segment as businesses balance cost, efficiency, and operational productivity.

- Direct OEM sales are dominant, representing 45% of distribution, as large buyers prefer customized solutions, after-sales support, and bulk procurement agreements.

What are the latest trends in the commercial kitchen equipment market?

Smart & Connected Kitchen Adoption

IoT-enabled and AI-integrated appliances are transforming commercial kitchens into data-driven, efficient environments. Smart ovens, predictive maintenance tools, and connected refrigeration systems enable operators to optimize energy use, reduce downtime, and streamline operations. The trend is particularly pronounced in North America and Europe, where regulatory pressure and labor cost considerations accelerate technology adoption. These solutions allow centralized monitoring of multiple kitchen locations, predictive alerts for equipment faults, and remote control of appliances, making them attractive to large QSR chains and institutional operators.

Energy Efficiency and Sustainable Equipment

Growing emphasis on environmental sustainability and energy conservation is encouraging the replacement of older, high-energy-consuming appliances with energy-efficient models. Equipment certified by ENERGY STAR or similar programs is increasingly demanded by restaurant chains and hotels to reduce utility costs and comply with regulatory mandates. Manufacturers are responding by introducing advanced heat recovery systems, low-emission fryers, and high-efficiency refrigeration units that reduce both operational expenses and carbon footprint.

Compact & Modular Equipment for Cloud Kitchens

The surge of cloud kitchens has created a demand for compact, modular, and high-output kitchen setups. Operators prefer space-efficient, multipurpose appliances that can handle high-volume preparation in limited areas. This trend is particularly strong in Asia-Pacific and North America, where the delivery economy is rapidly expanding. Manufacturers are developing modular cooking lines, stackable refrigeration units, and integrated food preparation systems to meet the operational and cost requirements of these emerging kitchens.

What are the key drivers in the commercial kitchen equipment market?

Growth of Quick Service Restaurants and Institutional Catering

The rapid global expansion of QSR chains and institutional catering operations is significantly boosting demand for commercial kitchen equipment. Standardized appliances are necessary to maintain uniform food quality, efficiency, and safety across multiple outlets. High-volume food preparation requirements have accelerated investment in cooking, refrigeration, and food processing equipment, making the QSR segment a leading contributor to market growth.

Technological Advancements in Automation

Automation, including semi-automated and fully automated kitchen equipment, is enhancing operational efficiency while reducing labor dependency. Smart appliances equipped with IoT connectivity and predictive maintenance improve workflow management, minimize downtime, and increase profitability. These technologies are particularly attractive to large chains and institutional buyers seeking consistent performance and reduced operating costs.

Regulatory Push for Energy Efficiency

Stringent energy consumption and environmental regulations in Europe and North America are driving the adoption of energy-efficient and environmentally compliant equipment. Replacement of outdated high-energy appliances and investment in smart systems are key growth drivers, providing opportunities for both OEMs and end users to align with sustainability initiatives.

What are the restraints for the global market?

High Capital Expenditure

Commercial kitchen equipment, especially automated or smart systems, requires significant upfront investment. Small-scale operators and start-ups often find it difficult to absorb these costs, limiting market penetration. Leasing and financing options are emerging, but high initial capital remains a barrier to entry for many potential buyers.

Raw Material Price Volatility

Fluctuating costs of stainless steel, aluminum, and electronic components directly impact manufacturing expenses, translating into higher prices for end-users. This unpredictability can hinder adoption, reduce profit margins, and create competitive pricing pressures among global players.

What are the key opportunities in the commercial kitchen equipment market?

Expansion of Cloud Kitchens and Delivery-Only Models

Cloud kitchens are transforming foodservice operations by reducing real estate costs and focusing on delivery efficiency. These kitchens require high-output, compact, and modular appliances. Equipment manufacturers can tap into this segment by providing customized solutions, lease-based offerings, and integrated smart systems tailored to cloud kitchen workflows. Rapid adoption in Asia-Pacific and North America makes this one of the most lucrative growth opportunities.

Smart & Connected Equipment Integration

The integration of IoT, AI, and cloud-based management systems in commercial kitchens opens recurring revenue opportunities for manufacturers. Predictive maintenance, remote monitoring, and performance analytics appeal to large chain operators seeking efficiency and cost control. Companies investing in software-enabled appliances and service contracts can capture premium market segments and create long-term customer loyalty.

Emerging Market Demand & Government Support

Developing regions in Asia, the Middle East, and Africa are witnessing strong foodservice infrastructure expansion. Government initiatives promoting industrial modernization, energy-efficient appliances, and food safety standards are increasing adoption rates. This environment offers opportunities for both multinational and local manufacturers to expand their presence and address rising domestic demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 112.0 Billion |

| Market Size in 2026 | USD 120.06 Billion |

| Market Size in 2031 | USD 169.98 Billion |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Cooking equipment continues to dominate the global commercial kitchen equipment market, accounting for approximately 32% of the total market share in 2025. This segment includes ovens, fryers, grills, and steamers, which are central to all foodservice operations. The dominance is primarily driven by high replacement frequency, continuous innovation in cooking technologies, and the need for standardized food preparation across QSR chains and large hospitality groups. Additionally, the shift toward energy-efficient and multifunctional cooking appliances is further accelerating demand. Refrigeration equipment holds nearly 25% market share and is witnessing strong growth due to increasing regulatory emphasis on food safety and temperature control. The rising adoption of energy-efficient refrigeration systems, coupled with the expansion of cold chain infrastructure and prepared food retailing, is driving this segment forward. Food preparation equipment accounts for around 18% share, supported by the rapid growth of cloud kitchens and QSRs that require high-speed, consistent, and automated food processing solutions.

Warewashing, storage, and handling equipment collectively contribute approximately 15% of the market. Growth in this segment is driven by stricter hygiene regulations, increasing labor costs, and the need for operational efficiency in high-volume kitchens. Automation in dishwashing and smart storage solutions is becoming increasingly common, particularly in developed markets where labor optimization is a key priority.

Application Insights

Quick-service restaurants (QSRs) and cloud kitchens represent the largest and fastest-growing application segments in the commercial kitchen equipment market. These formats rely heavily on standardized, high-efficiency kitchen setups to ensure consistency, speed, and scalability. The global expansion of food delivery platforms and franchise-based restaurant models is a key driver, requiring compact, modular, and high-performance equipment tailored for high-output environments. Institutional catering, including hospitals, educational institutions, and defense facilities, is a steadily growing segment, driven by increasing infrastructure investments and the need for hygienic, reliable, and large-capacity food preparation systems. This segment prioritizes durability, compliance with food safety standards, and cost-effective long-term operations.

The hotels and hospitality sector remains a premium application segment, characterized by high adoption of technologically advanced, energy-efficient, and aesthetically integrated kitchen appliances. Luxury hotels and resorts are increasingly investing in automated and smart kitchen systems to enhance operational efficiency and guest experience. Retail food chains and supermarkets are emerging as a significant growth area, with increasing investment in in-store food preparation and ready-to-eat meal offerings. This trend is driving demand for integrated cooking, refrigeration, and display solutions, particularly in urban markets where convenience foods are gaining popularity.

Distribution Channel Insights

Direct sales from original equipment manufacturers (OEMs) to end users dominate the market, accounting for approximately 45% of total distribution. This channel is preferred by large QSR chains, hotels, and institutional buyers due to the need for customized solutions, bulk procurement, and comprehensive after-sales services. Direct engagement also enables manufacturers to offer integrated kitchen solutions and long-term maintenance contracts, strengthening customer relationships. Distributor and dealer networks play a crucial role in catering to small and medium-sized enterprises, particularly in emerging markets. These channels provide localized support, faster delivery, and access to a wide range of products from multiple manufacturers.

Online and marketplace-based sales are gaining traction, especially for standardized and smaller equipment. Digital platforms offer price transparency, convenience, and access to a broader customer base. Additionally, innovative business models such as leasing, subscription-based equipment usage, and pay-per-use solutions are emerging, particularly among cloud kitchens and start-ups, enabling lower upfront investment and operational flexibility.

Automation Level Insights

Semi-automated equipment leads the automation segment, accounting for nearly 50% of the market share, as it offers an optimal balance between cost and operational efficiency. These systems are widely adopted across QSRs and mid-sized foodservice operators seeking to enhance productivity without incurring the high costs associated with fully automated kitchens. Fully automated and smart kitchen equipment is witnessing rapid adoption, particularly among large restaurant chains and institutional operators. These systems leverage IoT, AI, and robotics to streamline operations, reduce labor dependency, and improve consistency. The growing labor shortage in developed economies and the need for operational efficiency are key drivers for this segment.

Manual equipment continues to serve small-scale and traditional foodservice providers, especially in developing regions. However, its market share is gradually declining due to increasing demand for efficiency, consistency, and compliance with hygiene and safety standards.

Explore more data points, trends and opportunities Download Free Sample Report

Commercial Kitchen Equipment Market Segmentations

By Product Type

- Cooking Equipment

- Refrigeration Equipment

- Food Preparation Equipment

- Warewashing Equipment

- Storage & Handling Equipment

- Ventilation & Exhaust Systems

By Application

- Quick Service Restaurants (QSRs)

- Full-Service Restaurants (FSRs)

- Hotels & Hospitality

- Institutional Catering

- Cloud Kitchens / Ghost Kitchens

- Retail Food Chains & Supermarkets

By Distribution Channel

- Direct Sales

- Distributor & Dealer Networks

- Online & Marketplace Sales

- Leasing & Subscription-Based Models

By Automation Level

- Manual Equipment

- Semi-Automated Equipment

- Fully Automated / Smart Kitchen Equipment

Regional Insights

Asia-Pacific

Asia-Pacific remains the largest market, accounting for approximately 38% of global demand in 2025, with China, India, and Japan as key contributors. The region’s dominance is driven by rapid urbanization, rising disposable incomes, and a growing middle-class population with increasing demand for dining-out and food delivery services. The expansion of QSR chains, cloud kitchens, and retail food outlets is a major growth driver. Additionally, strong manufacturing capabilities in China and government initiatives supporting domestic production and food processing industries further boost market growth. India is emerging as the fastest-growing market in the region, supported by favorable policies, increasing foreign investments, and rapid expansion of organized foodservice sectors.

North America

North America holds around 26% of the global market share, led by the United States. The region’s growth is driven by high labor costs, which are accelerating the adoption of automated and smart kitchen equipment. Strict regulatory standards related to energy efficiency and food safety are also pushing businesses to upgrade their existing equipment. The presence of large QSR chains, advanced hospitality infrastructure, and high consumer spending on dining out further contribute to strong demand. Canada complements regional growth through increasing investments in institutional catering and hospitality modernization.

Europe

Europe is a mature yet steadily growing market, with key countries including Germany, France, and the United Kingdom. Growth in this region is primarily driven by stringent environmental and energy efficiency regulations, which are encouraging the adoption of sustainable and energy-efficient kitchen equipment. Additionally, the strong presence of premium hospitality and fine dining sectors supports demand for technologically advanced appliances. Increasing focus on reducing carbon emissions and improving operational efficiency is further accelerating replacement demand across the region.

Middle East & Africa

The Middle East & Africa region is witnessing significant growth, driven by strong investments in tourism, hospitality, and large-scale infrastructure projects. Countries such as the UAE, Saudi Arabia, and Qatar are leading demand due to their focus on developing luxury hotels, restaurants, and entertainment hubs. Government initiatives aimed at diversifying economies beyond oil, particularly in Saudi Arabia, are boosting the foodservice sector. In Africa, increasing urbanization, rising middle-class income, and expanding hospitality infrastructure are contributing to growing demand for commercial kitchen equipment. Export-driven demand from regional distributors also plays a key role.

Latin America

Latin America is experiencing steady growth, with Brazil and Mexico as the primary markets. The region’s expansion is driven by increasing urbanization, growth in QSR chains, and rising consumer preference for dining out and convenience foods. Economic development and improving retail infrastructure are supporting the adoption of modern kitchen equipment. Additionally, international restaurant chains entering the region are driving demand for standardized and high-efficiency kitchen setups, contributing to long-term market growth.

Investment & CapEx Trends

Governments are investing in food processing and hospitality infrastructure, promoting energy-efficient and standardized kitchen adoption. Private CapEx is rising in QSR chains and institutional catering facilities, including factory expansions and equipment modernization. Initiatives like “Make in India” and China’s industrial modernization programs further support market growth.

Key Players in the Commercial Kitchen Equipment Market

- Middleby Corporation

- ITW Food Equipment Group

- Rational AG

- Electrolux Professional

- Ali Group

- Hoshizaki Corporation

- Welbilt Inc.

- Dover Corporation

- Fujimak Corporation

- Duke Manufacturing

- Alto-Shaam

- Midea Group

- Haier Smart Home

- Samsung Professional Appliances

- LG Electronics