Coffin Market Size

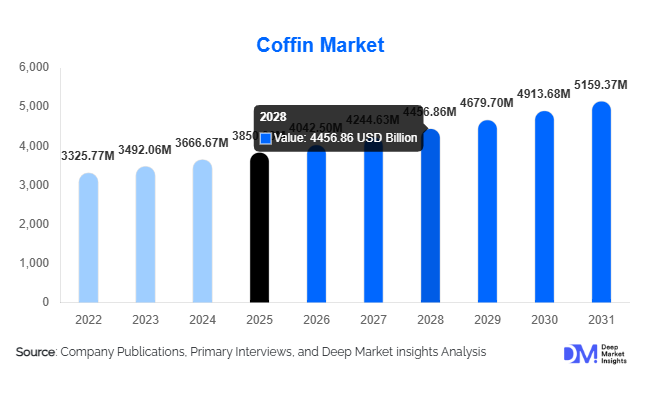

According to Deep Market Insights, the global coffin market size was valued at USD 3,850 million in 2025 and is projected to grow from USD 4042.50 million in 2026 to reach USD 5,159.37 million by 2031, expanding at a CAGR of 5.0% during the forecast period (2026–2031). The coffin market growth is primarily driven by demographic aging, increasing formalization of funeral services, and the rising demand for eco-friendly and customized burial solutions. While traditional wooden coffins continue to dominate due to cultural acceptance, emerging trends such as biodegradable coffins and digital sales channels are reshaping the competitive landscape globally.

Key Market Insights

- Wooden coffins remain the dominant product category, accounting for over 50% of global demand due to traditional and cultural preferences.

- Eco-friendly and biodegradable coffins are gaining traction, driven by environmental awareness and regulatory support for green burials.

- North America leads the global market, supported by high funeral expenditure and established funeral infrastructure.

- Asia-Pacific is the fastest-growing region, driven by population growth, urbanization, and evolving funeral practices.

- Funeral homes dominate distribution channels, though online platforms are rapidly expanding with increased price transparency.

- Cremation trends are reshaping demand patterns, shifting consumption toward lower-cost coffin alternatives.

What are the latest trends in the coffin market?

Rising Demand for Eco-Friendly Coffins

The shift toward sustainability is one of the most prominent trends in the coffin market. Consumers are increasingly opting for biodegradable materials such as bamboo, wicker, and cardboard to minimize environmental impact. Governments and environmental bodies are promoting green burial practices, particularly in Europe and North America, encouraging the use of sustainably sourced materials. Manufacturers are responding by introducing certified eco-friendly coffins that decompose naturally and reduce carbon emissions. This trend is also supported by the growth of green cemeteries and eco-conscious funeral planning services, which are influencing purchasing decisions across developed markets.

Digitalization of Funeral Services and Sales Channels

The integration of digital platforms into funeral services is transforming how coffins are marketed and sold. Online platforms enable consumers to compare products, customize designs, and purchase directly, bypassing traditional funeral home markups. Virtual catalogs, 3D visualization tools, and transparent pricing models are improving customer engagement and accessibility. This trend is particularly strong in developed markets, where digital adoption is high, and is gradually expanding into emerging regions. The rise of direct-to-consumer sales is also intensifying competition and encouraging innovation in product offerings.

What are the key drivers in the coffin market?

Aging Global Population

The increasing global elderly population is a fundamental driver of the coffin market. Regions such as North America, Europe, and Japan are experiencing significant demographic shifts, leading to higher mortality rates and consistent demand for funeral products. This demographic trend ensures long-term market stability and predictable demand patterns.

Expansion of Formal Funeral Services

Urbanization and changing social structures are driving the adoption of professional funeral services, particularly in emerging economies. Traditional home-based funerals are being replaced by organized services, increasing demand for standardized coffin products. This shift is especially evident in Asia-Pacific and Africa, where rising incomes and urban lifestyles are influencing consumer behavior.

What are the restraints for the global market?

Increasing Cremation Rates

The growing preference for cremation is a significant restraint for the coffin market. In countries such as the United States and Japan, cremation rates exceed 60–70%, reducing demand for traditional burial coffins. Although cremation still requires coffins, these are typically lower-cost options, impacting overall market revenue.

High Cost of Premium Coffins

Premium and luxury coffins can be expensive, limiting their adoption in price-sensitive markets. Economic uncertainties and rising funeral costs are encouraging consumers to opt for more affordable alternatives, which can affect profit margins for manufacturers focusing on high-end segments.

What are the key opportunities in the coffin industry?

Growth of Green Burial Solutions

The increasing adoption of environmentally sustainable burial practices presents a major opportunity for market players. Companies investing in biodegradable materials and eco-certifications can capture growing demand, particularly in Europe and North America. Green burial solutions are expected to witness strong growth as environmental concerns continue to influence consumer preferences.

Expansion in Emerging Markets

Emerging economies such as India, China, and Nigeria offer significant growth potential due to population expansion and increasing formalization of funeral services. Rising middle-class incomes and urbanization are driving demand for standardized coffin products, creating opportunities for both local and international manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3850 Million |

| Market Size in 2026 | USD 4042.50 Million |

| Market Size in 2031 | USD 5159.37 Million |

| CAGR | 5.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Wood coffins continue to dominate the global market, accounting for approximately 52% of the total revenue share in 2025. This dominance is primarily driven by deep-rooted cultural and religious preferences, particularly across North America, Europe, and parts of Africa, where traditional burial practices emphasize the use of natural and aesthetically refined materials. Hardwood coffins such as oak and mahogany are especially preferred in premium segments due to their durability and symbolic value, while softwood variants cater to cost-sensitive consumers. The segment’s leadership is further reinforced by strong supply chain availability and established manufacturing ecosystems.

Metal coffins, particularly steel variants, hold a significant share in developed markets such as the United States, where durability, sealing features, and premium positioning are key purchase drivers. The demand for metal coffins is also supported by higher disposable incomes and consumer willingness to invest in long-lasting burial solutions. Meanwhile, biodegradable coffins are the fastest-growing segment, driven by rising environmental awareness, increasing adoption of green burial practices, and regulatory encouragement in regions such as Europe and North America. Materials such as bamboo, wicker, and recycled cardboard are gaining traction due to their low environmental impact. Composite and fiberglass coffins cater to niche applications, particularly in regions requiring cost efficiency and durability under varying climatic conditions. Although their market share remains relatively limited, they are increasingly being adopted in emerging markets due to affordability and ease of mass production.

Application Insights

The traditional burial segment remains the leading application, accounting for approximately 65% of global demand in 2025. This dominance is driven by strong cultural, religious, and societal norms across regions such as Africa, Latin America, and parts of Europe, where burial practices are deeply embedded in social traditions. Additionally, government regulations and cemetery infrastructure in these regions continue to support burial practices, sustaining demand for standard and premium coffins. Cremation-compatible coffins are gaining significant traction, particularly in developed markets such as North America, Japan, and parts of Europe, where cremation rates have exceeded 60–70%. The shift toward cremation is largely driven by lower costs, urban space constraints, and changing consumer preferences. As a result, demand is increasing for lightweight, cost-effective coffins designed specifically for cremation processes.

Green burial applications are emerging as a high-growth segment, expanding at a faster pace than the overall market. This growth is supported by environmental regulations, rising consumer awareness regarding carbon footprints, and the increasing availability of eco-certified burial grounds. The segment is also benefiting from changing consumer attitudes toward sustainability and natural decomposition.

Distribution Channel Insights

Funeral homes remain the dominant distribution channel, accounting for nearly 70% of global coffin sales in 2025. Their leadership is driven by their integrated service model, where coffin selection is bundled with funeral planning, logistics, and ceremonial services. Consumers often rely on funeral directors for guidance, making this channel highly influential in purchasing decisions. Additionally, long-standing relationships between manufacturers and funeral homes ensure consistent product supply and pricing structures.

However, online platforms are rapidly transforming the distribution landscape. E-commerce channels are gaining traction due to increased price transparency, wider product availability, and the ability to customize coffins digitally. This trend is particularly prominent in North America and Europe, where consumers are increasingly seeking cost-effective alternatives to traditional funeral home offerings. Wholesale suppliers and religious institutions also play a significant role, particularly in emerging markets where informal or community-based funeral arrangements are common. These channels provide cost-effective solutions and cater to local preferences, supporting market penetration in rural and semi-urban areas.

End-Use Insights

The funeral services industry remains the primary end-use sector, accounting for the majority of coffin demand globally. Within this, traditional burial services continue to drive the largest share due to cultural norms and established funeral practices. However, the industry is undergoing structural transformation with the increasing adoption of cremation services, particularly in urbanized and developed regions. The cremation segment is growing rapidly, especially in North America and Asia-Pacific, influencing the demand for simplified and cost-effective coffin solutions. This shift is driven by urban land constraints, lower overall funeral costs, and changing societal attitudes toward burial practices.

Green burial services are emerging as a niche yet high-growth end-use segment, supported by environmental awareness and regulatory initiatives promoting sustainable practices. This segment is expected to gain further traction as eco-conscious consumer behavior becomes more mainstream.Export-driven demand also plays a crucial role in the market, with countries such as China and Vietnam acting as major manufacturing hubs. These countries supply cost-effective coffins to global markets, benefiting from lower production costs and large-scale manufacturing capabilities. This global trade dynamic supports market expansion and price competitiveness.

Explore more data points, trends and opportunities Download Free Sample Report

Coffin Market Segmentations

By Product Type

- Wood Coffins

- Metal Coffins

- Biodegradable Coffins

- Composite & Fiberglass Coffins

By Application

- Traditional Burial

- Cremation-Compatible Coffins

- Green Burial

By Distribution Channel

- Funeral Homes

- Online Platforms

- Wholesale Suppliers

- Religious Institutions

By End-Use

- Funeral Service Providers

- Cremation Service Providers

- Green Burial Service Providers

Regional Insights

North America

North America accounts for approximately 35% of the global coffin market in 2025, making it the largest regional market. The United States dominates demand, supported by high funeral expenditure, well-established funeral service infrastructure, and strong consumer preference for premium and customized coffins. One of the key growth drivers in this region is the aging population, which is increasing mortality rates and sustaining long-term demand. Additionally, the presence of organized funeral service providers and high adoption of value-added services such as customization and pre-planned funerals further support market growth.

However, the increasing cremation rate, exceeding 60% in the U.S., is reshaping demand patterns, driving growth in lower-cost coffin segments and cremation-compatible products. The region is also witnessing rising demand for eco-friendly coffins, driven by environmental awareness and regulatory initiatives.

Europe

Europe holds around 28% of the global market share, with major demand coming from countries such as Germany, the UK, France, and Italy. The region’s growth is driven by a combination of aging demographics, strong regulatory frameworks, and increasing environmental consciousness. Northern European countries, in particular, are leading the shift toward biodegradable coffins, supported by government policies promoting sustainable burial practices.The market is also influenced by cultural diversity, with varying burial and cremation practices across countries. Western Europe is witnessing higher cremation rates, while Southern and Eastern Europe continue to maintain strong burial traditions, supporting demand for traditional coffins.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 6.5%. China and India are the largest markets, driven by population growth, urbanization, and increasing formalization of funeral services. Rising disposable incomes and changing lifestyles are encouraging consumers to adopt organized funeral services, thereby boosting demand for standardized coffin products. Japan remains a mature market with high cremation rates, yet demand persists for specialized and ceremonial coffins. Additionally, government initiatives supporting infrastructure development and urban planning are contributing to market expansion. The region’s growth is further supported by its role as a global manufacturing hub, particularly for export-oriented coffin production.

Latin America

Latin America accounts for approximately 10% of the global market, with Brazil and Mexico serving as key demand centers. The region’s growth is primarily driven by strong cultural adherence to traditional burial practices, which continue to sustain demand for coffins. Additionally, population growth and gradual improvements in healthcare infrastructure are contributing to increased funeral service utilization. Economic factors play a significant role in shaping demand, with a strong preference for mid-range and economy coffin segments. The expansion of funeral service providers and increasing urbanization are further supporting market growth across the region.

Middle East & Africa

The Middle East & Africa region holds around 12% of the global market share, with growth driven by high population growth rates, urbanization, and increasing formalization of funeral services. Countries such as Nigeria and South Africa are key markets, supported by rising awareness and adoption of organized funeral services. In many parts of Africa, traditional burial practices remain dominant, sustaining demand for standard coffins. Additionally, government investments in cemetery infrastructure and urban planning are supporting market development. The region also presents significant untapped potential, as increasing income levels and urbanization continue to drive the transition toward formal funeral services. The Middle East, while smaller in comparison, shows steady demand influenced by religious practices and population growth, with increasing adoption of standardized coffin solutions in certain urban areas.

Key Players in the Coffin Market

- Matthews International Corporation

- Hillenbrand Inc.

- Batesville Services LLC

- Aurora Casket Company

- Thacker Caskets

- Victoriaville & Co.

- Schuylkill Haven Casket Company

- R. C. Moore Company

- Olpin Group

- Eagle Casket Company

- Master Casket Company

- Astral Industries

- Casket Depot

- Coffin World

- Zhejiang Shengda Group