Clothing Buttons Market Size

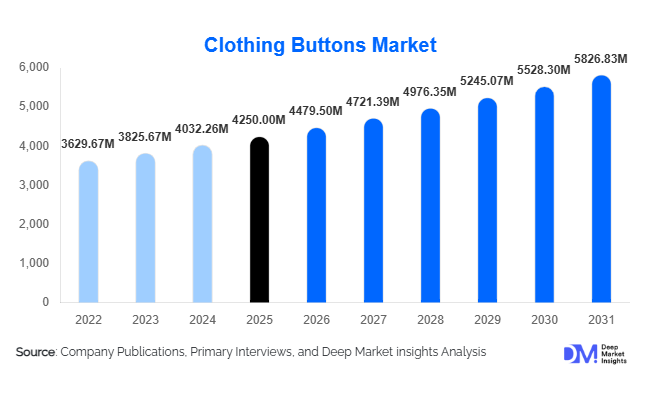

According to Deep Market Insights, the global clothing buttons market size was valued at USD 4,250 million in 2025 and is projected to grow from USD 4,479.50 million in 2026 to reach USD 5,826.83 million by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The market growth is primarily driven by the steady expansion of the global apparel industry, rising demand for fashion customization, and increasing adoption of sustainable materials in garment accessories.

Key Market Insights

- Plastic buttons dominate the market, accounting for over 40% share due to their cost-effectiveness, durability, and versatility across apparel segments.

- Asia-Pacific leads global production and demand, supported by strong textile manufacturing hubs in China, India, and Bangladesh.

- Sustainable and eco-friendly buttons are gaining traction, particularly in premium apparel and export-oriented manufacturing.

- Direct OEM supply channels dominate, enabling bulk procurement and cost efficiency for garment manufacturers.

- Customization and decorative buttons are witnessing rising demand, driven by fast fashion and direct-to-consumer apparel brands.

- Technological advancements in manufacturing, including automation and precision molding, are improving efficiency and scalability.

What are the latest trends in the clothing buttons market?

Shift Toward Sustainable Materials

The market is witnessing a strong shift toward eco-friendly materials such as wood, coconut shells, and recycled plastics. Apparel brands are increasingly prioritizing sustainability to meet regulatory requirements and consumer expectations. This has led to the adoption of biodegradable and low-impact production processes. Manufacturers are investing in certifications and environmentally responsible sourcing, which is becoming a key differentiator in premium segments. The demand for natural buttons is particularly strong in Europe and North America, where sustainability-driven purchasing decisions are more prominent.

Rising Demand for Customization and Design Innovation

Customization is becoming a major trend, driven by fast fashion and e-commerce apparel brands. Consumers are seeking unique clothing designs, prompting manufacturers to offer a wide range of button styles, finishes, and colors. Laser engraving, digital printing, and advanced molding technologies are enabling high levels of design precision. Decorative and fashion buttons are gaining popularity in premium and designer wear, while mid-range segments are also incorporating aesthetic elements to enhance product appeal.

What are the key drivers in the clothing buttons market?

Growth of Global Apparel Manufacturing

The expansion of the global apparel industry remains the primary driver of the clothing buttons market. Increasing clothing consumption, particularly in emerging economies, is boosting demand for garment accessories. Export-oriented manufacturing in countries such as India, Bangladesh, and Vietnam is further strengthening market growth, as these regions supply garments to developed markets.

Technological Advancements in Production

Automation and advanced manufacturing technologies are enhancing production efficiency and quality consistency. Injection molding, automated finishing, and high-speed assembly processes are reducing costs while enabling large-scale production. These advancements are particularly beneficial for mass-market segments, where cost efficiency and uniformity are critical.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fluctuations in the prices of plastics, metals, and natural materials pose a significant challenge for manufacturers. These variations impact production costs and profit margins, particularly for small and medium enterprises operating in competitive pricing environments.

Competition from Alternative Fastening Solutions

The increasing use of zippers, Velcro, and other fastening technologies in modern apparel is reducing reliance on traditional buttons in certain segments. Sportswear and performance clothing, in particular, are shifting toward alternative closures, which may limit market growth potential.

What are the key opportunities in the clothing buttons industry?

Expansion in Emerging Manufacturing Hubs

Emerging economies such as India, Vietnam, and Bangladesh present significant opportunities due to their rapidly growing textile industries. Government initiatives supporting domestic manufacturing and exports are encouraging investments in garment accessories, including buttons. Localization of production can help reduce costs and improve supply chain efficiency.

Integration of Smart and Functional Buttons

The development of smart buttons with embedded technologies such as RFID and NFC is opening new opportunities in premium and luxury apparel segments. These buttons can be used for authentication, tracking, and enhancing customer engagement. As digital integration becomes more prevalent in fashion, smart buttons are expected to gain traction.

Material Type Insights

Plastic buttons continue to dominate the global clothing buttons market, accounting for approximately 42% share in 2025. This leadership is primarily driven by their low production cost, scalability, and high versatility across mass-market apparel categories such as casual wear, uniforms, and children’s clothing. Plastic materials such as polyester and nylon allow for easy customization in terms of color, size, and finish, making them highly suitable for fast fashion cycles where speed and cost efficiency are critical. Additionally, advancements in recycled plastics are further strengthening this segment by aligning with sustainability trends.

Metal buttons represent the second-largest segment, widely used in denim, workwear, and outerwear applications due to their superior strength and durability. Their resistance to wear and tear makes them essential for heavy-duty garments. Meanwhile, natural material buttons, including wood, coconut shell, and horn, are witnessing increasing demand, particularly in eco-conscious and premium apparel segments. This growth is fueled by rising consumer awareness of sustainable fashion and stricter environmental regulations. Fabric-covered and ceramic buttons remain niche but are gaining traction in luxury and designer apparel, where aesthetics and exclusivity are key differentiators.

Product Type Insights

Sew-through buttons lead the product type segment with around 38% market share, driven by their widespread use in everyday garments such as shirts, trousers, and uniforms. Their simple design, cost-effectiveness, and ease of attachment make them the preferred choice for large-scale apparel manufacturing. This segment’s dominance is further supported by its compatibility with automated sewing processes, enhancing production efficiency.

Shank buttons are extensively used in formal wear and outerwear, where a raised attachment provides better drape and aesthetic appeal. Snap buttons are gaining traction, particularly in children’s wear and sportswear, due to their ease of use and quick fastening functionality. Decorative and fashion buttons are emerging as a high-growth segment, fueled by increasing demand for customization and design differentiation in premium and fast-fashion apparel. Innovations in textures, finishes, and embellishments are further accelerating growth in this category.

Application Insights

Casual wear remains the leading application segment, contributing nearly 35% of the global market in 2025. This dominance is driven by the high volume of everyday clothing consumption worldwide, particularly in emerging economies where population growth and urbanization are boosting apparel demand. The rapid expansion of fast fashion brands and e-commerce platforms is further reinforcing the demand for buttons in casual garments.

Denim and workwear applications also hold a significant share due to their reliance on durable fastening solutions such as metal buttons. These segments benefit from steady demand in both developed and developing markets. Outerwear and formal wear segments contribute moderately, with consistent demand for premium button designs. Meanwhile, luxury and designer apparel, although smaller in volume, generate higher margins due to the use of customized and high-quality buttons, reflecting evolving consumer preferences for exclusivity and aesthetics.

Distribution Channel Insights

Direct OEM supply dominates the distribution landscape, accounting for approximately 55% of the market share. This is primarily driven by the need for bulk procurement, cost efficiency, and quality consistency among large-scale garment manufacturers. OEM partnerships enable streamlined supply chains and faster production cycles, which are critical in the fast-paced fashion industry.

Wholesalers and distributors play a crucial role in catering to small and medium-sized apparel manufacturers, providing flexibility and a wide range of product options. Online B2B platforms are emerging as a fast-growing channel, offering competitive pricing, digital catalogs, and global accessibility. These platforms are particularly attractive to smaller buyers seeking convenience and variety. Retail craft and sewing stores serve niche markets, including individual consumers and small-scale designers, particularly in developed regions where DIY fashion and customization trends are gaining popularity.

End-Use Industry Insights

The apparel manufacturing industry remains the dominant end-use segment, accounting for nearly 70% of total demand in 2025. This dominance is directly linked to the scale of global textile production and the continuous growth of fast fashion and e-commerce-driven apparel sales. The increasing frequency of fashion cycles and rising consumer demand for new styles are significantly boosting button consumption.

Footwear and accessories are emerging as important secondary segments, particularly for decorative and functional buttons used in bags and fashion accessories. The home textiles segment provides stable demand, with applications in curtains, upholstery, and decorative items. Additionally, industrial and uniform manufacturing is contributing to steady demand, particularly in sectors such as hospitality, healthcare, and defense. Export-driven garment manufacturing, especially in Asia-Pacific region, remains a key growth driver, as global brands continue to source apparel from cost-competitive regions.

| By Material Type | By Product Type | By Application | By Distribution Channel | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global clothing buttons market with approximately 62% share in 2025, making it both the largest production and consumption hub. China leads the region with nearly 30% share, driven by its extensive textile manufacturing infrastructure, integrated supply chains, and strong export capabilities. India is the fastest-growing market, supported by government initiatives such as textile manufacturing incentives, rising domestic consumption, and increasing apparel exports. Bangladesh and Vietnam are also key contributors, benefiting from low labor costs and strong positioning in global garment supply chains.

The region’s growth is primarily driven by large-scale apparel production, export-oriented manufacturing, availability of raw materials, and favorable government policies. Increasing investments in textile infrastructure and the shift of global brands toward sourcing from Asia further strengthen regional demand.

North America

North America accounts for approximately 12% of the global market, with the United States being the primary contributor. The region is characterized by strong demand for premium, customized, and designer apparel, which drives the need for high-quality and decorative buttons. The presence of established fashion brands and a growing focus on sustainable clothing are key growth drivers. Additionally, the rise of direct-to-consumer (DTC) brands and e-commerce platforms is boosting demand for customized garment components. Technological advancements and automation in apparel manufacturing are also supporting market growth, although production volumes remain lower compared to Asia-Pacific.

Europe

Europe holds around 15% share of the global market, with countries such as Italy, Germany, and France leading demand. Italy stands out as a global hub for luxury fashion, driving demand for premium and designer buttons. Germany and France contribute significantly through their strong apparel and retail sectors. Regional growth is driven by high demand for sustainable and high-quality fashion products, strict environmental regulations, and increasing consumer preference for eco-friendly materials. The presence of renowned fashion houses and a strong focus on craftsmanship and design innovation further support the market in Europe.

Middle East & Africa

The Middle East & Africa region is emerging as a growth market, supported by expanding textile manufacturing in countries such as Turkey and Egypt. Turkey, in particular, serves as a major apparel export hub bridging Europe and Asia. Increasing urbanization, rising disposable incomes, and the expansion of retail infrastructure are key drivers of demand. In Africa, growing investments in textile manufacturing and government initiatives to boost local production are creating new opportunities. The region’s strategic location and improving trade connectivity are expected to further enhance its role in the global apparel supply chain.

Latin America

Latin America is led by Brazil and Mexico, where domestic apparel production and exports are driving demand for clothing buttons. The region accounts for a moderate share of the global market but is experiencing steady growth supported by expanding retail sectors and increasing consumer spending on apparel. Key growth drivers include the development of local textile industries, trade agreements facilitating exports, and rising adoption of fast fashion trends. Mexico benefits from its proximity to North America, serving as a key manufacturing base for exports, while Brazil’s large domestic market supports consistent demand.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Clothing Buttons Market

- YKK Corporation

- Coats Group plc

- Prym Group

- Scovill Fasteners

- SBS Zipper

- Union Knopf

- Bottonificio Lenzi

- Dill Button Group

- KAM Snap

- Zhejiang Weixing Industrial

- Hsin Yih Button

- Dongguan Chishing Plastic Products

- Tie Yong Industrial

- Suncor Buttons

- Fenghua Beida Button