Climbing Holds Market Size

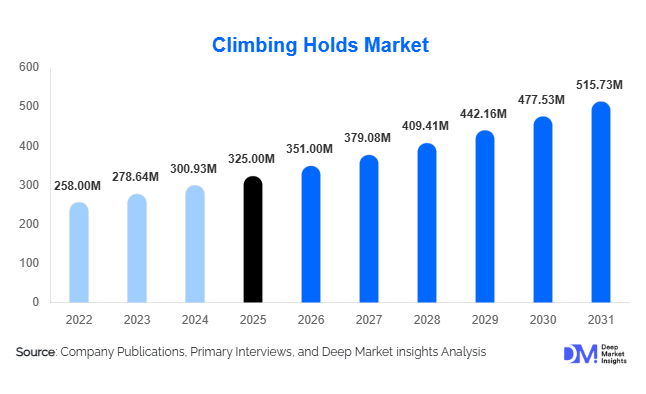

According to Deep Market Insights, the global climbing holds market size was valued at USD 325.0 million in 2025 and is projected to grow from USD 351.00 million in 2026 to reach USD 515.73 million by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). The climbing holds market growth is primarily driven by the rapid expansion of indoor climbing gyms, increasing participation in sport climbing as a mainstream fitness activity, and rising investments in recreational sports infrastructure across developed and emerging economies.

The market is evolving from a niche sports equipment category into a structured global fitness and entertainment industry. Indoor climbing gyms have become the primary demand center, accounting for a majority of recurring climbing hold purchases due to frequent route setting and periodic wall redesigns. The inclusion of sport climbing in global competitions has further strengthened visibility and participation, encouraging governments and private operators to invest in climbing infrastructure. Additionally, innovations in polyurethane materials, modular hold systems, and sustainable manufacturing practices are reshaping product design and procurement patterns. Asia-Pacific is emerging as the fastest-growing region, while North America and Europe continue to dominate in terms of installed climbing infrastructure and premium product demand.

Key Market Insights

- Indoor climbing gyms dominate global demand, driving frequent replacement cycles for climbing holds due to continuous route redesigning.

- Polyurethane leads the material segment due to durability, lightweight structure, and superior grip texture performance.

- North America holds the largest market share (~34% in 2025), supported by a mature fitness ecosystem and high gym penetration.

- Europe remains highly advanced in product innovation, particularly in competition-grade and premium climbing holds.

- Asia-Pacific is the fastest-growing region, driven by urban gym expansion and rising youth participation in climbing sports.

- Bouldering is the leading application segment due to lower infrastructure cost and high recreational adoption.

- Commercial climbing gyms account for the largest end-use share, driven by recurring demand for route diversification.

Climbing Holds Market Trends

Premiumization of Climbing Holds in Commercial Gyms

Commercial climbing gyms are increasingly investing in premium-grade climbing holds to enhance user experience and improve route-setting diversity. Gyms are shifting away from basic polyester holds toward advanced polyurethane and dual-texture designs that offer improved durability and tactile variation. This premiumization trend is also driven by rising customer expectations, as climbers seek more challenging and visually engaging routes. Frequent hold replacement cycles in gyms further support demand for higher-value products, strengthening manufacturer revenues and encouraging continuous product innovation.

Sustainability and Eco-Friendly Material Adoption

Sustainability has become a major trend in climbing hold manufacturing, with increasing adoption of recycled composites, low-emission resins, and eco-friendly polyurethane alternatives. Manufacturers are responding to environmental concerns and regulatory pressures by reducing volatile organic compounds (VOCs) and integrating circular production methods. Commercial gyms are also favoring suppliers with sustainable certifications to align with green building standards. This shift is particularly strong in Europe and North America, where environmental compliance influences procurement decisions and brand positioning.

Climbing Holds Market Drivers

Rapid Expansion of Indoor Climbing Infrastructure

The global rise in indoor climbing gyms is the most significant growth driver for the climbing holds market. Urbanization, limited access to natural climbing locations, and growing demand for experiential fitness are fueling gym construction worldwide. Each new facility requires large-scale installation of climbing holds and continuous replacement cycles to maintain route freshness. This creates a recurring revenue model for manufacturers and significantly increases overall market demand.

Olympic Recognition and Rising Sport Climbing Popularity

The inclusion of sport climbing in the Olympic Games has dramatically increased global visibility and participation. This has led to higher investments in training centers, competition-grade facilities, and youth development programs. Governments and sports federations are actively funding climbing infrastructure, boosting demand for certified and competition-standard climbing holds. The growing professional climbing ecosystem is also expanding the premium product segment.

Technological Advancements in Product Design

Innovation in material science and product engineering is enhancing market growth. Polyurethane holds, modular macro systems, and dual-texture surfaces are improving durability, grip performance, and route flexibility. Manufacturers are also developing ergonomic designs that reduce injury risk and improve climbing experience. These advancements are increasing product lifecycle value and encouraging gyms to upgrade their installations more frequently.

Climbing Holds Market Restraints

High Installation and Maintenance Costs

Climbing infrastructure requires significant capital investment, including wall construction, safety systems, and frequent hold replacements. Premium climbing holds, particularly competition-grade variants, can be expensive, limiting adoption in smaller gyms and price-sensitive markets. These high costs can restrict market penetration in developing regions and slow down expansion among low-budget operators.

Raw Material Price Volatility and Supply Chain Constraints

The market is heavily dependent on petrochemical-based resins used in polyurethane and polyester production. Fluctuating raw material prices impact manufacturer margins and create pricing instability. Additionally, global supply chain disruptions and regional manufacturing concentration can lead to delays in production and distribution, affecting timely delivery to commercial clients.

Climbing Holds Market Opportunities

Expansion in Emerging Markets and Urban Fitness Centers

Rapid urbanization in Asia-Pacific, Latin America, and the Middle East is creating strong opportunities for climbing gym expansion. Rising disposable income and increasing interest in experiential fitness are driving demand for indoor climbing facilities in cities such as Mumbai, Shanghai, São Paulo, and Dubai. This is expected to significantly increase demand for cost-effective and mid-range climbing holds tailored for new market entrants.

Integration with Smart Climbing and Digital Training Systems

The emergence of interactive climbing systems, including LED-guided routes and app-connected training platforms, presents a major growth opportunity. Smart climbing walls require compatible modular holds that can integrate with digital systems. Manufacturers investing in tech-enabled climbing solutions can differentiate themselves and capture premium market segments in entertainment centers and high-end gyms.

Growth in Institutional and Youth Training Programs

Schools, universities, and sports academies are increasingly adopting climbing walls as part of physical education programs. Government initiatives promoting youth fitness are further accelerating adoption. This creates demand for beginner-friendly, safe, and durable climbing holds designed specifically for training environments, expanding the institutional customer base significantly.

Product Type Insights

Jug holds remain the dominant product type in the global climbing holds market, accounting for approximately 22% of total market share in 2025. Their leadership is primarily driven by their essential role in beginner-friendly climbing routes, youth training programs, and commercial gym onboarding sections. As the entry-level interface of climbing walls, jug holds are heavily utilized in gyms to improve accessibility, reduce injury risk, and encourage participation among first-time climbers. The sustained growth of indoor climbing gyms, especially in urban areas, continues to reinforce demand for this segment.

Crimp and pinch holds collectively represent a significant share of intermediate and advanced climbing routes, benefiting from the rising popularity of technical training and competition-oriented climbing. Sloper and volume holds are witnessing strong adoption in modern climbing gyms due to their ability to create dynamic, three-dimensional route-setting experiences that enhance difficulty variation and user engagement. However, the fastest-growing segment is macro and modular holds, driven by their capacity to transform climbing wall geometry and enable frequent route redesigns without full wall reconstruction. This growth is supported by commercial gym operators’ increasing focus on customer retention through constantly evolving climbing experiences and premium route diversity.

Application Insights

Bouldering continues to dominate the global climbing holds market with an estimated 38% share in 2025, driven by its minimal infrastructure requirements, high user participation rates, and rapid expansion of dedicated bouldering gyms in urban centers. Its leadership is further reinforced by its accessibility to beginners and its strong alignment with social, recreational fitness trends. The segment benefits significantly from frequent route resetting requirements, which directly increases climbing hold consumption.

Lead climbing remains a key segment in professional training facilities and advanced gyms, supported by increasing participation in sport climbing competitions. Speed climbing is gaining traction due to its inclusion in international sporting events and growing competitive interest among younger athletes. Training and fitness applications are expanding rapidly as traditional gyms integrate climbing-based functional workouts to diversify offerings. Recreational and youth climbing is also experiencing strong institutional support, particularly through school programs and community sports initiatives, which is broadening the long-term user base and supporting sustained demand growth.

Distribution Channel Insights

Direct sales dominate the distribution structure with approximately 41% market share, as commercial climbing gyms and institutional buyers prefer direct procurement for customized hold sets, bulk pricing advantages, and long-term supplier relationships. This channel is particularly strong among large gym chains that require frequent route updates and tailored climbing wall configurations.

Specialty sports retailers and regional distributors play a crucial role in market expansion, especially in emerging economies where direct manufacturer access is limited. These intermediaries help bridge supply gaps and provide localized product availability. Online distribution channels are rapidly expanding, driven by the rise of home climbing setups, personal training walls, and small-scale fitness installations. OEM partnerships with climbing wall manufacturers are also becoming increasingly important, enabling integrated supply chains and turnkey climbing facility solutions that combine wall systems and holds into unified procurement models.

End-Use Insights

Commercial climbing gyms represent the largest end-use segment, accounting for nearly 46% of global demand in 2025. This dominance is driven by continuous route redesign requirements, high user turnover, and the need for frequent hold replacement to maintain engagement. The rapid global expansion of indoor climbing facilities has further strengthened this segment’s leadership position.

Educational institutions are emerging as one of the fastest-growing end-use categories, supported by increasing adoption of climbing walls in physical education programs and youth development initiatives. Fitness centers and multi-sport recreational complexes are also integrating climbing installations to diversify workout offerings and attract younger demographics. Additionally, defense and tactical training facilities are increasingly adopting climbing infrastructure for strength, endurance, and agility training programs, particularly in North America and Europe. This diversification of end-use applications is significantly expanding the total addressable market for climbing holds globally.

| By Product Type | By Material Type | By Application | By End-Use | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America leads the global climbing holds market with approximately 34% market share in 2025. The United States is the primary growth engine, supported by a highly developed indoor climbing gym ecosystem, strong participation in sport climbing, and widespread integration of climbing into mainstream fitness culture. Canada is also witnessing steady growth, particularly in urban centers such as Toronto, Vancouver, and Montreal. strong gym penetration, high disposable income, Olympic-level sport participation, and continuous innovation in commercial climbing facilities. Additionally, increasing consumer preference for experiential fitness and social workout environments is significantly boosting demand for climbing holds across both premium and mid-range segments.

Europe

Europe accounts for nearly 31% of the global market and remains one of the most mature and innovation-driven regions. Germany, France, the United Kingdom, Italy, and Spain are key contributors, with strong infrastructure support and a deeply established climbing culture. strong sustainability regulations driving eco-friendly product adoption, high penetration of advanced climbing gyms, and strong demand for competition-grade and premium holds. Europe also benefits from a well-established outdoor climbing tradition, which translates into high indoor training adoption and frequent equipment upgrades.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, projected to expand at over 10% CAGR. China leads regional expansion, followed by Japan, South Korea, India, and Australia. Rapid urbanization and rising disposable incomes are significantly reshaping the recreational sports landscape. expanding urban fitness infrastructure, increasing youth participation in adventure sports, government investment in sports facilities, and rising popularity of Western-style indoor climbing gyms. Additionally, the growing middle-class population and social media influence are accelerating awareness and adoption of climbing as a mainstream fitness activity.

Latin America

Brazil and Mexico are the primary contributors in Latin America, with gradual but steady growth in climbing infrastructure development. Although still an emerging market, increasing interest in adventure sports and fitness-based recreational activities is supporting expansion. rising youth participation in fitness activities, increasing investment in urban recreational centers, and growing popularity of adventure tourism. The region is also benefiting from the gradual entry of international gym chains and climbing facility operators targeting mid-income urban populations.

Middle East & Africa

The UAE and Saudi Arabia are leading growth in this region, driven by large-scale investments in tourism, entertainment, and sports infrastructure under national diversification programs. South Africa also represents a key emerging market within the African continent. government-led sports infrastructure development initiatives, increasing demand for premium entertainment experiences, and rapid expansion of indoor leisure facilities in urban centers. Additionally, rising tourism investments and luxury lifestyle developments are accelerating adoption of high-end climbing gyms and recreational climbing facilities.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Climbing Holds Market

- EP Climbing

- Entre-Prises

- Kilter Grips

- So iLL

- Trango

- Atomik Climbing Holds

- eGrips

- Euroholds

- Blocz