Climbing Helmet Market Size

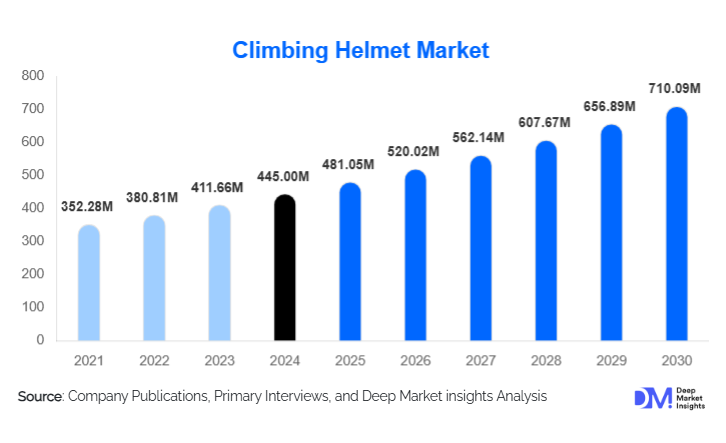

According to Deep Market Insights, the global climbing helmet market size was valued at USD 445 million in 2025 and is projected to grow from USD 481.05 million in 2026 to reach approximately USD 710.09 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The climbing helmet market growth is primarily driven by the rapid expansion of indoor climbing gyms, rising participation in recreational and competitive climbing, increasing safety awareness, and continuous product innovation focused on lightweight and high-impact protection.

Key Market Insights

- Sport and indoor climbing applications dominate demand, supported by the global rise of urban climbing gyms and Olympic-level recognition of climbing.

- Foam and hybrid helmet constructions are gaining preference due to superior comfort, reduced weight, and enhanced ventilation.

- Europe remains the largest regional market, supported by strong Alpine traditions and stringent safety compliance.

- Asia-Pacific is the fastest-growing region, driven by gym expansion, youth participation, and rising disposable incomes.

- Mid-range helmets (USD 60–120) account for the largest share, balancing safety certifications with affordability.

- E-commerce and D2C channels are rapidly expanding, especially among younger, tech-savvy climbers.

Climbing Helmet Market Trends

Lightweight and Multi-Impact Helmet Designs

Manufacturers are increasingly focused on developing lightweight helmets that provide multi-impact protection without compromising comfort. Advanced foam materials such as EPS and EPP, combined with hybrid shell constructions, are enabling helmets to absorb repeated impacts while remaining compact and breathable. This trend is particularly important for sport climbers and mountaineers who prioritize long-duration wear comfort. Reduced helmet weight has also helped improve adoption among experienced climbers who were previously resistant to helmet use.

Sustainability and Eco-Friendly Materials

Sustainability is emerging as a differentiating trend in the climbing helmet market. Leading brands are introducing recyclable plastics, bio-based foams, and low-emission manufacturing processes. Environmentally conscious consumers, particularly in Europe and North America, increasingly favor brands that align with responsible outdoor ethics. Sustainable packaging, extended product life cycles, and repair-friendly designs are also gaining traction as manufacturers align product strategies with circular economy principles.

Climbing Helmet Market Drivers

Growth of Indoor Climbing Gyms

The global proliferation of indoor climbing gyms is one of the strongest growth drivers for climbing helmets. Gyms frequently mandate helmet use for beginners, youth programs, and training courses, creating consistent institutional demand. Urbanization and increasing interest in fitness-oriented adventure sports have significantly expanded the addressable consumer base beyond traditional outdoor climbers.

Rising Safety Awareness and Certification Standards

Increasing awareness of head injury risks and stricter enforcement of international safety standards have accelerated helmet adoption. Certifications such as CE and UIAA are now considered essential benchmarks, encouraging climbers to upgrade or replace older helmets. Professional guides, climbing federations, and insurance providers further reinforce helmet usage, supporting long-term market growth.

Climbing Helmet Market Restraints

Price Sensitivity in Emerging Markets

Premium climbing helmets can be relatively expensive, limiting adoption among price-sensitive consumers in developing regions. Entry-level users often delay purchases or opt for uncertified alternatives, slowing penetration in emerging markets.

Cultural Resistance Among Experienced Climbers

In certain climbing disciplines, especially sport climbing, some experienced climbers continue to perceive helmets as unnecessary. Overcoming these ingrained perceptions requires ongoing education, regulation by gyms, and advocacy from professional athletes.

Climbing Helmet Market Opportunities

Institutional and Bulk Sales to Gyms and Training Centers

The expansion of climbing gyms, adventure training institutes, and youth sports programs presents strong opportunities for bulk helmet sales. Manufacturers offering durable, adjustable, and cost-efficient helmet models can secure long-term supply agreements and recurring revenue.

Technological Integration and Smart Safety Features

Opportunities are emerging for integrating smart features such as impact indicators, RFID tracking for gym inventory, and sensor-based damage alerts. These innovations can support premium pricing and enhance differentiation, particularly for professional and institutional users.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 445 Million |

| Market Size in 2026 | USD 481.05 Million |

| Market Size in 2031 | USD 710.09 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Foam (in-mold) helmets lead the market, accounting for approximately 48% of global demand in 2025, due to their lightweight construction and comfort. Hybrid helmets are gaining share among mountaineers and alpine climbers who require enhanced durability, while traditional hardshell helmets remain relevant in institutional and training applications where durability and cost-efficiency are prioritized.

Application Insights

Sport climbing, including indoor and outdoor applications, represents the largest application segment with around 42% market share. Mountaineering and alpine climbing follow, driven by strict safety requirements in high-altitude environments. Ice climbing and via ferrata segments, while smaller, are growing steadily due to rising adventure tourism participation.

Distribution Channel Insights

Specialty outdoor and sports retail stores dominate distribution, accounting for nearly 46% of sales, as consumers prefer professional fitting and expert advice. E-commerce and D2C platforms are the fastest-growing channels, benefiting from wider product availability, competitive pricing, and direct brand engagement.

End-User Insights

Recreational climbers constitute the largest end-user segment, representing approximately 55% of total demand. Professional climbers and mountaineers drive premium helmet sales, while climbing gyms and adventure operators generate consistent institutional demand through bulk procurement and replacement cycles.

Explore more data points, trends and opportunities Download Free Sample Report

Climbing Helmet Market Segmentations

By Helmet Construction Type

- Hardshell Helmets

- Hybrid Helmets

- Foam (In-Mold) Helmets

By Application

- Sport Climbing (Indoor & Outdoor)

- Trad & Multi-Pitch Climbing

- Mountaineering & Alpine Climbing

- Ice Climbing

- Via Ferrata & Recreational Scrambling

By End User

- Recreational Climbers

- Professional Climbers & Mountaineers

- Climbing Gyms & Training Institutes

- Adventure Tourism Operators & Guides

By Distribution Channel

- Specialty Outdoor & Sports Retail Stores

- E-commerce / Direct-to-Consumer (D2C)

- Institutional & Bulk Sales

By Price Category

- Entry-Level (Below USD 60)

- Mid-Range (USD 60–120)

- Premium (Above USD 120)

Regional Insights

Europe

Europe leads the global climbing helmet market with an estimated 32% share in 2025. Germany, France, Italy, Switzerland, and Austria are key contributors, supported by strong Alpine climbing cultures, high safety compliance, and premium product adoption.

North America

North America accounts for approximately 28% of global demand, led by the United States. The region benefits from widespread gym networks, strong adventure sports participation, and high consumer spending on certified safety equipment.

Asia-Pacific

Asia-Pacific represents about 23% of the market and is the fastest-growing region, expanding at over 9.5% CAGR. China, Japan, South Korea, and India are driving growth through gym expansion, youth participation, and government-supported sports infrastructure.

Latin America

Latin America holds roughly 9% market share, led by Chile and Argentina. Growth is supported by adventure tourism and the increasing adoption of climbing as a recreational sport.

Middle East & Africa

The Middle East & Africa account for around 8% of global demand, with growth driven by tourism initiatives in the UAE and Saudi Arabia and climbing activity in the alpine regions of Africa.