Clean Room Wipes Market Size

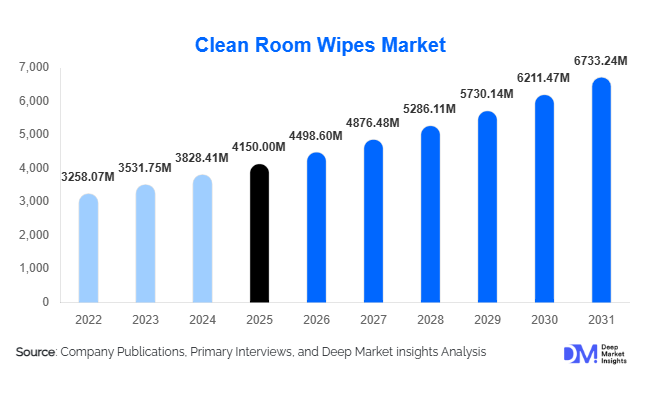

According to Deep Market Insights, the global clean room wipes market size was valued at USD 4,150 million in 2025 and is projected to grow from USD 4,498.60 million in 2026 to reach USD 6,733.24 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). The market growth is primarily driven by increasing contamination control requirements across semiconductor manufacturing, pharmaceutical production, and biotechnology research. Rising regulatory compliance standards, expansion of cleanroom infrastructure globally, and growing adoption of advanced materials such as microfiber and polyester blends are further accelerating demand for high-performance cleanroom wipes.

Key Market Insights

- Semiconductor and electronics manufacturing dominate demand, accounting for over 35% of total consumption due to stringent contamination control requirements.

- Pre-saturated wipes are gaining traction, driven by pharmaceutical and biotech applications requiring consistent disinfection performance.

- Asia-Pacific leads the global market, supported by strong electronics manufacturing hubs in China, Taiwan, South Korea, and Japan.

- The pharmaceutical and biotechnology sectors are the fastest-growing, with demand rising due to biologics and vaccine production.

- Sustainability trends are influencing product innovation, with increasing adoption of biodegradable and low-waste wipe materials.

- Direct B2B procurement dominates distribution, as large-scale industries rely on long-term supply contracts and customized solutions.

What are the latest trends in the clean room wipes market?

Shift Toward Pre-Saturated and Application-Specific Wipes

Manufacturers are increasingly developing pre-saturated cleanroom wipes tailored for specific applications such as disinfecting, solvent cleaning, and residue removal. These wipes ensure uniform application of chemicals and reduce variability in cleaning processes, making them highly suitable for pharmaceutical and biotech cleanrooms. Demand is particularly strong in aseptic environments where consistency and compliance with GMP standards are critical. Additionally, wipes pre-treated with isopropyl alcohol (IPA) and other validated disinfectants are becoming standard in sterile manufacturing environments, enhancing operational efficiency and reducing contamination risks.

Growing Adoption of Sustainable and Low-Particle Materials

Environmental sustainability is becoming a key focus area in the cleanroom consumables industry. Manufacturers are investing in biodegradable materials, recyclable packaging, and reduced-lint fabrics to address regulatory and environmental concerns. Polyester and microfiber wipes are being engineered to deliver high absorbency while minimizing particle generation. This trend is particularly strong in Europe, where environmental regulations are driving innovation in eco-friendly cleanroom products. Companies are also focusing on lifecycle assessments and carbon footprint reduction to align with the ESG goals of industrial buyers.

What are the key drivers in the clean room wipes market?

Expansion of Semiconductor Manufacturing

The rapid growth of semiconductor fabrication facilities globally is a major driver for cleanroom wipes demand. Advanced chip manufacturing requires ultra-clean environments with minimal particle contamination, leading to high consumption of low-lint wipes. Government initiatives to localize chip production in regions such as North America, Europe, and Asia are further boosting demand for cleanroom consumables.

Growth in Pharmaceutical and Biotechnology Production

The increasing production of biologics, vaccines, and advanced therapies is driving demand for sterile cleanroom environments. Cleanroom wipes play a critical role in maintaining hygiene and compliance in pharmaceutical manufacturing. The rise of contract manufacturing organizations (CMOs) and increased R&D activities are also contributing to sustained demand growth.

What are the restraints for the global market?

High Cost of Advanced Wipes

Premium cleanroom wipes, especially sterile and microfiber variants, are relatively expensive compared to standard wipes. This cost factor can limit adoption among smaller manufacturers and in cost-sensitive regions, impacting overall market penetration.

Environmental Concerns Related to Disposable Products

The widespread use of disposable wipes raises concerns regarding waste generation and environmental impact. Increasing regulatory scrutiny on single-use materials is pushing manufacturers to invest in sustainable alternatives, which may increase production costs and impact pricing strategies.

What are the key opportunities in the clean room wipes industry?

Semiconductor Industry Expansion Initiatives

Global investments in semiconductor manufacturing present a significant opportunity for cleanroom wipe manufacturers. Government-backed initiatives such as domestic chip production programs are driving demand for ultra-clean consumables. Companies that develop specialized wipes for high-criticality cleanrooms (ISO Class 3–5) can capture high-value segments.

Rising Demand for Sterile and Pre-Saturated Wipes

The pharmaceutical and biotechnology sectors are increasingly adopting sterile, pre-saturated wipes to meet stringent regulatory standards. This segment offers higher margins and recurring demand, making it an attractive opportunity for both existing players and new entrants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4150 Million |

| Market Size in 2026 | USD 4498.60 Million |

| Market Size in 2031 | USD 6733.24 Million |

| CAGR | 8.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Dry cleanroom wipes continue to dominate the market, accounting for approximately 62% of the total share in 2025, primarily due to their cost-effectiveness, versatility, and compatibility with a wide range of solvents and cleaning agents. These wipes are extensively used across semiconductor, electronics, and industrial manufacturing environments where users require flexibility in applying customized cleaning solutions. The leading driver for this segment is the ability to adapt to multiple cleaning protocols, making them a preferred choice in high-volume operations. Additionally, their lower cost per unit compared to pre-saturated variants supports bulk procurement by large-scale manufacturers. However, pre-saturated (wet) wipes are gaining strong momentum, particularly in pharmaceutical and biotechnology applications where consistent chemical dosing, reduced handling errors, and compliance with GMP standards are critical. The growing adoption of application-specific wipes, such as IPA-saturated or disinfectant-treated wipes, is expected to accelerate the growth of this segment over the forecast period, especially in sterile environments.

Material Type Insights

Polyester wipes lead the material segment with approximately 38% market share, driven by their superior performance characteristics, including low particle generation, high tensile strength, and excellent chemical resistance. The primary growth driver for polyester wipes is their suitability for high-criticality cleanroom environments such as semiconductor fabrication plants (fabs), where even minimal contamination can lead to significant yield losses. Polypropylene and poly-cellulose blends are widely used in medium- and low-criticality environments due to their cost advantages and adequate absorbency. These materials are commonly adopted in general industrial cleaning and less sensitive applications. Meanwhile, microfiber wipes are emerging as a high-performance segment, offering superior absorption, fine particle capture, and enhanced cleaning efficiency. Their increasing adoption in advanced semiconductor manufacturing and precision industries is driven by the need for ultra-clean surfaces and improved process yields.

Sterility Insights

Non-sterile cleanroom wipes dominate the market with approximately 68% share, largely due to their extensive usage in electronics, automotive, and industrial manufacturing sectors where sterility is not a mandatory requirement. The key driver for this segment is cost efficiency combined with high-volume usage in non-aseptic environments. However, sterile wipes are witnessing faster growth, particularly in the pharmaceutical and biotechnology industries. The rising production of biologics, vaccines, and cell-based therapies has increased the need for sterile environments, thereby driving demand for gamma-irradiated and validated sterile wipes. Regulatory compliance with GMP and aseptic processing standards is a major factor accelerating this segment’s growth, making sterile wipes a high-value, high-margin category.

End-Use Industry Insights

The semiconductor and electronics industry remains the largest end-user, accounting for over 35% of total demand. The primary driver for this dominance is the increasing complexity of chip manufacturing processes, which require ultra-clean environments to minimize defects and improve yield rates. The pharmaceutical and biotechnology sectors are the fastest-growing end-use industries, supported by rising global drug production, increased R&D investments, and stringent regulatory requirements for contamination control. Medical device manufacturing is also emerging as a significant segment, driven by the growing demand for precision-engineered devices and strict hygiene standards. Additionally, aerospace and defense applications are contributing to demand growth due to the need for contamination-free assembly environments.

Distribution Channel Insights

Direct B2B sales dominate the market with approximately 60% share, driven by long-term procurement contracts, bulk purchasing requirements, and the need for customized product specifications. Large industrial buyers, particularly in the semiconductor and pharmaceutical sectors, prefer direct engagement with manufacturers to ensure consistent quality and supply reliability. The key driver for this segment is the integration of cleanroom consumables into operational workflows, requiring dependable and scalable supply chains. Distributors and industrial suppliers play a crucial role in reaching small and medium-sized enterprises, offering a wide range of products and logistical support. Meanwhile, e-commerce platforms are gaining traction for low-volume and on-demand purchases, particularly among smaller laboratories and research facilities.

Explore more data points, trends and opportunities Download Free Sample Report

Clean Room Wipes Market Segmentations

By Product Type

- Dry Cleanroom Wipes

- Pre-Saturated (Wet) Cleanroom Wipes

By Material Type

- Polyester Wipes

- Polypropylene Wipes

- Poly-Cellulose Blends

- 100% Cellulose Wipes

- Microfiber Wipes

By Sterility

- Sterile Cleanroom Wipes

- Non-Sterile Cleanroom Wipes

By End-Use Industry

- Semiconductor & Electronics Manufacturing

- Pharmaceutical & Biotechnology

- Medical Device Manufacturing

- Aerospace & Defense

- Food & Beverage Processing

- Automotive Manufacturing

By Distribution Channel

- Direct B2B Sales

- Distributors & Industrial Suppliers

- E-commerce Platforms

Regional Insights

Asia-Pacific

Asia-Pacific leads the clean room wipes market with approximately 42% share in 2025, driven by strong industrial growth and the concentration of global semiconductor manufacturing hubs in countries such as China, Taiwan, South Korea, and Japan. The primary growth driver in this region is the rapid expansion of semiconductor fabrication facilities and electronics manufacturing, particularly in Taiwan and South Korea, which host some of the world’s most advanced chip production plants. China’s dominance is supported by government initiatives aimed at boosting domestic manufacturing capabilities and reducing reliance on imports. Additionally, the region’s growing pharmaceutical production capacity, especially in India and China, is further fueling demand for cleanroom consumables. Lower manufacturing costs and increasing foreign direct investments (FDI) in high-tech industries also contribute significantly to regional growth.

North America

North America holds around 27% market share, with the United States being the primary contributor. The region’s growth is driven by strong investments in semiconductor manufacturing, supported by government initiatives to localize chip production and reduce supply chain dependencies. Additionally, North America has a highly developed pharmaceutical and biotechnology sector, which requires stringent contamination control and drives demand for high-quality cleanroom wipes. The presence of advanced research facilities, high regulatory standards (such as FDA and GMP compliance), and continuous innovation in healthcare and life sciences are key factors supporting market growth in this region.

Europe

Europe accounts for approximately 22% of the market, led by Germany, France, and the UK. The region’s growth is primarily driven by stringent environmental and regulatory standards, which encourage the adoption of high-performance and sustainable cleanroom wipes. Germany’s strong industrial base, particularly in automotive and precision manufacturing, contributes significantly to demand. Additionally, Europe’s well-established pharmaceutical industry and increasing focus on biologics and advanced therapies are boosting the need for sterile cleanroom consumables. The push toward sustainability and circular economy practices is also encouraging innovation in eco-friendly wipe materials.

Latin America

Latin America is experiencing gradual growth, with Brazil and Mexico leading demand. The key driver in this region is the expansion of healthcare infrastructure and the increasing adoption of cleanroom practices in pharmaceutical and medical device manufacturing. Industrial growth and foreign investments in manufacturing sectors are also supporting market development. Although the region currently represents a smaller share of the global market, improving regulatory frameworks and rising awareness of contamination control are expected to drive steady growth over the forecast period.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth, driven by increasing investments in healthcare infrastructure, pharmaceutical manufacturing, and industrial diversification. Countries such as the UAE and Saudi Arabia are emerging as key markets due to government initiatives aimed at reducing dependency on imports and developing local manufacturing capabilities. The growth driver in this region is largely linked to expanding healthcare facilities, rising demand for high-quality medical products, and the establishment of cleanroom environments in emerging industries. Additionally, strategic investments in biotechnology and life sciences are expected to create new opportunities for cleanroom wipe manufacturers.