Cinema Screens Market Size

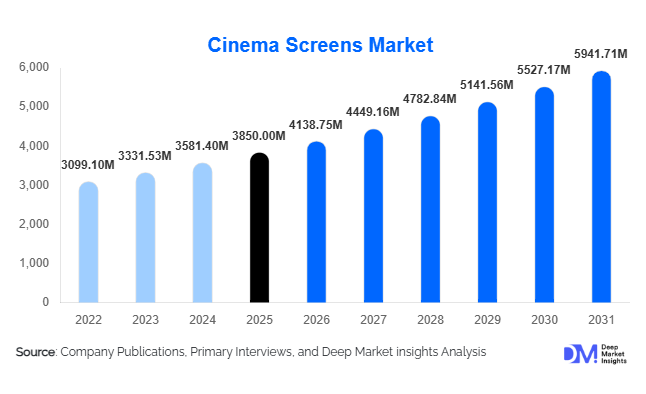

According to Deep Market Insights, the global cinema screens market size was valued at USD 3,850 million in 2025 and is projected to grow from USD 4,138.75 million in 2026 to reach USD 5,941.71 million by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The cinema screens market growth is primarily driven by the expansion of multiplex infrastructure, increasing adoption of premium large-format screens, and advancements in projection and display technologies such as laser and direct-view LED systems. The resurgence of theatrical releases and the growing emphasis on immersive viewing experiences are further accelerating investments in high-performance cinema screens globally.

Key Market Insights

- Premium large-format and immersive cinema experiences are driving upgrades, with IMAX and LED screens gaining significant traction globally.

- Asia-Pacific dominates the global market, led by rapid cinema infrastructure expansion in China and India.

- Multiplex chains account for the largest share of demand, driven by continuous screen additions and modernization initiatives.

- Direct-view LED cinema screens are emerging as a disruptive technology, offering superior brightness and operational efficiency.

- Outdoor and event-based cinema applications are expanding, creating new revenue streams for portable and inflatable screens.

- Technological advancements in projection systems, including laser and HDR compatibility, are reshaping screen material demand.

What are the latest trends in the cinema screens market?

Adoption of Direct-View LED Cinema Screens

The cinema industry is witnessing a gradual shift from traditional projection-based systems to direct-view LED screens. These screens deliver superior brightness, contrast, and colour accuracy while eliminating the need for projection equipment. Cinema operators are increasingly adopting LED screens for premium auditoriums, as they offer lower maintenance costs and enhanced durability over time. While initial investment costs remain high, declining prices and technological improvements are expected to accelerate adoption. LED screens are also enabling new design possibilities, including flexible screen sizes and curved displays, enhancing the overall cinematic experience.

Growth of Premium Large Format (PLF) Screens

Premium large-format screens, including IMAX and Dolby Cinema, are gaining significant popularity as audiences seek immersive experiences. These screens offer enhanced visuals, superior sound integration, and larger viewing areas, making them a preferred choice for blockbuster releases. Cinema chains are investing heavily in PLF installations to differentiate their offerings and increase ticket prices. This trend is particularly strong in developed markets such as North America and Europe, where consumers are willing to pay a premium for enhanced viewing experiences.

What are the key drivers in the cinema screens market?

Expansion of Multiplex Infrastructure

The rapid growth of multiplex chains, especially in emerging economies, is a major driver of the cinema screens market. Urbanisation, rising disposable incomes, and increasing demand for entertainment are encouraging investments in new cinema complexes. Countries such as India, China, and Saudi Arabia are witnessing a surge in multiplex construction, directly boosting demand for cinema screens. Additionally, government support for entertainment infrastructure is further accelerating this growth.

Technological Advancements in Projection Systems

The transition from traditional projection systems to laser-based projection has significantly increased demand for advanced cinema screens. Laser projection offers higher brightness, improved colour accuracy, and longer operational life, requiring compatible screen materials. This has led to increased replacement demand in mature markets, where cinema operators are upgrading existing screens to support new technologies.

What are the restraints for the global market?

High Initial Investment Costs

Advanced cinema screens, particularly LED and premium large-format installations, involve high upfront costs. Smaller and independent theatre operators often face financial constraints, limiting adoption. High installation and maintenance costs further add to the financial burden, making it challenging for operators to upgrade existing infrastructure.

Competition from OTT Platforms

The growing popularity of OTT platforms and home entertainment systems poses a challenge to the cinema screens market. Consumers increasingly prefer on-demand content, reducing footfall in theatres. This trend can delay investments in new cinema infrastructure and impact overall screen demand, particularly in developed markets.

What are the key opportunities in the cinema screens industry?

Expansion in Emerging Markets

Emerging economies in the Asia-Pacific, the Middle East, and Africa present significant growth opportunities for the cinema screens market. Rapid urbanisation, increasing disposable incomes, and government initiatives to boost entertainment infrastructure are driving demand for new cinema screens. Market participants can capitalise on this growth by offering cost-effective and scalable solutions tailored to local requirements.

Growth of Alternative Cinema Applications

The rise of outdoor cinema, live event screenings, and esports broadcasting is creating new opportunities for cinema screen manufacturers. Portable and inflatable screens are gaining popularity in event-based applications, providing flexibility and scalability. These alternative use cases are expanding the market beyond traditional cinema settings and opening new revenue streams.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3850 Million |

| Market Size in 2026 | USD 4138.75 Million |

| Market Size in 2031 | USD 5941.71 Million |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fixed frame screens continue to dominate the cinema screens market, accounting for approximately 42% of total demand in 2025, primarily due to their widespread adoption across commercial multiplex chains. The leading position of this segment is driven by its structural stability, consistent surface tension, and superior image uniformity, which are critical for delivering high-quality projection in large auditoriums. Multiplex operators prefer fixed frame screens as they support high-lumen laser projection systems and require minimal maintenance over long operating cycles. Additionally, the global trend toward multiplex expansion, especially in Asia-Pacific and the Middle East, has further strengthened demand for fixed installations.

Motorised and portable screens serve niche but growing applications such as event-based screenings, corporate presentations, and temporary cinema setups. These segments are benefiting from the rise of outdoor and experiential entertainment formats. Meanwhile, curved and premium large-format (PLF) screens are gaining traction in high-end cinemas, supported by increasing consumer willingness to pay for immersive experiences. The rapid emergence of direct-view LED cinema screens is also reshaping the product landscape, particularly in premium segments, as operators seek differentiation through superior brightness, contrast, and operational efficiency.

Application Insights

2D projection remains the dominant application segment, accounting for approximately 55% of the global market share in 2025. Its leadership is driven by its universal compatibility with all film formats, lower operational costs, and widespread content availability. The majority of global film production continues to be optimized for 2D viewing, ensuring consistent demand for standard projection screens across both developed and emerging markets. Furthermore, smaller and mid-sized theatres prefer 2D setups due to their cost-effectiveness and simpler infrastructure requirements.

However, 3D projection and premium formats are steadily expanding, fueled by increasing demand for immersive cinematic experiences. Premium formats, including IMAX and Dolby Cinema, are particularly driving screen upgrades in developed markets. LED cinema screens are emerging as a high-growth application segment, supported by advancements in display technology and declining costs. Additionally, outdoor and event-based applications are gaining momentum, driven by the rising popularity of live screenings, esports events, and community cinema experiences, further diversifying application demand.

Distribution Channel Insights

Direct sales to multiplex chains and large cinema operators dominate the distribution landscape, as these buyers require customized solutions, large-scale installations, and long-term service agreements. This segment leads due to the complexity and capital-intensive nature of cinema screen installations, which often involve integration with projection systems, sound equipment, and auditorium design. Long-term partnerships between manufacturers and cinema chains also ensure recurring revenue through maintenance and upgrade contracts.

Equipment suppliers and system integrators play a critical role in delivering turnkey solutions, including installation, calibration, and after-sales support. These players act as intermediaries, particularly in emerging markets where local expertise is essential. Rental and leasing models are emerging as alternative distribution channels, especially for event-based applications and smaller operators. These models are gaining traction due to their lower upfront costs and flexibility, enabling broader adoption among non-traditional end-users.

End-Use Insights

Commercial multiplex chains dominate the end-use segment, accounting for nearly 60% of the global market demand in 2025. The leadership of this segment is driven by the continuous expansion of multiplex infrastructure, particularly in high-growth regions such as Asia-Pacific and the Middle East. Multiplex operators are also investing heavily in upgrading existing screens to premium formats, further strengthening demand. The ability of multiplexes to generate higher footfall and offer diversified viewing experiences makes them the primary revenue driver for screen manufacturers.

Independent theatres and drive-in cinemas contribute to steady demand, particularly in regional and rural markets where multiplex penetration remains limited. The event and rental segment is the fastest-growing end-use category, supported by increasing demand for outdoor screenings, live sports broadcasting, and corporate events. Institutional applications, including education, defense, and government sectors, are also emerging as niche contributors, particularly for specialized simulation and training environments requiring high-quality visual display systems.

Explore more data points, trends and opportunities Download Free Sample Report

Cinema Screens Market Segmentations

By Product Type

- Fixed Frame Screens

- Motorised Screens

- Portable Screens

- Curved & Premium Large Format Screens

- LED Cinema Screens

By Application

- 2D Projection

- 3D Projection

- Premium Large Format

- LED Direct View Cinema

- Outdoor & Event-Based Screening

By Distribution Channel

- Direct Sales to Multiplex Chains

- System Integrators & Equipment Suppliers

- Rental & Leasing Providers

- Specialty AV Distributors

Regional Insights

Asia-Pacific

Asia-Pacific leads the global cinema screens market, accounting for approximately 38% of the total market share in 2025. The region’s dominance is primarily driven by rapid urbanization, expanding middle-class populations, and significant investments in multiplex infrastructure. China remains the largest market, supported by its extensive cinema network and continuous screen additions. India is the fastest-growing country in the region, with a CAGR exceeding 9%, driven by aggressive multiplex expansion, favorable government policies, and increasing consumer spending on entertainment. Southeast Asian countries such as Indonesia and Vietnam are also witnessing strong growth due to rising disposable incomes and improving cinema penetration. Additionally, local film industries and increasing content production are further fueling demand for cinema screens across the region.

North America

North America holds approximately 25% of the global market share, with the United States being the dominant contributor. The region’s growth is driven by high adoption of premium large-format screens, frequent technological upgrades, and strong consumer demand for immersive cinema experiences. Cinema operators in North America are early adopters of advanced technologies such as laser projection and LED screens, which is driving replacement demand. Additionally, the presence of major film studios and a strong theatrical release pipeline continues to support steady demand for high-performance cinema screens.

Europe

Europe accounts for nearly 20% of the global market, with key countries including the United Kingdom, Germany, and France leading demand. The region’s growth is primarily driven by the modernization of legacy cinema infrastructure and the increasing adoption of premium viewing formats. Government support for cultural and entertainment sectors, along with strong consumer preference for theatrical experiences, is further supporting market expansion. Additionally, sustainability initiatives are encouraging the adoption of energy-efficient projection systems and screen materials, influencing replacement cycles across the region.

Middle East & Africa

The Middle East & Africa region is the fastest-growing market, with a CAGR exceeding 10%. Growth is primarily driven by large-scale investments in entertainment infrastructure, particularly in countries such as Saudi Arabia and the UAE. Government initiatives to diversify economies and promote tourism and entertainment sectors are accelerating cinema development. The reopening and expansion of cinemas in Saudi Arabia have significantly boosted screen installations, while high disposable incomes in the UAE are supporting demand for premium formats. In Africa, gradual improvements in infrastructure and increasing urbanization are contributing to steady market growth.

Latin America

Latin America accounts for approximately 7% of the global market, with Brazil and Mexico serving as key contributors. The region’s growth is supported by increasing cinema penetration, rising urban populations, and growing consumer spending on entertainment. Expansion of regional multiplex chains and international cinema operators is driving new screen installations. Additionally, improving economic conditions and increasing availability of localized content are encouraging higher theatre attendance, thereby supporting demand for cinema screens. However, growth remains moderate compared to other regions due to economic volatility and limited large-scale investments.

Key Players in the Cinema Screens Market

- Harkness Screens

- Severtson Screens

- Stewart Filmscreen

- Strong/MDI Screen Systems

- Screen Research

- Barco

- Sony Corporation

- Samsung Electronics

- LG Electronics

- NEC Display Solutions

- Draper Inc.

- Da-Lite Screen Company

- Elite Screens

- Volfoni

- IMAX Corporation