Cinema Lenses Market Size

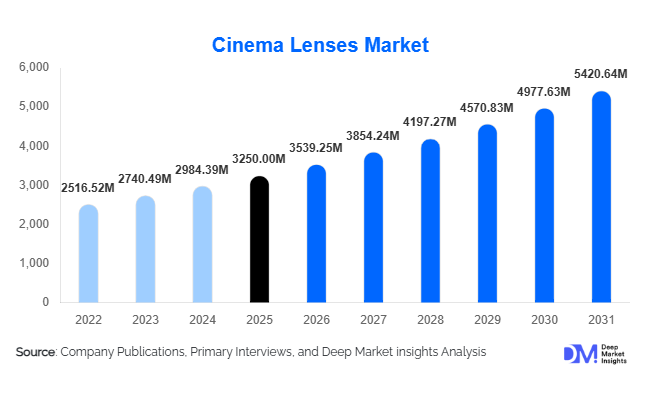

According to Deep Market Insights, the global cinema lenses market size was valued at USD 3,250 million in 2025 and is projected to grow from USD 3,539.25 million in 2026 to reach USD 5,420.64 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The cinema lenses market growth is primarily driven by the rapid expansion of global film production, the surge in OTT and streaming content creation, and increasing demand for high-resolution digital cinematography equipment capable of supporting 4K, 6K, and 8K video production.

Cinema lenses are specialized optical systems designed for professional filmmaking, delivering superior optical precision, consistent color rendering, minimal distortion, and precise focus control compared to traditional photography lenses. As digital filmmaking technologies continue to evolve, production houses and cinematographers are increasingly investing in premium lenses to enhance visual storytelling and meet the technical standards required by major streaming platforms and theatrical releases.

Additionally, the growing popularity of equipment rental houses is making high-end cinema lenses more accessible to independent filmmakers and smaller production studios. Emerging film production hubs in Asia-Pacific, Eastern Europe, and the Middle East are also contributing to market expansion as governments introduce incentives to attract international film projects. Continuous advancements in optical engineering, lightweight lens materials, and electronic metadata integration are further supporting the adoption of next-generation cinema lenses across professional production environments.

Key Market Insights

- Prime cinema lenses dominate the market, accounting for nearly 46% of global demand due to superior optical quality and wide aperture capabilities preferred in professional filmmaking.

- North America leads the global cinema lenses market, supported by Hollywood studios, strong production infrastructure, and high investments in cinematography equipment.

- Asia-Pacific is the fastest-growing region, driven by expanding film industries in China, India, South Korea, and Japan.

- OTT content production is accelerating demand for professional cinema lenses as streaming platforms invest heavily in high-quality original content.

- Large-format cinematography is emerging as a major trend, increasing demand for lenses compatible with full-frame and large-sensor cinema cameras.

- Equipment rental ecosystems are expanding globally, allowing production companies to access high-end cinema lenses without large capital investments.

What are the latest trends in the cinema lenses market?

Shift Toward Large-Format Cinematography

One of the most notable trends in the cinema lenses market is the growing adoption of large-format cinematography. Modern cinema cameras are increasingly designed with larger sensors capable of capturing greater image detail, improved dynamic range, and enhanced depth-of-field control. This shift has created strong demand for lenses capable of covering larger image circles while maintaining exceptional optical clarity. Large-format lenses are becoming popular among cinematographers for feature films, streaming series, and high-end advertising productions due to their ability to produce immersive visuals and cinematic aesthetics.

Lens manufacturers are responding to this trend by launching dedicated large-format lens families that offer improved resolution, lighter construction, and compatibility with next-generation cinema cameras. These lenses often command premium prices, contributing significantly to revenue growth within the cinema lenses market.

Integration of Smart Lens Technology

The integration of electronic and smart lens technologies is transforming filmmaking workflows. Modern cinema lenses are increasingly equipped with electronic contacts capable of transmitting metadata such as focus distance, aperture settings, and lens distortion information directly to camera systems. This metadata enables improved post-production workflows, allowing editors and visual effects teams to replicate camera movements, correct distortions, and enhance visual effects integration.

Smart lens technologies are particularly important for productions involving computer-generated imagery (CGI) and advanced visual effects. As virtual production techniques become more widespread across the film industry, demand for electronically enabled cinema lenses is expected to grow rapidly.

What are the key drivers in the cinema lenses market?

Expansion of Global Film and Television Production

The increasing volume of global film and television production is a major driver for the cinema lenses market. Streaming platforms and international broadcasters are investing billions of dollars annually in original content to attract global audiences. This surge in content production has created significant demand for professional cinematography equipment, including advanced cinema lenses capable of delivering cinematic image quality.

Film industries in countries such as the United States, India, China, South Korea, and the United Kingdom are producing an increasing number of films and television series each year. As production standards rise, filmmakers are prioritizing high-end optics that deliver consistent image quality across multiple shooting conditions.

Advancements in Digital Cinematography Technology

Technological advancements in digital cinema cameras are also driving the adoption of advanced lenses. Modern cameras now support ultra-high-definition recording formats such as 6K and 8K, which require extremely precise optics to maintain image sharpness and color accuracy. Cinema lenses designed for high-resolution sensors are therefore becoming essential equipment for professional productions.

In addition, innovations such as improved coatings, reduced focus breathing, and enhanced mechanical design are improving lens performance and durability, further encouraging adoption across the filmmaking industry.

What are the restraints for the global market?

High Cost of Professional Cinema Lenses

Professional cinema lenses are significantly more expensive than consumer photography lenses due to their complex optical designs, precision manufacturing processes, and lower production volumes. Individual lenses can cost tens of thousands of dollars, creating a financial barrier for smaller production studios and independent filmmakers.

Although rental services mitigate this challenge to some extent, the high upfront investment required for lens ownership remains a key restraint affecting widespread adoption across emerging film industries.

Rapid Technological Evolution

The cinema equipment industry is characterized by rapid technological change. Camera sensors continue to evolve in terms of resolution and size, requiring lens manufacturers to constantly adapt optical designs. This rapid pace of innovation increases research and development costs and can shorten product life cycles for cinema lenses, posing challenges for manufacturers seeking long-term product stability.

What are the key opportunities in the cinema lenses industry?

Growth of OTT Content Production

The global expansion of OTT streaming platforms presents one of the most significant opportunities for cinema lens manufacturers. Streaming companies are producing vast amounts of original content across multiple genres and languages to expand subscriber bases. These productions often require high-quality cinematography equipment that meets strict technical standards for resolution, color accuracy, and image consistency.

As OTT platforms continue expanding into emerging markets, local production ecosystems are developing rapidly, creating strong demand for cinema lenses among regional production houses and rental companies.

Emerging Film Production Hubs

Governments across Asia, Eastern Europe, and the Middle East are investing heavily in film production infrastructure to attract international productions. Tax incentives, rebates, and government-supported studio facilities are encouraging global studios to film in these regions.

As production activity increases, demand for professional cinematography equipment, including cinema lenses, is expected to grow significantly. Manufacturers that establish regional distribution networks and service centers in these emerging markets will benefit from expanding industry ecosystems.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3250 Million |

| Market Size in 2026 | USD 3539.25 Million |

| Market Size in 2031 | USD 5420.64 Million |

| CAGR | 8.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Lens Type Insights

Prime cinema lenses represent the largest segment within the market, accounting for nearly 46% of global demand. These lenses are widely preferred by cinematographers due to their superior optical quality, minimal distortion, and ability to achieve wider apertures compared to zoom lenses. Prime lenses also provide consistent visual characteristics across focal lengths, making them ideal for narrative filmmaking where visual continuity is essential. Zoom cinema lenses represent another important segment, particularly for television productions, documentaries, and live broadcast events where rapid focal length adjustments are necessary. Anamorphic lenses are gaining popularity in high-end productions due to their distinctive cinematic look, producing wide aspect ratios and characteristic lens flares that enhance visual storytelling.

Application Insights

Feature film production remains the largest application segment in the cinema lenses market, accounting for approximately 34% of total demand. High-budget film productions require multiple lens sets for different shooting conditions, contributing significantly to market revenue. Television and OTT series production represents the fastest-growing application segment as streaming platforms significantly increase content production budgets. Advertising production is another major application area, as brands invest in high-quality commercial videos and digital marketing campaigns that require professional cinematography equipment.

Distribution Channel Insights

Direct sales from manufacturers remain an important distribution channel for large production houses and equipment rental companies that purchase cinema lenses in bulk. Professional camera equipment dealers also play a key role in distributing cinema lenses to studios and cinematographers worldwide. Equipment rental houses are a particularly influential distribution channel in this market. These companies maintain extensive inventories of high-end lenses and rent them to film crews on a project basis, enabling filmmakers to access premium equipment without making significant capital investments.

End-Use Insights

Film production houses represent the largest end-use segment within the cinema lenses market due to the extensive equipment requirements associated with feature film production. Major studios typically maintain multiple lens sets to support different shooting styles and creative approaches. OTT content production companies are emerging as the fastest-growing end-use segment as streaming platforms rapidly expand their original programming portfolios. Equipment rental companies also play a crucial role in the industry, acting as intermediaries that supply cinema lenses to production teams across multiple projects.

Explore more data points, trends and opportunities Download Free Sample Report

Cinema Lenses Market Segmentations

By Lens Type

- Prime Cinema Lenses

- Zoom Cinema Lenses

- Anamorphic Cinema Lenses

- Spherical Cinema Lenses

- Macro Cinema Lenses

- Specialty Cinema Lenses

By Mount Type

- PL Mount

- EF Mount

- E Mount

- LPL Mount

- RF Mount

- Micro Four Thirds Mount

By Sensor Format Compatibility

- Full Frame / Large Format Cinema Lenses

- Super 35 Cinema Lenses

- APS-C Cinema Lenses

- Micro Four Thirds Cinema Lenses

- VistaVision / Large Sensor Lenses

By Application

- Feature Film Production

- Television and OTT Series Production

- Commercial Advertising Production

- Documentary Production

- Live Broadcast and Events

- Music Video Production

By End User

- Film Production Houses

- Television Studios

- OTT Content Production Companies

- Equipment Rental Houses

- Independent Cinematographers

- Film and Media Institutes

Regional Insights

North America

North America holds the largest share of the global cinema lenses market, accounting for approximately 38% of total demand in 2025. The United States dominates the region due to the presence of Hollywood studios, advanced production infrastructure, and strong investment in high-end filmmaking technologies. Canada also contributes significantly to regional demand, particularly through international film productions that take advantage of tax incentives and well-developed studio facilities in cities such as Vancouver and Toronto.

Europe

Europe represents approximately 27% of the global cinema lenses market. The United Kingdom, Germany, and France are the primary contributors to regional demand. The UK is a major hub for international film production due to its large studio complexes and highly skilled film workforce. European cinematographers are also early adopters of advanced lens technologies, supporting steady growth in the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by expanding film industries in China, India, South Korea, and Japan. India produces one of the largest numbers of films globally each year, creating consistent demand for professional cinematography equipment. South Korea’s internationally recognized film and television industry is also contributing to the rising demand for cinema lenses across the region.

Latin America

Latin America is witnessing gradual growth in cinema lens demand, particularly in Brazil and Mexico where regional film industries continue to expand. International film productions are increasingly using locations across the region, which is supporting equipment demand from local rental companies.

Middle East & Africa

The Middle East is emerging as an attractive film production destination due to government incentives and investments in media infrastructure. Countries such as the UAE and Saudi Arabia are establishing film studios and introducing production incentives to attract international projects. These initiatives are gradually increasing demand for cinema lenses and other professional filmmaking equipment.

Key Players in the Cinema Lenses Market

- ZEISS Group

- Cooke Optics

- Angénieux

- ARRI

- Canon Inc.

- Fujifilm Holdings Corporation

- Sony Corporation

- Leica Camera AG

- Sigma Corporation

- Samyang Optics

- Tokina

- Laowa (Venus Optics)

- Vantage Film

- DZOFILM

- Irix Lens