Children Toys Market Size

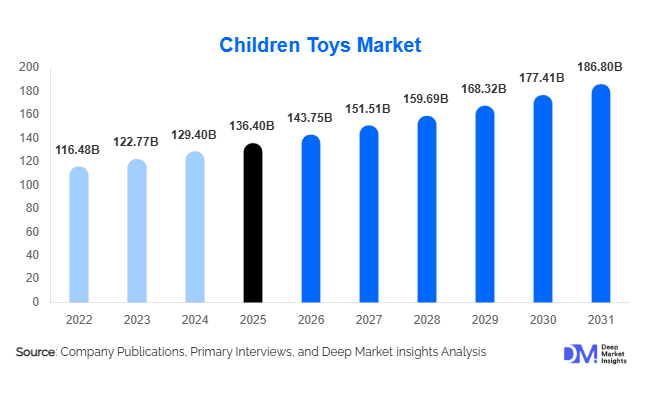

According to Deep Market Insights, the global Children Toys Market size was valued at USD 136.4 billion in 2025 and is projected to grow from USD 143.75 billion in 2026 to reach USD 186.8 billion by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The market growth is primarily driven by rising demand for educational and STEM-based toys, increasing penetration of e-commerce distribution channels, growing influence of entertainment franchises and licensed products, and expanding consumer preference for sustainable and technology-enabled toys.

Key Market Insights

- Educational and STEM toys are becoming the fastest-growing category, driven by parental focus on cognitive development, coding skills, and early learning outcomes.

- Construction toys and licensed collectibles dominate global revenue share, supported by strong franchise ecosystems and long product life cycles.

- Asia Pacific is the fastest-growing region, fueled by rising disposable incomes in China, India, and Southeast Asia.

- North America remains the largest consumption market, led by high per-capita spending and strong entertainment licensing networks.

- E-commerce and direct-to-consumer channels are reshaping distribution, significantly improving accessibility and global reach.

- Smart toys and AI-enabled interactive products are transforming traditional play patterns, especially in urban premium markets.

What are the latest trends in the Children Toys Market?

Rising Adoption of Educational and STEM-Based Play

The global toy industry is witnessing a structural shift toward educational value creation, with STEM toys, robotics kits, coding-based learning sets, and cognitive development tools gaining strong momentum. Parents are increasingly prioritizing toys that combine entertainment with skill-building outcomes such as problem-solving, creativity, and analytical thinking. Schools and daycare centers are also integrating structured play tools into early education systems, further strengthening demand. This trend is especially prominent in developed economies like the United States, Germany, Japan, and South Korea, while rapidly expanding in emerging markets such as India and China.

Digital Integration and Smart Toy Evolution

The integration of artificial intelligence, IoT, augmented reality, and app-based interaction is reshaping the toy industry. Smart toys that respond to voice commands, adapt learning levels, or connect with mobile applications are gaining popularity among tech-savvy parents. Hybrid physical-digital play experiences are emerging as a key trend, particularly in premium product categories. This technological evolution is enabling manufacturers to extend product lifecycles, increase engagement time, and create personalized learning experiences for children.

What are the key drivers in the Children Toys Market?

Growing Influence of Entertainment Licensing

Licensing agreements with movie franchises, gaming brands, sports leagues, and animation studios are significantly driving toy sales globally. Character-based toys and collectibles linked to popular franchises generate strong emotional engagement and repeat purchases. Licensed toys also command higher price points and contribute substantially to manufacturer profitability. This driver is particularly strong in North America and Europe, where entertainment ecosystems are highly developed and globally influential.

Expansion of E-Commerce and Omnichannel Retail

The rapid expansion of online retail platforms is transforming global toy distribution. Consumers now benefit from wider product selection, competitive pricing, and doorstep delivery convenience. Digital marketplaces are enabling smaller brands to reach global audiences without traditional retail dependency. Emerging economies such as India, Brazil, and Indonesia are witnessing particularly strong growth in online toy purchases, supported by increasing smartphone penetration and digital payment adoption.

Rising Demand for Educational and Developmental Toys

Parents are increasingly prioritizing toys that support early childhood development, including motor skills, creativity, language learning, and STEM education. This shift is driving demand for puzzles, building blocks, robotics kits, and learning-based games. The trend is reinforced by increasing awareness of child development psychology and curriculum-aligned play activities.

What are the restraints for the global market?

Rising Raw Material and Production Costs

Fluctuations in plastic resin prices, electronic components, packaging materials, and logistics costs are significantly impacting manufacturing margins. Compliance with safety regulations and quality standards further increases production expenses, particularly for small and mid-sized manufacturers. These cost pressures limit pricing flexibility in highly competitive mass-market segments.

Competition from Digital Entertainment Platforms

The growing dominance of mobile gaming, streaming platforms, and social media content is reducing traditional toy engagement time among children. Increasing screen dependency is creating structural competition for physical toys, particularly in developed markets. Manufacturers are responding by integrating digital and interactive features into traditional toy formats.

What are the key opportunities in the Children Toys Market?

Expansion of STEM and Robotics-Based Learning Toys

Growing emphasis on future-ready skills such as coding, engineering, and digital literacy presents a major opportunity for toy manufacturers. STEM-focused products are increasingly being adopted by schools, educational institutions, and parents seeking structured learning outcomes. This segment offers strong long-term growth potential due to alignment with global education reforms.

Growth of Kidult and Collectibles Segment

Adult consumers purchasing toys for nostalgia, collecting, and hobby-based engagement represent a rapidly expanding segment. Construction sets, anime figures, gaming collectibles, and limited-edition merchandise are gaining strong traction. This segment delivers higher margins and repeat purchases, making it highly attractive for global brands.

Sustainability and Eco-Friendly Toy Manufacturing

Rising environmental awareness is driving demand for toys made from recyclable plastics, wood, organic materials, and biodegradable packaging. Companies adopting sustainable manufacturing practices are gaining a competitive advantage, particularly in Europe and North America, where regulatory standards and consumer expectations are high.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 136.4 Billion |

| Market Size in 2026 | USD 143.75 Billion |

| Market Size in 2031 | USD 186.8 Billion |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Building and construction toys dominate the global Children Toys Market, accounting for approximately 24.8% of total market revenue in 2025. The segment continues to lead due to its strong appeal across multiple age groups, ranging from preschool children to adult collectors and hobbyists. Demand is particularly driven by the educational and developmental benefits associated with construction-based play, including problem-solving, creativity enhancement, spatial awareness, and motor skill development. Premium licensed building sets linked to movies, gaming franchises, and entertainment characters are further accelerating segment growth, especially in North America and Europe. In addition, the rapidly expanding “kidult” demographic is significantly increasing repeat purchases and premium product adoption within this category. Educational and STEM toys account for nearly 16.5% of the global market and represent the fastest-growing product category globally. Rising parental focus on coding, robotics, engineering skills, and early cognitive development is driving demand for interactive learning toys, robotics kits, and science-based educational products. Governments and educational institutions are increasingly integrating STEM-focused learning tools into classrooms and daycare environments, particularly across the United States, China, Japan, Germany, and India. This segment is also benefiting from growing awareness regarding experiential learning and future-ready skill development among parents.

Dolls, plush toys, and action figures continue to maintain a strong market presence due to the continued expansion of global licensing ecosystems. Character-based toys linked to animated films, superheroes, gaming franchises, anime, and streaming content are generating substantial demand among children and collectors alike. Electronic and smart toys are witnessing accelerated growth as manufacturers integrate artificial intelligence, voice interaction, augmented reality, and app connectivity into product portfolios. Smart toys capable of adaptive learning and personalized engagement are gaining popularity in premium urban markets where parents prioritize technologically advanced educational experiences. Outdoor and sports toys remain highly important in child development-oriented purchasing, especially among parents emphasizing physical activity and reduced screen exposure. Ride-on toys, scooters, sports kits, and water-play products continue to experience stable demand globally. Meanwhile, collectibles and trading toys are rapidly gaining traction among teenage and adult demographics due to rising fandom culture, limited-edition product launches, influencer-driven trends, and the expansion of gaming and anime-related merchandise categories.

End-Use Insights

Residential and household consumption remains the dominant end-use segment in the Children Toys Market, accounting for nearly 72% of total global demand in 2025. The segment is primarily driven by increasing household expenditure on educational products, birthday gifting, festive purchases, and entertainment-oriented toys. Rising disposable income levels, especially in urban households across the Asia Pacific and North America, continue to support strong retail demand. Parents are increasingly prioritizing toys that combine entertainment with developmental benefits, significantly strengthening demand for educational puzzles, building kits, robotics sets, and sensory toys. Educational institutions and daycare centers are among the fastest-growing end-use segments globally. Schools, kindergartens, preschools, and childcare centers are increasingly incorporating structured play tools into learning environments to improve cognitive development, social interaction, and motor skill enhancement. STEM learning kits, coding toys, language-learning games, and sensory products are seeing particularly strong institutional demand. Government-supported early childhood education initiatives in countries such as the United States, China, Germany, India, and South Korea are further supporting segment expansion.

Therapy centers, pediatric hospitals, and rehabilitation clinics are emerging as niche but strategically important end-use segments. Sensory toys, autism-support products, motor skill development tools, and cognitive therapy games are increasingly used in pediatric therapy programs and behavioral development treatments. The growing awareness surrounding developmental disorders and sensory learning is supporting long-term demand within this category. Export-driven manufacturing demand remains a critical component of the global Children Toys Market. China continues to dominate global toy exports due to its highly integrated manufacturing ecosystem, strong supplier base, and large-scale production capabilities. However, countries such as India and Vietnam are rapidly emerging as alternative manufacturing hubs due to lower labor costs, government incentives, export-focused industrial policies, and global supply chain diversification strategies adopted by multinational toy companies.

Explore more data points, trends and opportunities Download Free Sample Report

Children Toys Market Segmentations

By Product Type

- Building & Construction Toys

- Dolls & Plush Toys

- Action Figures & Roleplay Toys

- Educational & STEM Toys

- Electronic & Smart Toys

- Games & Puzzles

- Outdoor & Sports Toys

- Arts, Crafts & DIY Toys

- Vehicles & Remote-Control Toys

- Collectibles & Trading Toys

By Material Type

- Plastic Toys

- Wooden Toys

- Fabric & Plush Materials

- Metal-Based Toys

- Eco-friendly & Biodegradable Materials

By Distribution Channel

- Hypermarkets & Supermarkets

- Specialty Toy Stores

- Department Stores

- Online Retail/E-commerce

- Direct-to-Consumer Brand Stores

- Convenience & Discount Stores

By Technology Integration

- Traditional Non-electronic Toys

- Battery-operated Toys

- Connected/IoT Toys

- AI-enabled Interactive Toys

- AR/VR-Enabled Toys

By End Use

- Residential/Home Use

- Educational Institutions

- Childcare Centers & Daycare

- Hospitals & Therapy Centers

- Recreational & Entertainment Centers

- Gift & Seasonal Purchasing

Regional Insights

North America

North America accounted for approximately 33% of the global Children Toys Market revenue in 2025, making it the largest regional market globally. The United States dominates regional demand due to high consumer spending power, widespread penetration of premium toy brands, and strong entertainment licensing ecosystems linked to movies, gaming franchises, and streaming platforms. The region also demonstrates high adoption of educational and STEM-based toys as parents increasingly prioritize cognitive development and early learning outcomes. Rapid integration of smart toys, AI-enabled learning products, and connected gaming experiences is further supporting market expansion across urban consumer groups. In addition, the strong presence of organized retail chains, advanced e-commerce infrastructure, and seasonal gifting culture significantly contribute to market growth. Canada also maintains a steady demand for educational toys, collectibles, and eco-friendly products due to rising sustainability awareness and premium purchasing trends.

Europe

Europe represents nearly 27% of global market revenue, led by Germany, the United Kingdom, France, Italy, and Spain. The regional market is strongly driven by growing demand for sustainable, eco-friendly, and educational toys. European consumers demonstrate a high preference for non-toxic materials, wooden toys, recyclable packaging, and environmentally responsible manufacturing practices. Strict regulatory standards related to toy safety and chemical compliance are also encouraging manufacturers to focus on high-quality production and sustainable innovation. Germany remains a major market for construction toys and STEM learning products due to strong educational integration and high household spending on child development tools. The United Kingdom is witnessing significant growth in online toy retail and licensed merchandise, while France and Italy continue to support demand for creative play, arts & crafts, and preschool learning toys. Increasing awareness of screen-free developmental play is further boosting demand for traditional and educational toy categories across the region.

Asia Pacific

Asia Pacific accounted for approximately 29% of the global Children Toys Market in 2025 and is projected to remain the fastest-growing regional market through 2031. China dominates both regional manufacturing and consumer demand due to its massive production infrastructure, integrated supply chain ecosystem, and expanding middle-class population. Rising urbanization, increasing disposable income, and growing parental investment in educational products continue to support strong domestic demand. India is emerging as one of the fastest-growing toy markets globally, driven by favorable demographics, rising birth rates, rapid e-commerce expansion, and government initiatives supporting domestic manufacturing under programs such as “Make in India.” Japan and South Korea remain highly influential markets for premium collectibles, anime merchandise, robotics toys, and technologically advanced learning products. Southeast Asian countries, including Indonesia, Vietnam, and Thailand, are also witnessing rising toy consumption due to improving retail infrastructure and growing middle-income populations.

Latin America

Latin America holds approximately 6% of the global market share, with Brazil and Mexico representing the largest regional markets. The market is primarily driven by rising urbanization, improving retail accessibility, and increasing penetration of international toy brands. Growing middle-class spending and expanding e-commerce infrastructure are improving product availability across major metropolitan regions. Brazil remains the leading regional market due to its large child population and increasing demand for affordable educational toys and licensed products. Mexico benefits from strong trade connectivity with North America and increasing retail investments by global brands. Seasonal gifting traditions, expanding organized retail, and growing smartphone penetration are also supporting online toy sales across the region.

Middle East & Africa

The Middle East & Africa region accounted for approximately 5% of global Children Toys Market revenue in 2025, with growth largely concentrated in the Gulf Cooperation Council countries and South Africa. The UAE and Saudi Arabia are emerging as key premium toy consumption markets due to rising disposable income, luxury retail expansion, and strong demand for international brands. Increasing investments in shopping malls, family entertainment centers, and organized retail infrastructure are further supporting regional growth. Educational reform initiatives and rising awareness regarding child development are also increasing demand for STEM-based learning toys across urban populations. In Africa, South Africa remains the largest toy market due to comparatively advanced retail networks and growing demand for affordable educational and outdoor toys. Rising internet penetration and improving digital commerce infrastructure are expected to gradually expand regional market accessibility over the coming years.

Key Players in the Children Toys Market

- LEGO Group

- Mattel Inc.

- Hasbro Inc.

- Bandai Namco Holdings

- Spin Master Corp.

- TOMY Company Ltd.

- VTech Holdings Ltd.

- MGA Entertainment

- Ravensburger AG

- Jazwares LLC