Chest Bags Market Size

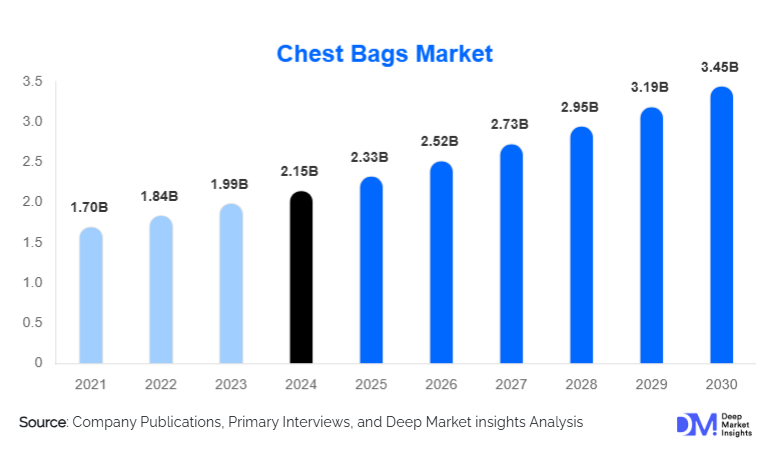

According to Deep Market Insights, the global chest bags market size was valued at USD 2.15 billion in 2025 and is projected to grow from USD 2.33 billion in 2026 to reach USD 3.45 billion by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The chest bags market growth is primarily driven by rising urban mobility needs, increasing preference for compact and hands-free carry solutions, and the growing influence of streetwear and athleisure fashion across global consumer segments.

Key Market Insights

- Chest bags are transitioning from utility accessories to lifestyle fashion products, driven by streetwear culture and influencer-led trends.

- Asia-Pacific dominates the global market, supported by large-scale manufacturing, rising urban populations, and export-oriented production.

- Online retail channels account for the majority of sales, benefiting from direct-to-consumer models and global e-commerce penetration.

- Mid-range priced chest bags lead demand, offering an optimal balance between affordability, durability, and design innovation.

- Sustainability-focused materials, including recycled polyester and vegan leather, are gaining strong consumer traction.

- Technology-enabled features such as anti-theft systems, RFID protection, and smart charging are reshaping product differentiation.

What are the latest trends in the chest bags market?

Rise of Streetwear and Urban Lifestyle Adoption

Chest bags have become a staple accessory in global streetwear fashion, driven by endorsements from celebrities, athletes, and social media influencers. Once positioned purely as functional carry gear, chest bags are now integrated into everyday fashion ensembles. Minimalist designs, bold branding, and seasonal color palettes are being introduced by both sportswear and lifestyle brands. This trend is particularly strong among millennials and Gen Z consumers, who prioritize versatility and visual appeal alongside functionality. Limited-edition collaborations between fashion designers and sportswear brands are further elevating the premium positioning of chest bags.

Technology-Enhanced and Anti-Theft Designs

Manufacturers are increasingly integrating technology-driven features into chest bags to address urban security and convenience needs. Anti-theft zippers, slash-resistant materials, RFID-blocking pockets, and USB charging ports are becoming mainstream in mid-range and premium products. Smart chest bags with tracking modules and modular compartments are also emerging, catering to travelers, commuters, and professionals. These innovations are enhancing perceived value and allowing brands to command higher margins, particularly in developed markets where consumers prioritize safety and connectivity.

What are the key drivers in the chest bags market?

Growth in Urban Mobility and Hands-Free Convenience

The rapid expansion of urban mobility solutions such as cycling, e-scooters, and public transit has significantly increased demand for compact, hands-free carry accessories. Chest bags offer superior weight distribution, accessibility, and security compared to backpacks or handbags, making them ideal for daily commuting. This driver is especially prominent in densely populated cities across Asia-Pacific and Europe, where mobility efficiency and personal security are key considerations.

Influence of Athleisure and Casual Fashion

The global athleisure trend has blurred the line between functional gear and fashion accessories. Chest bags align perfectly with this shift, offering casual aesthetics combined with utility. Sportswear brands and outdoor equipment manufacturers are leveraging this trend by launching lifestyle-focused chest bag collections that appeal beyond sports and travel use. This has expanded the consumer base and increased average selling prices.

What are the restraints for the global market?

Price Sensitivity in Emerging Economies

While demand is growing, consumers in developing markets remain highly price-conscious. Premium and technology-enabled chest bags face adoption challenges in price-sensitive regions, limiting penetration beyond the economy and mid-range segments. Fluctuating raw material prices further pressure manufacturers’ ability to maintain competitive pricing.

Competition from Substitute Carry Products

Chest bags face ongoing competition from backpacks, waist packs, and tote bags. Shifting fashion trends and seasonal preferences can redirect consumer spending toward alternative accessories, posing a challenge to consistent demand growth.

What are the key opportunities in the chest bags industry?

Sustainable and Eco-Friendly Product Development

Growing environmental awareness presents strong opportunities for brands to innovate using recycled fabrics, biodegradable packaging, and ethical sourcing practices. Eco-friendly chest bags are gaining traction among environmentally conscious consumers, particularly in Europe and North America. Brands adopting sustainability certifications and circular economy models are expected to gain a competitive advantage.

Expansion into Emerging Urban Markets

Rapid urbanization in India, Southeast Asia, Latin America, and Africa presents significant growth potential. Rising disposable incomes, expanding youth populations, and exposure to global fashion trends are driving demand for affordable yet stylish chest bags. Localized designs and regional pricing strategies can unlock high-volume growth in these markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.15 Billion |

| Market Size in 2026 | USD 2.33 Billion |

| Market Size in 2031 | USD 3.45 Billion |

| CAGR | 8.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Soft-shell chest bags dominate the market due to their lightweight construction, flexibility, and affordability, accounting for approximately 42% of global revenue in 2025. Tactical and utility chest bags are gaining popularity among outdoor enthusiasts and professionals, while smart and hard-shell chest bags are emerging as premium offerings targeting travelers and urban commuters seeking enhanced protection and organization.

Material Insights

Polyester remains the most widely used material, representing nearly 38% of total market value, owing to its durability, water resistance, and cost efficiency. Nylon follows closely, particularly in premium and tactical applications. Leather and synthetic leather chest bags cater to fashion-conscious consumers, while eco-friendly materials are the fastest-growing segment as sustainability becomes a key purchase criterion.

Distribution Channel Insights

Online retail channels account for approximately 58% of global chest bag sales, driven by brand websites, e-commerce marketplaces, and social media commerce. Offline retail, including specialty stores and department stores, remains important for premium and experiential purchases. Direct-to-consumer strategies are enabling brands to improve margins and strengthen customer engagement.

End-Use Insights

Daily casual and urban use represents the largest end-use segment, contributing around 44% of total demand. Travel and tourism, as well as sports and outdoor activities, are the fastest-growing segments, supported by rising global travel and recreational participation. Professional and tactical applications are also expanding, particularly among delivery personnel, photographers, and security professionals.

Explore more data points, trends and opportunities Download Free Sample Report

Chest Bags Market Segmentations

By Product Type

- Soft-Shell Chest Bags

- Hard-Shell Chest Bags

- Tactical & Utility Chest Bags

- Anti-Theft Chest Bags

- Smart & Tech-Enabled Chest Bags

By Material Type

- Polyester

- Nylon

- Leather & Synthetic Leather

- Canvas

- Eco-Friendly & Recycled Materials

By Capacity

- Small (≤3 Liters)

- Medium (3–6 Liters)

- Large (>6 Liters)

By Price Range

- Economy (≤ USD 25)

- Mid-Range (USD 25–75)

- Premium (≥ USD 75)

By Distribution Channel

- Online Retail

- Offline Retail

Regional Insights

Asia-Pacific

Asia-Pacific leads the global chest bags market with approximately 36% share in 2025. China is the largest producer and consumer, while India and Southeast Asia represent the fastest-growing demand centers due to urbanization and rising middle-class incomes.

North America

North America accounts for around 24% of global demand, driven by premium product adoption, strong e-commerce penetration, and high consumer spending on lifestyle accessories. The United States dominates regional consumption.

Europe

Europe holds roughly 21% of the market, supported by strong fashion orientation and demand for sustainable products. Germany, the UK, France, and Italy are key markets.

Latin America

Latin America contributes about 11% of global revenue, with Brazil and Mexico leading regional growth as urban fashion adoption increases.

Middle East & Africa

The Middle East & Africa region accounts for nearly 8% of the market, supported by tourism-driven demand and rising lifestyle retail in the UAE and Saudi Arabia.