Cheque Scanner Market Size

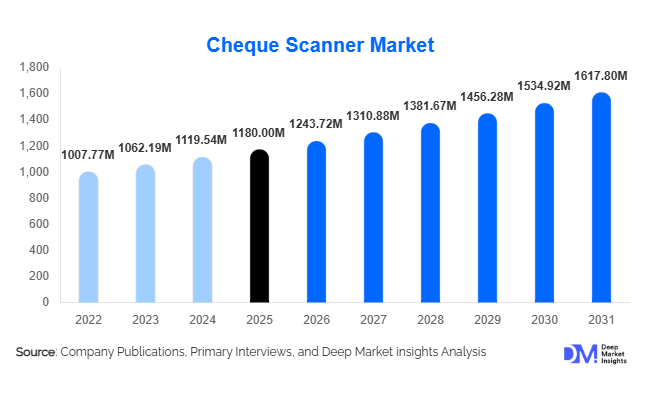

According to Deep Market Insights, the global cheque scanner market size was valued at USD 1,180 million in 2025 and is projected to grow from USD 1,243.72 million in 2026 to reach USD 1,617.80 million by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The cheque scanner market growth is primarily driven by continued institutional cheque usage, regulatory mandates supporting cheque truncation systems (CTS), and increasing integration of image-based remote deposit capture (RDC) technologies across banking networks.

Although retail cheque volumes are gradually declining due to digital payment alternatives, corporate, government, and regulated financial transactions continue to sustain hardware demand. Banks are upgrading legacy scanners with AI-enabled verification systems and cloud-connected platforms to enhance fraud detection, operational efficiency, and compliance. Growth remains value-driven rather than volume-driven, with rising adoption of high-speed enterprise scanners and software-integrated imaging solutions supporting long-term market expansion.

Key Market Insights

- Banking & financial institutions account for nearly 62% of total demand, driven by regulatory compliance and centralized clearing operations.

- Multi-feed and batch scanners lead the product segment with approximately 38% market share, owing to high-volume processing requirements.

- Image-based RDC technology holds over 41% of the technology segment, reflecting increasing adoption of cloud-connected deposit systems.

- North America dominates with around 34% global share, supported by sustained institutional cheque usage in the U.S.

- Asia-Pacific is the fastest-growing region, led by India’s modernization of cheque truncation infrastructure.

- Top five manufacturers control nearly 54% of global revenue, indicating moderate market consolidation.

What are the latest trends in the cheque scanner market?

AI-Integrated Fraud Detection Systems

Cheque scanner manufacturers are embedding artificial intelligence and machine learning capabilities into scanning platforms to reduce fraud risk and enhance compliance. Advanced imaging algorithms can detect signature mismatches, duplicate cheque deposits, altered fields, and suspicious transaction patterns in real time. Financial institutions are prioritizing fraud prevention due to rising regulatory scrutiny and AML requirements, making AI-enabled scanners a preferred upgrade from legacy hardware. Vendors are increasingly bundling analytics dashboards, automated exception handling, and cloud-based monitoring tools with hardware sales, creating hybrid hardware-software revenue streams.

Cloud-Connected Remote Deposit Capture (RDC)

The shift toward cloud-integrated banking infrastructure is transforming cheque scanner deployment models. Image-based remote deposit capture systems allow branches, corporate offices, and merchants to scan and clear cheques digitally without physical transportation. SaaS-enabled platforms are improving scalability, while API integrations with core banking systems enhance real-time processing. This trend is especially prominent among regional banks and mid-tier financial institutions seeking operational efficiency and cost optimization.

What are the key drivers in the cheque scanner market?

Regulatory Mandates and Cheque Truncation Systems

Governments and central banks in multiple regions have implemented cheque truncation systems to digitize clearing processes and reduce settlement timelines. These mandates require high-resolution imaging standards and secure data capture protocols, prompting banks to upgrade existing equipment. Compliance-driven investments remain one of the strongest growth drivers, particularly in Asia-Pacific and parts of Europe.

Operational Efficiency in Banking Infrastructure

Banks are consolidating branch networks while centralizing back-office operations to reduce costs. High-speed and mid-speed scanners streamline bulk cheque processing, reduce manual errors, and enhance productivity. Automation-focused investments, particularly in North America and Europe, are driving steady replacement demand. The ability to lower operational expenditure while improving accuracy makes cheque scanners a critical component of branch modernization strategies.

What are the restraints for the global market?

Declining Retail Cheque Usage

The continued rise of instant payments, digital wallets, and mobile banking applications is gradually reducing retail cheque transactions, particularly in developed economies. While institutional demand remains stable, the long-term structural decline in consumer cheque usage may cap volume growth in mature markets.

High Capital Investment for Enterprise Systems

High-speed enterprise-grade cheque scanners involve high upfront costs, often ranging between USD 3,000 and USD 10,000 per unit. Smaller financial institutions and cooperative banks in emerging markets may delay upgrades due to capital constraints, limiting penetration in price-sensitive regions.

What are the key opportunities in the cheque scanner industry?

Emerging Market Banking Modernization

Emerging economies in Asia, Africa, and Latin America continue to rely heavily on cheque-based transactions for government payments, SME settlements, and rural banking operations. As these countries modernize clearing systems and introduce cheque truncation standards, demand for cost-effective mid-speed scanners is expected to rise. Vendors offering localized compliance features and competitive pricing models can capture untapped demand.

Subscription-Based Hardware & Software Bundling

Manufacturers are increasingly shifting toward subscription-based models that combine hardware leasing, cloud storage, fraud analytics, and maintenance services. This recurring revenue approach enhances profitability and improves customer retention. Financial institutions benefit from reduced capital expenditure and predictable operating costs, creating a mutually advantageous ecosystem.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1180 Million |

| Market Size in 2026 | USD 1243.72 Million |

| Market Size in 2031 | USD 1617.80 Million |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Multi-feed and batch cheque scanners dominate the product segment, accounting for approximately 38% of global revenue in 2025. Their leadership is primarily driven by large commercial banks and centralized clearing houses that require high-volume processing capabilities to handle corporate and institutional cheque flows. These scanners significantly reduce manual intervention, improve processing accuracy, and enhance operational efficiency, key priorities for banks undergoing branch consolidation and back-office automation. Replacement demand for legacy batch scanners with upgraded AI-enabled imaging systems is further strengthening this segment.

Single-feed scanners maintain consistent demand in small bank branches, credit unions, and merchant locations where daily cheque volumes are moderate. Their affordability and compact design make them suitable for distributed banking networks. Meanwhile, integrated cheque and document scanners are gaining traction in institutions seeking multifunctional devices capable of processing deposit slips, IDs, and compliance documentation alongside cheques. Enterprise-grade networked scanners are expanding in financial hubs where centralized image exchange systems and large-scale treasury operations require seamless connectivity and high throughput performance.

Technology Insights

Image-based Remote Deposit Capture (RDC) technology leads the market with approximately 41% share in 2025, driven by regulatory mandates supporting cheque truncation systems and the shift toward cloud-integrated banking infrastructure. RDC technology eliminates the need for physical cheque transportation, accelerates clearing cycles, and improves liquidity management for financial institutions. Its ability to integrate with core banking systems and digital archival platforms has made it the preferred upgrade path for banks modernizing legacy systems.

MICR-based systems remain foundational for authentication and data extraction but are increasingly enhanced with OCR capabilities and AI-powered fraud analytics. Financial institutions are prioritizing advanced imaging platforms capable of real-time signature verification, duplicate detection, and compliance monitoring. The convergence of hardware with AI-based verification software is enabling manufacturers to move toward higher-margin, value-added offerings.

Throughput Capacity Insights

Mid-speed scanners (51–150 documents per minute) hold nearly 36% of the global market, as they provide an optimal balance between processing capacity and capital investment. Regional banks and mid-sized financial institutions prefer mid-speed models due to their ability to handle growing cheque volumes without the high upfront cost of enterprise-grade high-speed systems. This segment benefits from modernization programs across emerging markets, where banks are upgrading from manual or low-speed systems to automated mid-tier solutions.

High-speed scanners dominate centralized clearing centers in developed economies, particularly in North America and Europe, where corporate cheque volumes remain significant. Low-speed scanners continue to serve decentralized rural branches and small merchant environments, ensuring broad-based demand across deployment scales.

End-Use Insights

Banking and financial institutions remain the largest end-use segment, contributing approximately USD 730 million in 2025 revenue, representing over 60% of total market demand. Growth in this segment is primarily driven by regulatory compliance requirements, fraud risk mitigation, and branch automation strategies. Large commercial banks and credit unions are investing in scanner upgrades to enhance operational resilience and reduce processing turnaround times.

Government and public sector applications are among the fastest-growing segments, expanding at an estimated CAGR above 6%, fueled by digital treasury modernization initiatives and public payment digitization reforms. Tax authorities, municipal bodies, and public disbursement agencies continue to rely on cheque-based transactions in several regions. Retail merchants, utilities, insurance providers, healthcare institutions, and educational organizations are increasingly adopting RDC-enabled scanners to streamline reconciliation processes and accelerate fund availability. Export-driven manufacturing demand remains concentrated in the Asia-Pacific region, which serves as the primary production hub supplying North America and Europe, reinforcing global supply chain integration.

Explore more data points, trends and opportunities Download Free Sample Report

Cheque Scanner Market Segmentations

By Product Type

- Single-Feed Cheque Scanners

- Multi-Feed / Batch Cheque Scanners

- Networked / Enterprise Cheque Scanners

- Integrated Cheque & Document Scanners

By Technology

- MICR-Based Scanners

- OCR-Enhanced Scanners

- Image-Based Remote Deposit Capture (RDC) Scanners

- AI-Enabled Fraud Detection Scanners

By Throughput Capacity

- Low-Speed (Up to 50 DPM)

- Mid-Speed (51–150 DPM)

- High-Speed (Above 150 DPM)

By End-Use Industry

- Banking & Financial Institutions

- Government & Public Sector

- Retail & Large Merchants

- Corporate Enterprises

- Healthcare & Educational Institutions

By Deployment Mode

- On-Premise Systems

- Cloud-Integrated / SaaS-Linked Systems

By Distribution Channel

- Direct Sales (OEM to End User)

- System Integrators

- Banking Technology Vendors

Regional Insights

North America

North America accounts for approximately 34% of the global cheque scanner market in 2025, with the United States alone contributing nearly 28% share. Regional growth is driven by sustained institutional cheque usage in corporate payments, government disbursements, and B2B transactions. The presence of advanced banking infrastructure, early adoption of cheque truncation systems, and continuous replacement of legacy equipment support steady demand. Additionally, strong regulatory enforcement related to AML and fraud prevention is accelerating upgrades toward AI-integrated scanning systems. Canada also contributes a stable demand through credit unions and regional banking networks, emphasizing operational efficiency.

Europe

Europe holds around 26% market share, led by the United Kingdom, Germany, and France. Growth in this region is supported by financial digitization initiatives, cross-border clearing harmonization, and modernization of corporate treasury operations. Although retail cheque usage is declining, corporate and institutional transactions remain resilient. European banks are investing in secure digital archiving systems and compliance-driven imaging upgrades. Additionally, regulatory data protection standards are encouraging the adoption of secure on-premise and hybrid scanning deployments.

Asia-Pacific

Asia-Pacific captures roughly 24% of global revenue and represents the fastest-growing region. India leads regional expansion due to cheque truncation system upgrades and rapid banking digitization initiatives aimed at improving clearing efficiency. China and Japan maintain consistent enterprise-level demand driven by corporate banking and centralized treasury functions. Expanding financial inclusion programs and modernization of state-owned banking institutions across Southeast Asia are further supporting mid-speed scanner adoption. The region’s strong electronics manufacturing base also strengthens its position as a global production and export hub.

Latin America

Latin America accounts for approximately 7% of global revenue, led by Brazil and Mexico. Regional growth is supported by banking sector modernization, SME transaction expansion, and gradual adoption of electronic clearing systems. While digital payments are growing, cheque-based transactions remain relevant in corporate and government sectors. Infrastructure development and regulatory reforms aimed at improving financial transparency are encouraging investments in upgraded imaging solutions.

Middle East & Africa

The Middle East & Africa region represents about 9% of the market, supported by banking infrastructure upgrades in the UAE and South Africa. Growth drivers include financial inclusion initiatives, modernization of public payment systems, and expansion of commercial banking networks. In Gulf Cooperation Council (GCC) countries, high-value corporate transactions continue to utilize cheque instruments, sustaining demand for enterprise-grade scanners. Across Africa, ongoing banking digitization efforts and regulatory improvements are gradually increasing scanner installations, particularly within urban financial centers.

Key Players in the Cheque Scanner Market

- Canon Inc.

- Panini S.p.A.

- Digital Check Corp.

- Epson Corporation

- NCR Corporation

- Burroughs Inc.

- RDM Corporation

- ARCA Technologies

- Kodak Alaris

- MagTek Inc.

- Unisys Corporation

- Glory Ltd.

- Seac Banche S.p.A.

- Bluepoint Solutions

- Parascript LLC