Ceiling Fans Market Size

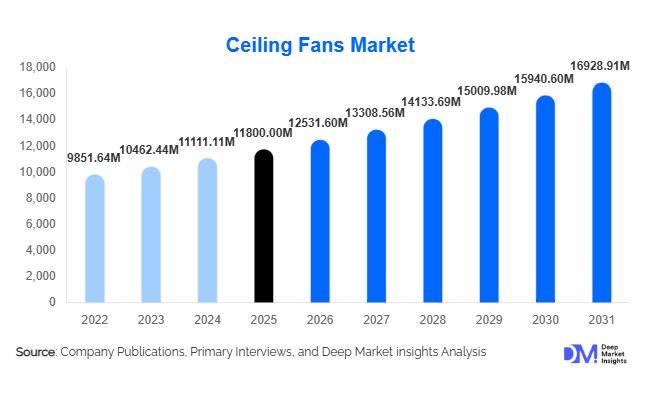

According to Deep Market Insights, the global ceiling fans market size was valued at USD 11,800 million in 2025 and is projected to grow from USD 12,531.60 million in 2026 to reach USD 16,928.91 million by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The ceiling fans market growth is primarily driven by increasing urbanization, rising demand for energy-efficient cooling solutions, and expanding residential and commercial infrastructure across emerging economies. Additionally, the growing adoption of smart and BLDC (Brushless Direct Current) fans, coupled with rising electricity costs, is accelerating the shift toward energy-efficient appliances globally.

Key Market Insights

- Energy-efficient BLDC ceiling fans are gaining strong traction, driven by regulatory policies and rising consumer awareness of electricity savings.

- Asia-Pacific dominates the global market, accounting for nearly 45% of total demand, led by India and Southeast Asia.

- Residential applications remain the largest segment, contributing approximately 65% of total market demand.

- Smart ceiling fans are emerging as a high-growth segment, supported by increasing smart home adoption and IoT integration.

- Offline distribution channels continue to lead, although e-commerce platforms are rapidly expanding in urban markets.

- Industrial HVLS fans are witnessing increased adoption, particularly in warehouses and large commercial spaces.

What are the latest trends in the ceiling fans market?

Shift Toward Energy-Efficient BLDC Technology

The ceiling fans market is undergoing a significant transformation with the growing adoption of BLDC motor technology. These fans consume up to 50–60% less electricity compared to conventional AC motor fans, making them highly attractive in regions with high power tariffs. Governments are also promoting energy-efficient appliances through labeling programs and incentives, accelerating adoption. Manufacturers are increasingly focusing on integrating advanced controllers, remote operation, and inverter compatibility in BLDC fans, enhancing their value proposition. This trend is particularly strong in emerging economies such as India, where large-scale replacement demand exists.

Rising Demand for Smart and Connected Fans

The integration of IoT and smart home technologies is reshaping the ceiling fans market. Consumers are increasingly opting for smart ceiling fans that can be controlled via smartphones, voice assistants, and home automation systems. Features such as scheduling, remote diagnostics, and energy monitoring are becoming standard in premium offerings. This trend is driven by urban consumers seeking convenience, connectivity, and modern aesthetics. Manufacturers are leveraging app-based ecosystems and AI-enabled controls to differentiate their products, making smart fans a rapidly expanding segment within the premium category.

What are the key drivers in the ceiling fans market?

Rapid Urbanization and Housing Development

The expansion of residential construction, particularly in Asia-Pacific, Africa, and Latin America, is a major driver for ceiling fan demand. Government-led housing initiatives and increasing urban population are boosting installations in both new constructions and retrofit projects. Ceiling fans remain a default cooling solution due to their affordability and ease of installation, especially in regions with limited air conditioning penetration.

Growing Focus on Energy Efficiency

Rising electricity costs and environmental concerns are encouraging consumers to adopt energy-efficient appliances. Ceiling fans, particularly BLDC variants, are positioned as cost-effective solutions that significantly reduce energy consumption. Regulatory frameworks promoting energy labeling and efficiency standards are further supporting market growth.

What are the restraints for the global market?

Increasing Penetration of Air Conditioning Systems

The growing affordability and adoption of air conditioners, particularly in urban and high-income regions, pose a challenge to ceiling fan demand. Consumers with higher purchasing power often prefer air conditioning for enhanced cooling comfort, limiting ceiling fan growth in certain segments.

Price Sensitivity in Emerging Markets

A significant portion of consumers in developing economies remains highly price-sensitive, favoring low-cost ceiling fans over energy-efficient or smart variants. This limits the adoption of advanced technologies and slows value growth in the market despite strong volume demand.

What are the key opportunities in the ceiling fans industry?

Expansion of Smart and IoT-Enabled Fans

The increasing adoption of smart home ecosystems presents a strong opportunity for ceiling fan manufacturers. Smart fans integrated with voice assistants and mobile applications are gaining popularity among urban consumers. This segment offers higher margins and differentiation opportunities, encouraging companies to invest in innovation and connectivity features.

Infrastructure Growth in Emerging Economies

Rapid urbanization and government-led housing projects in regions such as Southeast Asia, Africa, and the Middle East are creating significant demand for ceiling fans. Expanding electrification and rising disposable incomes are further boosting adoption, making these regions key growth markets for manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11800 Million |

| Market Size in 2026 | USD 12531.60 Million |

| Market Size in 2031 | USD 16928.91 Million |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Standard AC motor ceiling fans continue to dominate the global market, accounting for approximately 55% of total demand in 2025. This leadership is primarily driven by their affordability, simple technology, and widespread availability across developing economies where price sensitivity remains high. These fans are deeply entrenched in markets such as India, Southeast Asia, and Africa due to strong distribution networks and low upfront costs. However, the market is gradually shifting toward energy-efficient BLDC fans, which currently account for nearly 18% share but are growing at the fastest pace. The key driver for this segment is the rising cost of electricity combined with government-led energy efficiency programs and labeling regulations. BLDC fans offer up to 60% energy savings, making them increasingly attractive for both residential and commercial users.

Meanwhile, premium and decorative ceiling fans are gaining traction in urban and developed markets, where consumers prioritize aesthetics, noiseless operation, and smart features. This segment is being driven by rising disposable incomes and evolving interior design trends. Additionally, industrial HVLS (High Volume Low Speed) fans, though currently niche, are witnessing strong growth due to increasing demand from warehouses, logistics hubs, and manufacturing facilities. Their ability to provide efficient air circulation over large spaces with lower energy consumption is a key factor supporting their adoption.

Application Insights

Indoor ceiling fans dominate the application segment, contributing over 85% of total market demand in 2025. Their dominance is driven by their essential role in residential homes, offices, and retail spaces, particularly in regions with warm climates and limited air conditioning penetration. The key growth driver for indoor fans is the continuous expansion of residential construction and renovation activities globally, especially in emerging economies where ceiling fans remain a default cooling solution.

On the other hand, outdoor ceiling fans are emerging as a growing niche segment, driven by the expansion of hospitality infrastructure such as resorts, restaurants, and cafes with open-air seating. These fans are designed to withstand moisture, humidity, and dust, making them suitable for patios and semi-open environments. The increasing trend of outdoor living spaces in developed markets such as North America and Europe is further supporting demand for this segment.

Distribution Channel Insights

Offline distribution channels dominate the ceiling fans market, accounting for approximately 70% of total sales. This dominance is driven by well-established dealer and distributor networks, particularly in emerging markets where consumers prefer physical inspection, installation support, and after-sales service. Electrical retail stores and specialty appliance outlets continue to play a crucial role in influencing purchase decisions, especially in rural and semi-urban areas.

However, online distribution channels are witnessing rapid growth, particularly in urban regions. The key driver for this shift is increasing digital penetration, rising consumer trust in e-commerce platforms, and the availability of competitive pricing and wider product selection. Direct-to-consumer (D2C) brand websites are also gaining traction, as manufacturers invest in digital marketing, faster delivery logistics, and exclusive online product offerings. This hybrid distribution model is expected to reshape market dynamics over the coming years.

End-Use Insights

The residential segment leads the ceiling fans market, contributing approximately 65% of total demand in 2025. This dominance is driven by high household penetration, continuous replacement cycles, and strong demand from new housing developments. The primary growth driver is rapid urbanization and government-supported housing schemes, particularly in Asia-Pacific and Africa, where ceiling fans are considered essential household appliances.

The commercial segment, including offices, retail spaces, and hospitality establishments, is experiencing steady growth. Increasing infrastructure development and the need for cost-effective air circulation solutions are key drivers in this segment. Meanwhile, the industrial segment is emerging as a high-growth area, driven by the adoption of HVLS fans in warehouses, factories, and logistics centers. The rapid expansion of the global e-commerce and supply chain industry is significantly boosting demand for large-scale air circulation solutions in industrial environments.

Explore more data points, trends and opportunities Download Free Sample Report

Ceiling Fans Market Segmentations

By Product Type

- Standard AC Motor Ceiling Fans

- Energy-Efficient BLDC Ceiling Fans

- Premium & Decorative Ceiling Fans

- Smart/IoT-Enabled Ceiling Fans

- Industrial HVLS Ceiling Fans

By Application

- Indoor Ceiling Fans

- Outdoor Ceiling Fans

By Distribution Channel

- Offline Retail

- Online Retail

By End-Use

- Residential

- Commercial

- Industrial

By Technology

- AC Motor Technology

- BLDC Technology

- Smart Connected Systems

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global ceiling fans market, accounting for approximately 45% of total demand in 2025. India alone contributes nearly 20% of global demand, making it the largest country market, driven by high household penetration, strong domestic manufacturing, and favorable climatic conditions. China and Southeast Asian countries such as Indonesia, Vietnam, and Thailand are also major contributors due to rapid urbanization and infrastructure growth. The key drivers for regional growth include expanding electrification, rising middle-class population, increasing housing construction, and government initiatives promoting energy-efficient appliances. Additionally, the presence of large-scale manufacturing hubs in the region supports both domestic consumption and exports.

North America

North America holds around 15% of the global market share, with the United States being the primary contributor. The market in this region is largely replacement-driven, with consumers upgrading to energy-efficient and smart ceiling fans. Key growth drivers include increasing adoption of smart home technologies, rising demand for premium and decorative fans, and the trend toward outdoor living spaces. Additionally, energy efficiency regulations and sustainability awareness are encouraging the replacement of older models with advanced BLDC and IoT-enabled fans.

Europe

Europe accounts for approximately 12% of the global market, led by countries such as Germany, the United Kingdom, France, Italy, and Spain. The market is relatively mature, with growth primarily driven by replacement demand and premiumization. Key drivers include stringent energy efficiency regulations, increasing focus on sustainable appliances, and rising consumer preference for aesthetically designed ceiling fans. The growing popularity of smart home systems is also contributing to the adoption of connected ceiling fans across urban households.

Middle East & Africa

The Middle East and Africa region contributes around 10% of global demand and is among the fastest-growing markets. Countries such as Saudi Arabia, the UAE, South Africa, and Nigeria are key contributors. The primary growth drivers include hot climatic conditions, increasing electrification in rural areas, and rapid infrastructure development. In many parts of Africa, ceiling fans serve as an affordable alternative to air conditioning, driving strong demand. Additionally, government investments in housing and commercial infrastructure are further supporting market expansion.

Latin America

Latin America holds approximately 8% of the global market, with Brazil and Mexico leading regional demand. The market is driven by favorable climatic conditions, increasing residential construction, and rising urbanization. Key growth drivers include improving economic conditions, expansion of the middle-class population, and growing demand for affordable cooling solutions. The region is also witnessing the gradual adoption of energy-efficient and decorative ceiling fans, particularly in urban centers, supporting steady market growth.

Key Players in the Ceiling Fans Market

- Crompton Greaves Consumer Electricals

- Orient Electric

- Havells India

- Usha International

- Bajaj Electricals

- Panasonic Corporation

- Hunter Fan Company

- Minka Group

- Emerson Electric

- Luminance Brands

- Big Ass Fans

- Westinghouse Electric Corporation

- Shell Electric Holdings

- V-Guard Industries

- Atomberg Technologies