Cat Litter Market Size

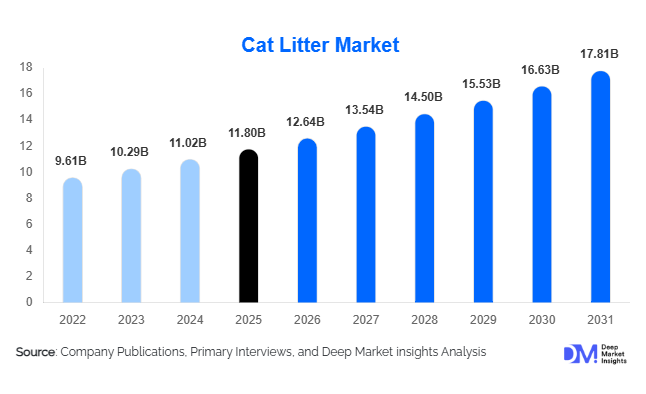

According to Deep Market Insights, the global cat litter market size was valued at USD 11.8 billion in 2025 and is projected to grow from USD 12.64 billion in 2026 to reach USD 17.81 billion by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The cat litter market growth is primarily driven by rising global cat ownership, increasing pet humanization trends, rapid urbanization, and growing demand for premium, odor-control, and eco-friendly litter solutions across developed and emerging economies.

Key Market Insights

- Clay-based cat litter continues to dominate globally, primarily due to its low cost, strong clumping ability, and widespread availability across retail channels.

- Biodegradable litter is the fastest-growing segment, driven by environmental concerns and regulatory pressure to reduce non-biodegradable waste.

- North America leads global demand, supported by high pet ownership rates and strong penetration of premium pet care products.

- Asia-Pacific is the fastest-growing region, driven by rising disposable income, urban pet adoption, and increasing awareness of pet hygiene.

- E-commerce channels are expanding rapidly, reshaping purchasing behavior through subscription models and doorstep delivery convenience.

- Premiumization is reshaping the industry, with consumers increasingly opting for silica gel, odor-control, and low-dust formulations.

What are the latest trends in the cat litter market?

Shift Toward Sustainable and Biodegradable Litter

The market is witnessing a strong shift toward eco-friendly litter products made from wood, paper, corn, wheat, and coconut-based materials. Consumers are increasingly concerned about environmental degradation caused by traditional clay mining and landfill waste accumulation. As a result, biodegradable litter products are gaining traction, particularly in Europe and North America, where sustainability regulations are more stringent. Manufacturers are investing in compostable formulations, renewable raw materials, and plastic-free packaging to meet evolving consumer expectations. This trend is also encouraging premium pricing strategies, as eco-friendly products are positioned as healthier and safer alternatives for both pets and the environment.

Premiumization and Smart Product Innovation

Cat owners are increasingly willing to pay for advanced litter solutions that offer enhanced odor control, dust reduction, and antimicrobial properties. Silica gel and crystal litter products are gaining popularity due to their superior moisture absorption and longer usability cycles. Additionally, innovation in lightweight formulations is reducing transportation costs and improving convenience for consumers. Smart pet care integration is also emerging, with automated litter boxes and sensor-based odor management systems gaining traction in urban households. Subscription-based delivery models are further strengthening customer retention and enabling predictable revenue streams for manufacturers and retailers.

What are the key drivers in the cat litter market?

Rising Global Cat Ownership

One of the strongest growth drivers is the steady increase in cat adoption globally, particularly in urban apartments where cats are preferred due to their low maintenance requirements. Rising nuclear households, delayed family formation, and lifestyle changes are contributing to higher pet ownership rates. This has a direct impact on cat litter consumption volumes, as litter is an essential recurring purchase. Emerging economies such as India, China, and Brazil are witnessing accelerated adoption rates, further expanding the global customer base.

Pet Humanization and Premium Spending

Pet owners are increasingly treating pets as family members, driving higher spending on hygiene and wellness products. This shift has significantly boosted demand for premium litter products that offer better odor control, hygiene, and convenience. Consumers are prioritizing quality over cost, especially in developed markets, leading to strong growth in silica gel and biodegradable litter segments. This trend is also encouraging brand differentiation and innovation in packaging, scent control, and sustainability features.

Expansion of E-Commerce and Subscription Models

The rapid growth of online retail has transformed the distribution landscape of the cat litter market. E-commerce platforms offer convenience, product variety, and competitive pricing, making them increasingly popular among pet owners. Subscription-based models are particularly impactful, ensuring recurring purchases and stable demand cycles. This shift is also enabling smaller and niche brands to compete effectively with established players by directly reaching consumers without heavy reliance on traditional retail infrastructure.

What are the restraints for the global market?

Environmental Concerns of Clay-Based Products

Traditional clay-based litter, despite its dominance, faces growing scrutiny due to environmental concerns associated with strip mining and non-biodegradable waste. Regulatory pressure in several regions, particularly Europe, is pushing manufacturers to reduce dependence on clay-based products. This transition creates cost and supply chain challenges for established producers, especially those reliant on large-scale mining operations.

Price Sensitivity in Emerging Markets

While premium litter products are growing in developed economies, price sensitivity remains a significant barrier in developing regions. Consumers in cost-conscious markets often prefer low-cost clay-based options, limiting the adoption of high-margin biodegradable or silica-based alternatives. This imbalance restricts overall market value expansion and slows the transition toward sustainable product categories in price-sensitive geographies.

What are the key opportunities in the cat litter industry?

Expansion of Biodegradable Product Lines

The growing demand for sustainable pet care products presents a major opportunity for manufacturers to expand biodegradable litter offerings. Companies investing in plant-based raw materials and compostable formulations can capture environmentally conscious consumers, especially in North America and Europe. This segment also allows for premium pricing and improved brand positioning in a sustainability-driven market environment.

Growth in Emerging Markets

Rapid urbanization and rising disposable incomes in the Asia-Pacific and Latin America are creating strong growth opportunities. Countries such as China, India, and Brazil are witnessing increasing pet adoption rates, but remain underpenetrated compared to developed markets. Localized production, affordable pricing strategies, and distribution expansion can enable companies to establish early leadership in these high-growth regions.

Innovation in Smart and Value-Added Solutions

Technological integration presents a significant opportunity, with innovations such as odor-control crystals, antimicrobial additives, and smart litter monitoring systems gaining traction. Automated litter boxes and subscription-based refill models are also expanding the market scope beyond traditional product sales. These innovations improve convenience and hygiene while creating new revenue streams for manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.8 Billion |

| Market Size in 2026 | USD 12.64 Billion |

| Market Size in 2031 | USD 17.81 Billion |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Clay-based litter continues to dominate the global cat litter market, accounting for approximately 62% of total market share in 2025. The leadership of this segment is primarily driven by its cost-effectiveness, widespread availability, and strong clumping properties, which make it highly suitable for mass-market adoption across both developed and emerging economies. Sodium bentonite-based clumping clay, in particular, remains the most preferred variant due to its superior moisture absorption and ease of cleaning, making it a staple choice among households with multiple cats. Within product formats, clumping litter leads with around 58% share, supported by its convenience, odor control efficiency, and reduced maintenance requirements. This segment continues to benefit from consumer preference for hygiene and time-saving solutions, especially among urban pet owners. Silica gel litter is gaining significant traction in the premium segment due to its high absorbency, low dust generation, and longer usage cycles, making it attractive for consumers seeking high-performance solutions despite higher costs.

Biodegradable litter is emerging as the fastest-growing segment, supported by increasing environmental awareness, regulatory pressures, and consumer inclination toward sustainable pet care products. Materials such as wood, corn, and paper are gaining popularity, particularly in Europe and North America. Additionally, crystal and pellet formats are expanding in niche and premium applications, driven by their lightweight nature, low tracking properties, and suitability for automated litter systems. Overall, innovation and sustainability are reshaping product preferences across segments.

Distribution Channel Insights

Offline retail remains the dominant distribution channel, contributing approximately 65% of the global market share in 2025. This dominance is driven by the strong presence of supermarkets, hypermarkets, pet specialty stores, and veterinary clinics, where consumers prefer to physically evaluate product quality, weight, and packaging before purchase. Established retail networks and brand visibility in physical stores continue to reinforce this segment’s leadership globally. However, online retail is the fastest-growing channel, driven by increasing digital adoption, convenience, and the availability of subscription-based delivery models. E-commerce platforms provide a broader product assortment, competitive pricing, and customer reviews, enabling informed purchasing decisions. The rise of direct-to-consumer (D2C) brands is further disrupting traditional retail dynamics, allowing manufacturers to engage directly with consumers and build brand loyalty.

Additionally, digital marketing strategies, influencer promotions, and targeted advertising are accelerating online sales, particularly among younger and urban consumers. Subscription services are proving especially impactful, ensuring recurring demand and reducing the burden of frequent repurchasing for consumers. This shift toward omnichannel distribution is expected to redefine the competitive landscape in the coming years.

End-Use Insights

Household pet owners represent the largest end-use segment, accounting for the majority of global demand, driven by the continuous rise in cat ownership and increasing focus on pet hygiene and well-being. This segment’s dominance is reinforced by the recurring nature of litter consumption, making it an essential and non-discretionary product for pet owners worldwide.

Within this category, multi-cat households are emerging as a high-growth segment, as they consume higher volumes of litter and exhibit a stronger preference for premium, odor-control, and low-dust products. These households are more likely to adopt advanced litter solutions, including clumping and silica-based products, to manage hygiene effectively. Institutional demand from veterinary clinics, pet shelters, and boarding facilities is also growing steadily, contributing to bulk purchasing and stable demand cycles. Furthermore, the broader global pet care industry, expanding at over 6–7% annually, continues to support long-term growth in the cat litter market. Emerging applications, such as automated litter systems and smart pet care solutions, are also creating new demand avenues, particularly in urban and tech-savvy consumer segments.

Explore more data points, trends and opportunities Download Free Sample Report

Cat Litter Market Segmentations

By Product Composition

- Clay-Based Cat Litter

- Silica Gel Cat Litter

- Biodegradable Cat Litter

By Product Format

- Clumping Cat Litter

- Non-Clumping Cat Litter

- Crystal Cat Litter

- Pellet Cat Litter

By Distribution Channel

- Offline Retail

- Online Retail

By Price Tier

- Economy

- Mid-Range

- Premium

Regional Insights

North America

North America leads the global cat litter market, accounting for approximately 38% of the total market share in 2025. The United States is the primary contributor, driven by high pet ownership rates, strong consumer spending on pet care, and widespread adoption of premium litter products such as silica gel and advanced clumping variants. Canada also contributes significantly, supported by similar consumption patterns and a high awareness of pet hygiene. Key growth drivers in this region include the increasing trend of pet humanization, rising demand for convenience-driven products, and strong penetration of e-commerce and subscription-based purchasing models. Additionally, innovation in odor-control technologies and sustainable packaging solutions is further accelerating market expansion. The presence of leading global manufacturers and well-established distribution networks also strengthens regional dominance.

Europe

Europe holds around 27% of the global market share, with major demand coming from Germany, the United Kingdom, and France. The region is characterized by a strong shift toward sustainable and eco-friendly litter products, driven by stringent environmental regulations and high consumer awareness regarding sustainability. Growth in Europe is primarily driven by increasing adoption of biodegradable litter, government regulations on waste management, and consumer preference for premium, low-dust, and chemical-free products. Additionally, urbanization and rising pet ownership across Western and Northern Europe are supporting steady demand. The region also benefits from well-developed retail infrastructure and growing online sales channels.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the global cat litter market, with a projected CAGR exceeding 9%. China, Japan, and India are the key markets driving regional growth. China dominates in terms of volume demand due to rapid urbanization, increasing disposable incomes, and a surge in pet adoption among younger populations. Japan represents a mature market with strong demand for premium, compact, and high-performance litter products, driven by space constraints and high hygiene standards. India is emerging as a high-growth market due to rising awareness of pet care, an expanding middle-class population, and increasing availability of affordable litter products. Key drivers in the region include urban lifestyle changes, growth of nuclear families, expansion of e-commerce platforms, and increasing influence of Western pet care practices. Local manufacturing expansion and competitive pricing strategies are further accelerating market penetration.

Latin America

Latin America is experiencing steady growth, led by Brazil and Mexico, which are the largest markets in the region. Rising middle-class populations, increasing pet ownership, and urbanization are the primary factors driving demand. The market is currently dominated by affordable clay-based litter products, reflecting price sensitivity among consumers. However, premium and biodegradable segments are gradually gaining traction in urban centers, supported by increasing consumer awareness and improving economic conditions. Expansion of modern retail formats and growing e-commerce penetration are also contributing to market growth in the region.

Middle East & Africa

The Middle East & Africa region represents a relatively nascent but growing market for cat litter, with demand concentrated in urban areas such as the UAE and South Africa. Increasing disposable incomes, changing lifestyles, and rising pet adoption are key factors supporting market expansion. Growth in this region is further driven by the increasing availability of premium imported products, the expansion of pet specialty retail stores, and growing awareness of pet hygiene. While the market remains smaller compared to other regions, it presents significant long-term growth potential, particularly as urbanization and pet ownership continue to rise.

Key Players in the Cat Litter Market

- Nestlé Purina PetCare

- Mars Petcare

- Church & Dwight Co., Inc.

- Clorox Company

- Oil-Dri Corporation of America

- Dr. Elsey’s

- Intersand Group

- Healthy Pet

- Pettex Limited

- Pioneer Pet