Cashmere Clothing Market Size

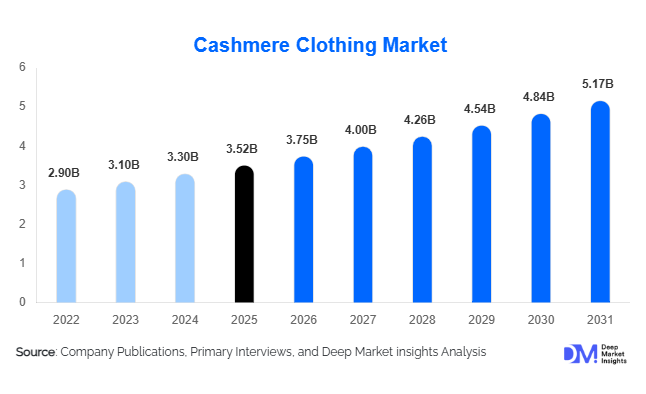

According to Deep Market Insights, the global cashmere clothing market size was valued at USD 3.52 billion in 2025 and is projected to grow from USD 3.74 billion in 2026 to reach USD 5.18 billion by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The cashmere clothing market growth is primarily driven by rising consumer demand for premium apparel, increasing preference for sustainable natural fibers, and expanding luxury fashion consumption across emerging economies. Growing awareness regarding durable and high-quality garments, combined with the rapid expansion of digital luxury retail platforms, is further supporting market expansion globally.

Key Market Insights

- Luxury and premium knitwear demand is accelerating globally, driven by consumer preference for timeless, durable, and high-quality apparel.

- Sustainable and traceable cashmere sourcing is becoming a major purchasing criterion, particularly among younger and environmentally conscious consumers.

- Europe dominates the global market, supported by the presence of luxury fashion houses and premium textile manufacturers.

- Asia-Pacific is the fastest-growing regional market, driven by rising disposable income and expanding luxury consumption in China, India, Japan, and South Korea.

- E-commerce and direct-to-consumer retail models are reshaping the industry, enabling brands to improve customer reach and profitability.

- Technological innovations in recycled cashmere and fiber blending are improving affordability and sustainability across the premium apparel industry.

Cashmere Clothing Market Trends

Sustainable and Traceable Cashmere Gaining Momentum

Sustainability has emerged as one of the most important trends in the global cashmere clothing market. Consumers are increasingly demanding transparency regarding sourcing practices, animal welfare standards, and environmental impact. Luxury brands are investing heavily in blockchain-enabled traceability systems, regenerative grazing programs, and ethical sourcing partnerships across Mongolia and Inner Mongolia. Recycled cashmere collections are also expanding rapidly as brands seek to reduce raw material dependency and appeal to environmentally conscious consumers. Several premium fashion companies are additionally launching carbon-neutral production initiatives and introducing sustainability certifications to strengthen brand positioning within the luxury apparel industry.

Digital Luxury Retail and Personalization Expanding Rapidly

Luxury apparel brands are increasingly adopting advanced digital commerce strategies to improve customer engagement and sales conversion. Artificial intelligence-powered personalization, virtual fitting rooms, predictive fashion recommendations, and omni-channel retail integration are becoming standard across premium cashmere retail platforms. Younger consumers are driving online luxury purchases, particularly across Asia-Pacific and North America. Brands are additionally leveraging influencer marketing, social commerce, and direct-to-consumer business models to strengthen customer loyalty and improve margins. The rapid expansion of luxury e-commerce is significantly increasing accessibility to premium cashmere products across tier-2 and tier-3 cities globally.

Cashmere Clothing Market Drivers

Growing Premiumization in Fashion Consumption

Consumers globally are increasingly prioritizing quality, exclusivity, and durability over low-cost fast-fashion products. Cashmere apparel aligns strongly with this trend due to its premium texture, lightweight insulation, and luxury positioning. Rising disposable incomes among affluent and upper-middle-class consumers are supporting increased spending on premium knitwear, coats, scarves, and winter apparel. Luxury fashion brands are continuously expanding their product portfolios to cater to growing demand for high-end lifestyle fashion. Premiumization trends are particularly strong across Europe, North America, China, Japan, and South Korea.

Rising Demand for Sustainable Natural Fibers

Global consumers are increasingly seeking sustainable alternatives to synthetic textiles, benefiting natural fibers such as cashmere. The fashion industry is experiencing significant pressure to reduce environmental impact, and cashmere is increasingly positioned as a premium eco-friendly fiber when responsibly sourced. Luxury brands are investing heavily in sustainable grazing systems, recycled fiber technologies, and ethical supply-chain management. Consumer preference for long-lasting garments with lower environmental impact is expected to support long-term market growth.

Cashmere Clothing Market Restraints

Volatility in Raw Cashmere Prices

The global cashmere industry remains highly dependent on raw fiber production concentrated in Mongolia and China. Climate variability, livestock diseases, overgrazing concerns, and geopolitical trade fluctuations frequently impact raw cashmere supply and pricing. Rising raw material costs significantly affect profit margins for apparel manufacturers and contribute to higher retail prices for consumers. Smaller and mid-sized brands are particularly vulnerable to price volatility due to limited sourcing flexibility and weaker supplier bargaining power.

Counterfeit and Low-Quality Imitation Products

The increasing availability of counterfeit cashmere apparel products remains a major challenge for premium brands. Many low-cost products marketed as cashmere contain high proportions of synthetic fibers, reducing consumer trust and impacting brand reputation. The presence of imitation products intensifies pricing pressure and creates quality inconsistencies within the broader market. Luxury brands are therefore investing in product authentication systems, advanced labeling technologies, and supply-chain transparency initiatives to maintain brand integrity and consumer confidence.

Cashmere Clothing Market Opportunities

Expansion of Affordable Luxury Cashmere

The growing popularity of affordable luxury fashion presents significant opportunities for market expansion. Younger consumers increasingly aspire to own premium apparel products but remain price-sensitive. Brands introducing blended cashmere, recycled cashmere, and lightweight knitwear collections are successfully attracting broader customer groups. Affordable luxury positioning is particularly effective in emerging markets where rising middle-class populations are increasing discretionary spending on fashion and lifestyle products. Digital-first cashmere brands are additionally leveraging direct-to-consumer retail models to reduce distribution costs and improve affordability.

Growth of Sustainable and Recycled Cashmere Solutions

Innovations in recycled cashmere technologies are creating major opportunities across the luxury apparel industry. Recycled cashmere products help brands reduce raw material dependency while improving sustainability performance. Companies investing in circular textile manufacturing, fiber recovery systems, and eco-friendly production technologies are expected to gain strong competitive advantages. Consumers increasingly value sustainability certifications and traceable sourcing, creating opportunities for brands that can demonstrate ethical manufacturing and environmental responsibility. This trend is expected to accelerate long-term adoption of recycled and blended cashmere apparel globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.52 Billion |

| Market Size in 2026 | USD 3.75 Billion |

| Market Size in 2031 | USD 5.17 Billion |

| CAGR | 6.60% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Sweaters represent the largest product category within the cashmere clothing market, accounting for approximately 42% of global revenue in 2025. Demand remains particularly strong for pullovers, turtlenecks, cardigans, and lightweight all-season knitwear. Consumers increasingly prefer versatile premium sweaters suitable for both casual and formal wear. Coats and outerwear also represent a significant segment due to rising luxury winterwear demand across North America and Europe. Scarves and wraps continue gaining popularity as premium gifting products, while loungewear and athleisure cashmere apparel are emerging rapidly as lifestyle fashion trends evolve toward comfort-oriented luxury clothing.

Fiber Type Insights

Pure cashmere apparel dominates the market with nearly 55% share globally, supported by strong consumer preference for ultra-soft, premium-quality garments. Luxury fashion houses continue to prioritize 100% cashmere collections to strengthen exclusivity and premium brand positioning. Blended cashmere products are witnessing rapid growth due to improved affordability and durability. Cashmere-silk and cashmere-cotton blends are increasingly popular among younger consumers seeking lightweight luxury apparel suitable for year-round use. Recycled cashmere is additionally emerging as one of the fastest-growing fiber categories due to sustainability-driven purchasing behavior.

Distribution Channel Insights

Offline retail channels, including luxury boutiques, department stores, and brand-owned retail outlets, continue to dominate the cashmere clothing market with nearly 60% revenue share in 2025. Consumers frequently prefer physical retail experiences when purchasing premium apparel to assess texture, softness, and garment quality directly. However, online retail channels are experiencing the fastest growth due to rising luxury e-commerce adoption and increasing digital engagement among younger consumers. Direct-to-consumer platforms are helping brands improve margins while strengthening customer loyalty through personalization, exclusive collections, and seamless omni-channel experiences.

Consumer Group Insights

Women represent the largest consumer segment in the global cashmere clothing market, accounting for nearly 58% of total demand in 2025. The segment benefits from extensive product diversity across sweaters, dresses, scarves, wraps, and winter fashion collections. Men’s cashmere apparel is also witnessing strong growth due to increasing acceptance of premium knitwear and luxury casual fashion. Demand for children’s cashmere clothing remains niche but is expanding gradually among affluent consumers seeking premium comfort-focused apparel for infants and young children.

Price Positioning Insights

Premium luxury and ultra-luxury cashmere apparel continue to dominate market revenues due to strong brand loyalty and high profit margins. Consumers purchasing within these segments prioritize craftsmanship, exclusivity, and heritage brand value. Affordable luxury cashmere products are emerging as the fastest-growing segment globally, supported by digital-first brands introducing lower-cost blended cashmere collections. Mid-range premium fashion brands are increasingly targeting aspirational consumers through online channels and seasonal product launches designed to balance affordability with premium quality.

Explore more data points, trends and opportunities Download Free Sample Report

Cashmere Clothing Market Segmentations

By Product Type

- Sweaters

- Coats & Outerwear

- Bottom Wear

- Tops & Casualwear

- Dresses & Skirts

- Scarves & Wrap Apparel

- Sleepwear & Loungewear

- Active & Athleisure Cashmere Wear

- Baby & Kids Cashmere Clothing

- Customized & Bespoke Cashmere Apparel

By Fiber Type

- Pure Cashmere

- Ultra-Fine Cashmere

- Blended Cashmere

- Organic & Sustainable Cashmere

- Recycled Cashmere

By Consumer Group

- Women

- Men

- Children & Infants

- Unisex Fashion

By Distribution Channel

- Brand-Owned Retail Stores

- Department Stores

- Luxury Boutiques

- Factory Outlets

- E-commerce Marketplaces

- Brand-Owned Online Stores

- Omni-Channel Retail

- Duty-Free & Travel Retail

By Price Positioning

- Ultra-Luxury

- Premium Luxury

- Affordable Luxury

- Mid-Range Fashion Cashmere

- Entry-Level Mass Premium

Regional Insights

North America

North America accounts for approximately 25% of the global cashmere clothing market, led primarily by the United States. High discretionary spending, strong luxury retail infrastructure, and growing online premium apparel purchases continue to support market growth. Consumers increasingly prefer sustainable luxury fashion, driving demand for ethically sourced and traceable cashmere garments. Canada additionally contributes through strong winterwear demand and premium outerwear consumption. The region also benefits from rapid adoption of digital luxury commerce platforms and direct-to-consumer retail models.

Europe

Europe remains the largest regional market, accounting for nearly 38% of global revenue in 2025. Italy, France, Germany, and the United Kingdom dominate regional demand due to their strong luxury fashion ecosystems and established premium textile industries. Italy serves as a major manufacturing and export hub for luxury cashmere apparel, supported by advanced craftsmanship and vertically integrated supply chains. European consumers strongly prioritize sustainability, quality, and timeless fashion, reinforcing long-term demand for premium cashmere garments.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market for cashmere clothing. China plays a dual role as both a leading producer of raw cashmere and a rapidly expanding luxury apparel consumer market. Rising upper-middle-class populations, increasing fashion consciousness, and rapid luxury e-commerce growth are driving demand across China, Japan, South Korea, and India. Younger consumers are increasingly purchasing premium knitwear and affordable luxury cashmere products through digital retail platforms. Expanding premium retail infrastructure and rising urban disposable incomes are expected to accelerate regional market growth further.

Latin America

Latin America represents a relatively smaller but steadily growing market for premium cashmere apparel. Brazil and Mexico are witnessing increasing luxury fashion consumption among affluent urban consumers. Rising exposure to global luxury brands and expanding online premium retail availability are supporting market penetration. Demand remains concentrated within premium sweaters, scarves, and winterwear categories, particularly among high-income consumers seeking imported luxury fashion products.

Middle East & Africa

The Middle East & Africa region is emerging as an important luxury apparel growth market, led by the UAE and Saudi Arabia. Affluent consumer populations, luxury retail expansion, and tourism-driven shopping activity are supporting demand for premium cashmere garments. Dubai and Abu Dhabi continue to strengthen their position as global luxury shopping destinations. South Africa additionally contributes through growing premium apparel consumption among upper-income urban consumers. Increasing luxury mall developments and international brand expansion are expected to accelerate regional market demand over the forecast period.

Key Players in the Cashmere Clothing Market

- Brunello Cucinelli S.p.A.

- Loro Piana S.p.A.

- Ermenegildo Zegna Group

- Pringle of Scotland

- Malo Cashmere

- Autumn Cashmere

- Barrie Knitwear

- Gobi Cashmere

- N.Peal

- SofiaCashmere

- White + Warren

- Falconeri

- Repeat Cashmere

- Johnston of Elgin

- TSE Cashmere