Carpet Market Size

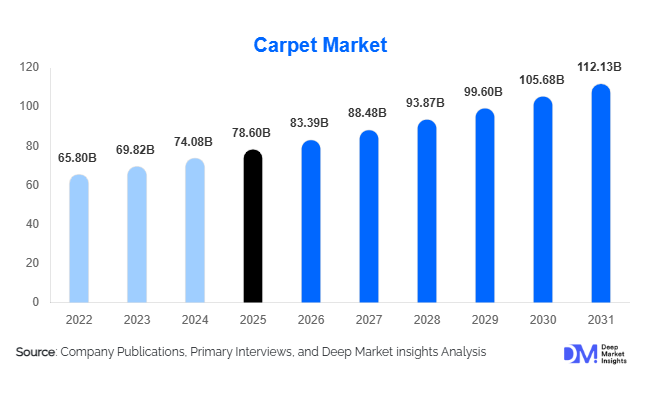

According to Deep Market Insights, the global carpet market size was valued at USD 78.6 billion in 2025 and is projected to grow from USD 83.39 billion in 2026 to reach USD 112.13 billion by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). The market growth is primarily driven by rising residential construction activity, increasing commercial infrastructure investments, rapid urbanization, and growing consumer spending on interior décor and premium flooring solutions. Carpets continue to witness strong adoption across residential, hospitality, corporate, retail, healthcare, and transportation applications due to their acoustic insulation, thermal comfort, aesthetic appeal, and ease of customization.

The market is undergoing a significant transformation with the increasing penetration of sustainable and recyclable flooring products. Manufacturers are investing heavily in eco-friendly fibers, low-VOC materials, digital printing technologies, and modular carpet systems to align with changing consumer preferences and regulatory standards. Demand for carpet tiles is expanding rapidly across commercial spaces owing to their flexibility, lower maintenance costs, and ease of replacement. In addition, rising adoption of smart manufacturing technologies and automation is improving operational efficiency and enabling greater product customization.

Asia-Pacific dominates the global carpet market due to large-scale construction activity and expanding middle-class consumer demand in China and India, while North America and Europe continue to generate strong replacement demand driven by renovation and remodeling trends. Increasing investments in hospitality infrastructure, airports, offices, educational institutions, and public infrastructure projects are further supporting long-term market expansion globally.

Key Market Insights

- Sustainable and recyclable carpets are gaining significant traction, particularly across commercial and institutional construction projects driven by green building regulations.

- Carpet tiles and modular flooring systems are witnessing rapid adoption in corporate offices, educational institutions, airports, and hospitality infrastructure due to flexibility and lower lifecycle costs.

- Asia-Pacific dominates the global carpet market, led by strong construction growth, urbanization, and rising residential flooring demand in China and India.

- North America remains a major premium carpet market, supported by renovation spending, home improvement trends, and strong demand for luxury interior décor products.

- Commercial applications are expanding faster than residential demand, particularly across hospitality, healthcare, retail, and co-working office infrastructure.

- Technological advancements, including digital carpet printing, stain-resistant coatings, antimicrobial treatments, and robotic tufting systems, are transforming manufacturing efficiency and product innovation.

Carpet Market Trends

Sustainable and Recyclable Carpets Becoming Mainstream

Sustainability has become one of the defining trends within the global carpet market. Manufacturers are increasingly focusing on recycled nylon, PET-based fibers, bio-based polymers, and closed-loop recycling systems to reduce environmental impact. Commercial developers and institutional buyers are prioritizing carpets with low volatile organic compound (VOC) emissions and green certifications such as LEED and BREEAM. The growing emphasis on circular economy practices is encouraging carpet producers to introduce take-back and recycling programs that improve product lifecycle sustainability. Major commercial projects in Europe and North America are increasingly mandating recyclable flooring materials, further accelerating adoption. Additionally, consumer awareness regarding eco-friendly home interiors is positively influencing demand for natural fiber carpets such as wool, jute, and sisal.

Rapid Growth of Modular Carpet Tiles

Carpet tiles are emerging as one of the fastest-growing product categories globally, particularly across offices, educational institutions, healthcare facilities, airports, and hospitality infrastructure. Modular carpet systems offer operational advantages such as easier installation, selective replacement, reduced maintenance costs, and design flexibility. Corporate offices are increasingly adopting carpet tiles to support dynamic workspace configurations and improve acoustic insulation within collaborative work environments. Hospitality operators are also investing in customized modular flooring solutions to enhance aesthetics while minimizing operational disruptions during renovations. Technological advancements in digital printing and automated tufting are enabling manufacturers to introduce highly customized carpet tile collections tailored for premium commercial applications. The expansion of smart buildings and co-working infrastructure globally is expected to further strengthen demand for modular flooring systems over the forecast period.

Carpet Market Drivers

Expansion of Residential Construction and Renovation Activities

Growing residential construction activity across emerging economies and increasing home renovation spending in developed countries remain major growth drivers for the carpet market. Rapid urbanization, rising disposable incomes, and expanding middle-class populations in countries such as China, India, Indonesia, and Vietnam are driving strong demand for residential flooring products. In North America and Europe, consumers are increasingly investing in premium home interiors and remodeling projects, positively supporting carpet replacement demand. Carpets continue to be preferred in bedrooms, living rooms, and luxury apartments due to their comfort, insulation properties, and aesthetic versatility. Rising demand for customized interior décor solutions is also encouraging manufacturers to launch premium and designer carpet collections.

Growth of Commercial Infrastructure and Hospitality Investments

Large-scale investments in hospitality, office infrastructure, airports, retail malls, educational institutions, and healthcare facilities are significantly contributing to carpet market expansion. Hotels and resorts increasingly require premium flooring products with advanced acoustic and durability properties, particularly within luxury and upscale hospitality segments. Commercial offices are also adopting modular carpet systems to improve workplace flexibility and reduce long-term maintenance expenses. Government investments in public infrastructure modernization, smart city projects, and transportation facilities are further supporting institutional carpet demand. Expanding tourism infrastructure in the Middle East and Asia-Pacific is particularly strengthening demand for commercial carpets and high-end woven flooring products.

Carpet Market Restraints

Volatility in Raw Material Prices

The carpet industry remains highly sensitive to fluctuations in raw material prices, especially synthetic fibers such as nylon, polyester, and polypropylene that are derived from petrochemical feedstocks. Changes in crude oil prices, supply chain disruptions, and geopolitical uncertainties directly impact production costs and manufacturer profit margins. Smaller manufacturers often struggle to absorb sudden input cost increases, resulting in pricing pressures across competitive markets. Rising transportation and logistics costs have also added additional operational challenges for global carpet suppliers.

Competition from Hard Flooring Alternatives

The increasing popularity of hard flooring products such as luxury vinyl tiles (LVT), ceramic tiles, hardwood flooring, and laminates represents a major restraint for carpet manufacturers. Consumers increasingly perceive hard flooring as easier to clean, more moisture resistant, and longer lasting, particularly in kitchens, offices, and high-traffic areas. Advancements in hard flooring aesthetics and durability have intensified competition, limiting carpet penetration across certain residential and commercial applications. Manufacturers must continue innovating in stain resistance, durability, and sustainability to maintain competitive positioning.

Carpet Market Opportunities

Growing Demand for Sustainable Commercial Flooring

The rising adoption of green building standards and environmentally responsible construction practices presents substantial growth opportunities for carpet manufacturers. Commercial developers, corporate offices, airports, and institutional buyers are increasingly prioritizing recyclable and low-emission flooring materials that align with sustainability objectives. This trend is encouraging manufacturers to invest in recycled fibers, carbon-neutral production facilities, and closed-loop recycling technologies. Companies capable of offering environmentally certified carpet products are expected to gain stronger penetration across premium commercial infrastructure projects. Europe and North America remain the leading regions for sustainable flooring demand, while Asia-Pacific is emerging rapidly as governments implement stricter environmental regulations within the construction sector.

Expansion of Smart Offices and Flexible Workspaces

The global expansion of smart offices, co-working infrastructure, and hybrid workplace models is generating significant opportunities for modular carpet systems. Carpet tiles are increasingly preferred within flexible office environments due to easier maintenance, acoustic insulation benefits, and adaptability to changing floor layouts. The growing focus on employee wellness and workplace aesthetics is also encouraging adoption of premium flooring products with improved comfort and sound absorption capabilities. Rapid commercial infrastructure development in the Middle East, India, Southeast Asia, and Africa is expected to further accelerate demand for high-performance commercial carpets over the next decade.

Product Type Insights

Tufted carpets dominate the global carpet market, accounting for nearly 46% of total revenue in 2025 due to their cost efficiency, design flexibility, and widespread residential and commercial applications. These carpets are highly preferred across North America and Europe because of faster manufacturing processes and broad style availability. Woven carpets continue to maintain strong demand within luxury hospitality and premium residential projects owing to superior durability and craftsmanship. Carpet tiles are among the fastest-growing product categories, particularly across offices, airports, educational institutions, and healthcare facilities where ease of replacement and modular installation offer operational advantages. Shag and specialty carpets continue gaining popularity in premium residential interiors, while flatweave rugs and handmade carpets maintain strong export demand from markets such as India, Turkey, and Iran.

Material Insights

Nylon remains the leading material segment, accounting for approximately 34% of global carpet market revenue in 2025 due to its superior durability, stain resistance, and resilience in high-traffic environments. Nylon carpets are extensively used across commercial offices, hotels, and institutional spaces where long-term performance is critical. Polyester carpets are witnessing rapid growth owing to affordability, softness, and increasing use of recycled PET fibers in sustainable flooring products. Polypropylene carpets remain popular in price-sensitive markets due to moisture resistance and lower production costs. Natural fiber carpets such as wool, sisal, jute, and cotton are increasingly preferred within premium eco-conscious residential interiors, particularly across Europe and luxury hospitality applications.

Application Insights

Residential applications continue to dominate the carpet market, contributing nearly 52% of global demand in 2025. Rising urban housing construction, home renovation activity, and increasing consumer investment in interior décor are driving strong residential carpet adoption globally. Commercial applications represent the fastest-growing segment, supported by rising investments in office infrastructure, hospitality, airports, retail spaces, healthcare facilities, and educational institutions. Carpet tiles are particularly gaining traction within commercial projects due to durability and lower lifecycle maintenance costs. Transportation applications, including automotive, railway, marine, and aviation carpeting systems, are also expanding steadily as manufacturers focus on lightweight and recyclable flooring materials to support sustainability objectives.

Distribution Channel Insights

Specialty flooring stores remain the leading distribution channel, accounting for nearly 38% of global carpet sales due to the importance of physical product inspection, design consultation, and customized flooring solutions. Home improvement retail chains continue to generate strong demand across residential remodeling markets, particularly in North America and Europe. E-commerce platforms are witnessing rapid growth as consumers increasingly prefer online browsing, digital room visualization tools, and direct-to-consumer purchasing models. Manufacturers are investing heavily in AI-driven customization platforms, augmented reality applications, and online interior visualization software to improve customer engagement and expand digital sales channels globally.

End-Use Insights

Household consumers remain the largest end-use segment in the carpet market, supported by rising residential construction and replacement demand. Hospitality and tourism infrastructure represent one of the fastest-growing end-use categories, with hotels, resorts, and luxury accommodations increasingly investing in premium flooring aesthetics and acoustic performance. Corporate offices are driving substantial demand for modular carpet tiles as businesses prioritize flexible workplace layouts and employee comfort. Healthcare facilities and educational institutions are increasingly adopting antimicrobial and sound-absorbing carpets to improve indoor environments. Government buildings, airports, and transportation infrastructure projects are also contributing significantly to institutional carpet demand globally.

| By Product Type | By Material | By Application | By Distribution Channel | By End Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 27% of the global carpet market, led primarily by the United States, which contributes nearly 22% of global demand. Strong residential renovation activity, premium home décor spending, and commercial office refurbishment projects continue to support market growth across the region. The United States remains a global leader in tufted carpet manufacturing and carpet tile adoption, particularly within corporate infrastructure and educational facilities. Canada is witnessing steady growth driven by urban housing development and commercial construction investments.

Europe

Europe represents nearly 24% of global carpet market revenue, supported by strong demand for sustainable and premium flooring products. Germany, the United Kingdom, France, Belgium, and the Netherlands are among the leading regional markets. European buyers increasingly prioritize recyclable carpets and environmentally certified flooring materials, driving innovation in sustainable manufacturing. Belgium remains a major production and export hub for high-quality commercial carpets and woven flooring products. Commercial office modernization and hospitality renovation projects continue to generate strong regional demand.

Asia-Pacific

Asia-Pacific dominates the global carpet market with nearly 38% share in 2025 due to rapid urbanization, infrastructure expansion, and growing middle-class consumer demand. China remains the largest regional market driven by large-scale residential construction and strong domestic manufacturing capabilities. India is among the fastest-growing carpet markets globally, supported by rising housing demand, smart city projects, and expanding exports of handmade carpets and rugs. Japan and South Korea continue to generate demand for premium commercial flooring solutions and technologically advanced carpet systems.

Latin America

Latin America represents a developing carpet market led by Brazil and Mexico. Rising urban housing demand, expanding retail infrastructure, and increasing commercial construction investments are supporting market growth. Mexico also benefits from integration with North American manufacturing supply chains, strengthening demand for industrial and commercial flooring products. Growing middle-class consumer spending on home interiors is gradually expanding residential carpet adoption across the region.

Middle East & Africa

The Middle East & Africa region is witnessing rapid growth supported by tourism infrastructure projects, luxury hospitality investments, airport expansions, and smart city developments. Saudi Arabia and the United Arab Emirates are among the fastest-growing markets due to mega infrastructure initiatives and rising premium commercial construction activity. Africa continues to maintain importance within handmade carpet exports and hospitality-driven flooring demand, particularly across tourism-focused economies such as South Africa and Kenya.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Carpet Market

- Mohawk Industries

- Shaw Industries Group

- Interface Inc.

- Tarkett

- Milliken & Company

- Beaulieu International Group

- Balta Group

- Victoria PLC

- Oriental Weavers

- Forbo Holding

- Dixie Group

- Tai Ping Carpets

- Ege Carpets

- Brintons Carpets

- Merinos Hali