Cannabis Market Size

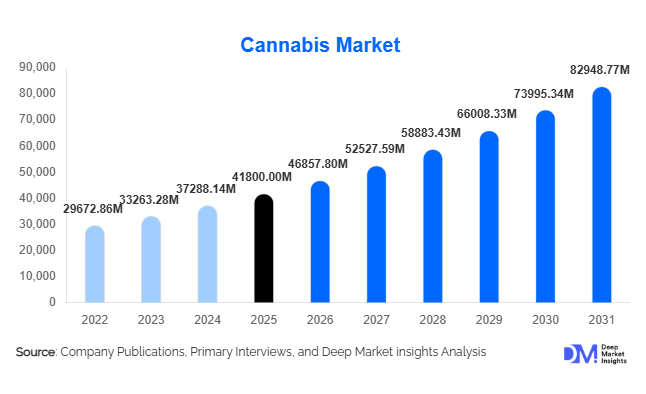

According to Deep Market Insights, the global cannabis market size was valued at USD 41,800 million in 2025 and is projected to grow from USD 46,857.80 million in 2026 to reach USD 82,948.77 million by 2031, expanding at a CAGR of 12.1% during the forecast period (2026–2031). The cannabis market growth is primarily driven by expanding legalization frameworks, increasing medical adoption of cannabinoid-based therapeutics, and rapid product innovation across adult-use and wellness segments.

The industry has transitioned from a fragmented, regulation-heavy landscape to a structured commercial ecosystem encompassing pharmaceutical-grade production, branded consumer products, and export-driven supply chains. North America remains the dominant revenue contributor, while Europe and Asia-Pacific are emerging as high-growth regions. Continued regulatory reform, clinical validation of cannabis-derived treatments, and technological advancements in cultivation and extraction are reshaping the competitive environment and accelerating institutional participation.

Key Market Insights

- Adult-use cannabis accounts for over 55% of global revenue, driven by expanding legalization in U.S. states and established markets such as Canada.

- THC-dominant products lead with nearly 58% market share, although CBD-dominant formulations are gaining momentum in medical and wellness applications.

- North America dominates with approximately 46% market share in 2025, supported by high consumer spending and regulatory maturity.

- Asia-Pacific is the fastest-growing region, registering an estimated CAGR of 15% due to emerging medical frameworks and export potential.

- Licensed dispensaries account for nearly 62% of sales, reflecting structured retail models in regulated markets.

- Indoor cultivation leads production models, contributing around 46% of total supply value due to quality consistency and compliance advantages.

What are the latest trends in the cannabis market?

Shift Toward Value-Added and Discrete Consumption Formats

Consumers are increasingly shifting from traditional dried flower to edibles, vape cartridges, capsules, and beverage infusions. This transformation reflects demand for precise dosing, discreet consumption, and lifestyle integration. Edibles and infused beverages are expanding retail shelf space, particularly among first-time users and older demographics seeking smoke-free alternatives. Product micro-dosing trends are also gaining traction, allowing controlled experiences with lower THC concentration per serving. This shift is supporting higher average transaction values and stronger brand differentiation in mature markets.

Pharmaceutical-Grade Cannabinoid Development

Clinical research and regulatory acceptance of cannabis-derived medicines are reshaping the industry. Pharmaceutical-grade isolates, synthetic cannabinoids, and GMP-certified production facilities are expanding rapidly. Markets such as Germany, the U.K., and Australia are witnessing structured prescription-based growth. Companies are investing in clinical trials targeting chronic pain, epilepsy, oncology support, and neurological disorders. This transition from recreational perception toward therapeutic validation is strengthening institutional investment and opening long-term revenue channels beyond retail-driven demand.

What are the key drivers in the cannabis market?

Expanding Legalization and Regulatory Reform

Regulatory expansion remains the most influential growth driver. The continued legalization of adult-use cannabis across U.S. states, coupled with progressive medical reforms in Europe and the Asia-Pacific, has significantly expanded the addressable market. Legalization reduces illicit trade dependency, increases tax revenues, and encourages structured investment. Regulatory clarity also enables cross-border trade in medical cannabis, strengthening export-oriented cultivation hubs in Latin America and Africa.

Rising Medical Adoption and Prescription Volumes

The global medical cannabis segment, valued at approximately USD 14,600 million in 2025, is expanding at a CAGR exceeding 13%. Physician acceptance is rising as clinical evidence supports efficacy in pain management, epilepsy treatment, and chemotherapy-related symptoms. Insurance discussions and structured reimbursement pathways in Europe are further supporting prescription growth, enhancing long-term demand stability.

What are the restraints for the global market?

Regulatory Fragmentation and Banking Constraints

Despite legalization progress, regulatory inconsistencies across jurisdictions increase compliance complexity. In the United States, federal-level prohibition limits interstate commerce and banking access, restricting operational efficiency and institutional capital flow. These constraints slow scalability and create cost disparities between regions.

Price Compression and Oversupply Risks

Mature markets such as Canada have experienced wholesale price declines of 15–25% due to excess cultivation capacity. Oversupply has pressured EBITDA margins, which currently range between 18–25% for leading operators. Sustained profitability requires operational efficiency, brand differentiation, and expansion into higher-margin derivative products.

What are the key opportunities in the cannabis industry?

Pharmaceutical and Biotech Integration

The integration of cannabis into mainstream pharmaceutical research represents a high-margin opportunity. Companies investing in GMP-certified extraction, minor cannabinoid research (CBG, CBN), and clinical trials can secure intellectual property advantages and stable revenue streams. This segment is expected to outpace traditional retail growth over the next decade.

Emerging Market Export Hubs

Countries such as Colombia, Uruguay, South Africa, and Thailand are positioning themselves as low-cost cultivation and export centers. As European medical demand expands, these regions can capitalize on supply gaps. Export-driven strategies allow companies to leverage favorable climate conditions and lower labor costs while accessing premium overseas markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 41800 Million |

| Market Size in 2026 | USD 46857.80 Million |

| Market Size in 2031 | USD 82948.77 Million |

| CAGR | 12.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Dried flower remains the largest product segment, accounting for approximately 39% of global revenue in 2025. Its leadership is primarily driven by strong consumer familiarity, lower price points compared to derivative formats, and established supply chains across North America and Canada. In adult-use markets, dried flower continues to dominate due to cultural consumption patterns and higher THC potency preferences. However, its share is gradually declining as value-added formats gain momentum. Edibles, beverages, vape cartridges, and concentrates are increasingly preferred by new consumers seeking discreet, smoke-free alternatives with controlled dosing.

Cannabis oils and tinctures hold a significant position within the medical segment, supported by physician preference for precise dosage administration and ease of titration. These formats are particularly dominant in European prescription markets. Edibles and infused beverages represent one of the fastest-growing subsegments, especially in the United States and Canada, driven by lifestyle integration and consumer shift toward wellness-oriented consumption. Meanwhile, isolates and distillates are emerging as high-margin B2B products, supplying pharmaceutical, nutraceutical, and cosmetic manufacturers. The growing demand for minor cannabinoids such as CBG and CBN is further expanding the high-value extract category.

Application Insights

Adult-use cannabis leads the global market with roughly 55% share of total revenue in 2025, primarily driven by legalization momentum across U.S. states and mature retail frameworks in Canada. High retail penetration, diversified product offerings, and expanding consumer demographics have positioned adult-use cannabis as the primary revenue engine. Continued state-level legalization in the United States remains the key driver sustaining segment dominance.

Medical cannabis accounts for approximately 35% of the global market, supported by structured prescription programs in Germany, the U.K., Australia, and other European markets. Clinical validation for chronic pain, epilepsy, and oncology-related symptoms continues to drive physician adoption and insurance discussions. Industrial cannabis, including hemp-derived cannabinoids and fiber applications, contributes the remaining share and benefits from rising demand in nutraceuticals, cosmetics, bioplastics, and functional foods. Industrial hemp’s regulatory flexibility in many countries supports steady expansion beyond traditional recreational and medical use cases.

Distribution Channel Insights

Licensed retail dispensaries dominate distribution, accounting for nearly 62% of total global sales. This leadership is driven by regulatory mandates in North America that require controlled retail environments, strict age verification, and product traceability. Dispensaries also enable brand differentiation, upselling of derivative products, and customer education, which strengthens repeat purchasing behavior.

Online channels are expanding rapidly, particularly for CBD-dominant and wellness-oriented products where regulations permit e-commerce. Digital platforms enhance consumer accessibility, subscription models, and direct-to-consumer brand strategies. Pharmacies and hospital channels remain critical in structured medical markets such as Germany and the U.K., where prescription-based access ensures product standardization and clinical compliance. Direct B2B bulk supply is growing in relevance, especially for pharmaceutical-grade isolates and distillates, reflecting increasing industrial and biotech integration.

Cultivation & Production Model Insights

Indoor cultivation leads the global production landscape with approximately 46% market share, primarily due to superior quality control, regulatory compliance, and consistent year-round output. Controlled environments allow producers to optimize cannabinoid profiles, reduce contamination risks, and meet stringent medical standards, particularly in Europe and North America.

Greenhouse cultivation provides cost efficiency advantages through natural light utilization while maintaining partial environmental control. This model is widely adopted in Canada and select European markets seeking balanced cost-quality outcomes. Outdoor cultivation remains prevalent in Latin America and Africa, where favorable climate conditions reduce production costs and support export-oriented operations. Additionally, biotechnological and synthetic cannabinoid production is emerging as a high-value niche, enabling pharmaceutical-grade precision and intellectual property development, particularly for rare cannabinoids and research-driven applications.

Explore more data points, trends and opportunities Download Free Sample Report

Cannabis Market Segmentations

By Product Type

- Dried Flower

- Cannabis Oils & Tinctures

- Edibles & Infused Beverages

- Vape Products & Concentrates

- Topicals & Transdermal Products

- Capsules & Tablets

- Isolates & Distillates

By Application

- Medical Cannabis

- Adult-Use (Recreational) Cannabis

- Industrial Hemp & Cannabinoid Applications

By Distribution Channel

- Licensed Retail Dispensaries

- Online/E-commerce Platforms

- Pharmacies & Hospital Channels

- Direct B2B Bulk Supply

By Cultivation & Production Model

- Indoor Cultivation

- Greenhouse Cultivation

- Outdoor Cultivation

- Biotechnological & Synthetic Production

Regional Insights

North America

North America holds approximately 46% of the global cannabis market share in 2025, making it the dominant regional contributor. The United States alone accounts for nearly 38% of global revenue, driven by widespread adult-use legalization at the state level, high per-capita spending, and advanced retail infrastructure. Expanding multi-state operator footprints, product innovation, and strong consumer awareness underpin growth. Canada contributes around 8%, supported by federal legalization, export capabilities, and established cultivation infrastructure. Continued regulatory liberalization and potential federal reforms in the U.S. remain key regional growth catalysts.

Europe

Europe represents approximately 24% of the global market, led by Germany, which dominates medical cannabis imports and prescription volumes. The U.K., Italy, and the Netherlands also contribute significantly through structured medical programs. The region’s growth is primarily driven by increasing physician acceptance, import reliance due to limited domestic production, and evolving adult-use discussions in countries such as Germany and Malta. Harmonization of EU medical cannabis standards and reimbursement pathways is expected to accelerate future growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region, registering an estimated CAGR of around 15%. Thailand and Australia are leading emerging medical markets, supported by regulatory reforms and healthcare integration. Rising healthcare investments, growing middle-class income, and export ambitions are driving expansion. While Japan remains limited to CBD products, broader cannabinoid wellness demand is rising. Increasing government approvals and international trade partnerships are expected to strengthen regional participation.

Latin America

Latin America is evolving into a strategic export hub. Colombia and Uruguay benefit from low production costs, favorable climates, and supportive regulatory frameworks for cultivation and export. Brazil is witnessing increasing medical cannabis adoption due to expanding patient awareness and regulatory flexibility for imports. The region’s competitive cost structure and export-oriented policies position it as a long-term supply center for Europe and North America.

Middle East & Africa

The Middle East & Africa region presents strong research and export potential. Israel leads in medical cannabis innovation and clinical research, contributing significantly to pharmaceutical development. South Africa is expanding licensed cultivation capacity, aiming to strengthen export channels. Favorable climatic conditions, lower operational costs, and increasing foreign investment are driving growth. Export demand from Europe remains the primary catalyst for regional expansion, particularly for pharmaceutical-grade products.

Key Players in the Cannabis Market

- Curaleaf Holdings

- Green Thumb Industries

- Trulieve Cannabis

- Canopy Growth Corporation

- Tilray Brands

- Aurora Cannabis

- Cronos Group

- Cresco Labs

- Verano Holdings

- Organigram Holdings

- Hexo Corp

- Sundial Growers

- TerrAscend

- Columbia Care

- Aphria