CAD in Apparel Market Size

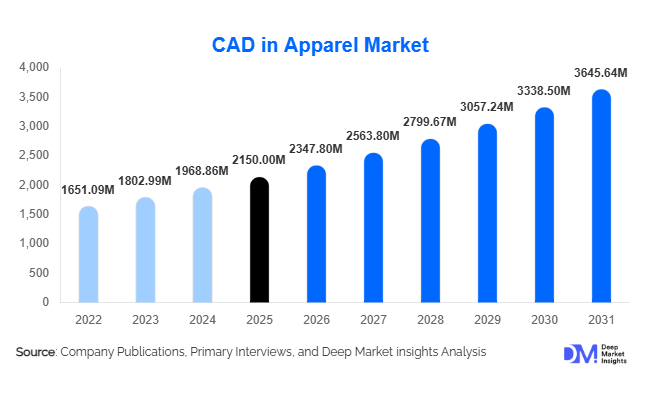

According to Deep Market Insights, the global CAD in apparel market size was valued at USD 2,150 million in 2025 and is projected to grow from USD 2,347.80 million in 2026 to reach USD 3,645.64 million by 2031, expanding at a CAGR of 9.2% during the forecast period (2026–2031). The market growth is primarily driven by the rapid digital transformation of the fashion and textile industry, increasing adoption of 3D design technologies, and the need to reduce product development cycles and material waste.

Key Market Insights

- 3D apparel design and virtual sampling technologies are gaining rapid adoption, significantly reducing physical sampling costs and accelerating time-to-market.

- Cloud-based CAD platforms are transforming accessibility, enabling SMEs in developing markets to adopt advanced design tools through subscription-based models.

- Asia-Pacific dominates the global market, driven by large-scale apparel manufacturing hubs in China, India, Bangladesh, and Vietnam.

- Large enterprises account for the majority of demand, investing heavily in integrated CAD and PLM ecosystems to streamline operations.

- Sustainability-driven design practices are influencing adoption, with CAD tools helping reduce fabric waste and optimize production processes.

- Integration with AI and digital workflows is enhancing design accuracy, automation, and collaboration across global supply chains.

What are the latest trends in CAD in apparel market?

Shift Toward 3D Design and Virtual Prototyping

The adoption of 3D CAD tools is rapidly transforming apparel design workflows. Companies are increasingly replacing traditional physical sampling with digital prototypes, enabling real-time visualization and faster design iterations. This shift is particularly beneficial for fast fashion brands, where speed and agility are critical. Virtual prototyping reduces costs associated with materials, shipping, and rework while improving collaboration between designers and manufacturers across geographies. Additionally, digital garment simulation allows brands to test fit, drape, and aesthetics before production, enhancing product quality and reducing returns in e-commerce channels.

Cloud-Based CAD and SaaS Adoption

Cloud deployment is emerging as a key trend, especially among SMEs. SaaS-based CAD platforms eliminate the need for high upfront investment and provide scalability, remote accessibility, and real-time collaboration. This is particularly impactful in emerging markets where smaller manufacturers are digitizing operations. Cloud solutions also enable integration with PLM and ERP systems, creating a unified digital ecosystem. The shift toward cloud is further supported by increasing internet penetration and the need for distributed design teams to collaborate seamlessly.

What are the key drivers in the CAD in apparel market?

Increasing Demand for Faster Product Development

The fashion industry is under constant pressure to shorten product development cycles due to fast fashion trends and seasonal collections. CAD tools enable automation of pattern making, grading, and prototyping, significantly reducing design timelines. This allows brands to respond quickly to changing consumer preferences and market trends, making speed a critical growth driver.

Digital Transformation Across Supply Chains

Apparel companies are increasingly adopting digital solutions to improve efficiency and coordination. CAD systems integrated with PLM and manufacturing tools enable seamless data flow across the value chain. This enhances visibility, reduces errors, and improves collaboration between design, sourcing, and production teams, particularly in global supply chains.

What are the restraints for the global market?

High Implementation and Training Costs

Advanced CAD systems, especially 3D solutions, require significant investment in software, hardware, and employee training. This creates a barrier for smaller players with limited financial resources, slowing adoption in certain regions.

Resistance to Traditional Workflow Changes

Many designers and manufacturers continue to rely on conventional manual processes. The transition to digital systems requires cultural and operational changes, which can delay adoption, particularly in developing markets.

What are the key opportunities in the CAD in apparel industry?

Expansion in Emerging Markets

Developing countries such as India, Bangladesh, and Vietnam present significant growth opportunities due to their large apparel manufacturing bases. Increasing digitalization and government support for industrial modernization are encouraging the adoption of CAD solutions. Vendors offering cost-effective and localized solutions can tap into this expanding market.

Sustainability and Waste Reduction Solutions

CAD systems play a crucial role in reducing fabric waste through optimized pattern layouts and digital sampling. As sustainability regulations become stricter, companies are increasingly adopting CAD to minimize environmental impact. This creates opportunities for vendors to integrate sustainability analytics and lifecycle assessment tools into their platforms.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2150 Million |

| Market Size in 2026 | USD 2347.80 Million |

| Market Size in 2031 | USD 3645.64 Million |

| CAGR | 9.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

2D pattern design software remains the dominant segment, accounting for approximately 32% of the market in 2025, primarily due to its foundational role in garment construction and its deep penetration across both large manufacturers and SMEs. This segment continues to lead as pattern development is a non-negotiable step in apparel production, and most organizations rely on 2D CAD systems for accuracy, repeatability, and cost efficiency. The relatively lower cost and ease of implementation compared to advanced systems further reinforce its widespread adoption, especially in emerging markets.

However, 3D design and simulation software is the fastest-growing segment, driven by increasing demand for virtual prototyping, reduced sampling costs, and enhanced visualization capabilities. These tools allow designers to simulate garment fit and aesthetics in real time, significantly reducing time-to-market. Meanwhile, PLM-integrated CAD solutions are gaining traction among large enterprises seeking seamless digital workflows across design, sourcing, and production. Textile design CAD tools are also expanding in importance as brands focus on differentiation through innovative prints and graphics, particularly in fast fashion and customized apparel segments.

Application Insights

Pattern making and grading lead the application segment with a market share of around 28%, as they form the backbone of apparel production processes globally. This segment’s leadership is driven by the necessity of precise sizing, fit consistency, and scalability across mass production, making CAD indispensable in these functions. The increasing complexity of global sizing standards and the need for rapid scaling of designs further strengthen demand in this segment.

Virtual prototyping is emerging as a high-growth application, supported by the industry-wide shift toward digital product development. It enables companies to minimize physical samples, reduce lead times, and improve collaboration between design and production teams. Production planning applications are also gaining traction, particularly among large manufacturers aiming to optimize workflows and reduce inefficiencies. Additionally, textile and print design applications are expanding rapidly due to rising demand for customization, short product cycles, and visually differentiated collections in both fashion and sportswear industries.

Deployment Mode Insights

On-premise solutions dominate the market with approximately 58% market share, primarily driven by large enterprises that prioritize data security, system control, and integration with legacy infrastructure. These organizations often operate complex global supply chains and prefer in-house systems to ensure confidentiality and operational stability. The established presence of on-premise solutions and existing investments also contributes to their continued dominance.

However, cloud-based deployment is the fastest-growing segment, fueled by its flexibility, scalability, and lower upfront costs. SaaS-based CAD platforms are particularly appealing to SMEs, enabling them to access advanced design capabilities without heavy capital expenditure. Cloud solutions also facilitate real-time collaboration across geographically dispersed teams, which is increasingly critical in global apparel production networks. As digital transformation accelerates, cloud adoption is expected to significantly reshape the competitive landscape.

End-Use Industry Insights

Apparel manufacturing remains the largest end-use segment, accounting for nearly 40% of the market, driven by extensive adoption in global production hubs. The dominance of this segment is attributed to the need for efficiency, precision, and scalability in mass production environments. CAD systems enable manufacturers to optimize material usage, reduce errors, and streamline production processes, making them essential tools in modern apparel factories.

Sportswear and activewear represent the fastest-growing segment, supported by rising global fitness awareness, increasing participation in sports, and demand for performance-driven apparel. CAD tools are critical in this segment for designing technically advanced garments with specific fit and material requirements. Fashion and luxury brands are also increasingly leveraging CAD for digital design, virtual showrooms, and rapid collection development, while retail private labels are adopting these solutions to enhance product differentiation and reduce time-to-market in highly competitive retail environments.

Explore more data points, trends and opportunities Download Free Sample Report

CAD in Apparel Market Segmentations

By Product Type

- 2D Pattern Design Software

- 3D Apparel Design & Simulation Software

- PLM Integrated CAD Solutions

- Textile Print & Graphics CAD Software

- Grading & Marker Making Software

By Application

- Fashion Design & Concept Development

- Pattern Making & Grading

- Virtual Prototyping & Sampling

- Production Planning & Optimization

- Textile & Print Design

By Deployment Mode

- On-Premise Solutions

- Cloud-Based (SaaS) Solutions

By End-Use Industry

- Apparel Manufacturing

- Fashion & Luxury Brands

- Retail Private Labels

- Sportswear & Activewear

- Uniforms & Workwear

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

Regional Insights

Asia-Pacific

Asia-Pacific leads the CAD in apparel market with approximately 45% market share in 2025, making it the largest and most influential region globally. China dominates the market, accounting for around 20% of global demand, followed by India, Bangladesh, and Vietnam. The region’s leadership is driven by its position as the global hub for apparel manufacturing, supported by large-scale production facilities and export-oriented industries. Increasing digital adoption among manufacturers, particularly SMEs, is accelerating demand for CAD solutions.

Government initiatives such as industrial modernization programs, textile parks, and incentives for digital transformation are key growth drivers. India, the fastest-growing country with a CAGR of nearly 12%, is benefiting from initiatives like “Make in India,” rising domestic consumption, and growing exports. Additionally, the need to meet international quality standards and reduce production lead times is pushing manufacturers across the region to adopt advanced CAD technologies.

North America

North America holds about 22% market share, led by the United States. The region is characterized by high adoption of advanced 3D CAD technologies and a strong presence of global fashion brands and technology providers. Growth in this region is primarily driven by innovation, early adoption of digital tools, and the increasing integration of CAD with AI and PLM systems. Another key driver is the strong demand for customization and on-demand production, particularly in e-commerce and direct-to-consumer models. Companies in North America are also focusing on sustainability, using CAD tools to reduce waste and optimize design processes. The presence of a highly skilled workforce and robust IT infrastructure further supports the rapid adoption of advanced CAD solutions.

Europe

Europe accounts for nearly 20% of the market, with key countries including Italy, Germany, France, and the UK. Italy leads the region due to its strong luxury fashion industry, where high-end brands invest heavily in advanced CAD solutions to maintain quality and innovation. Germany and the UK are also significant contributors, driven by technological advancement and digitalization initiatives. Growth in Europe is strongly influenced by stringent sustainability regulations and increasing emphasis on eco-friendly production practices. CAD systems are being adopted to minimize fabric waste, improve resource efficiency, and ensure compliance with environmental standards. Additionally, the region’s focus on high-value, design-intensive apparel supports the adoption of advanced 3D and integrated CAD solutions.

Latin America

Latin America represents around 6% market share, with Brazil and Mexico as key contributors. The region is gradually adopting CAD solutions as apparel manufacturing expands and digital transformation gains momentum. Growth is driven by increasing investments in local textile industries and the need to improve competitiveness in global export markets. Rising demand for affordable fashion and the expansion of regional retail brands are also contributing to adoption. Governments and industry players are focusing on improving manufacturing efficiency and reducing dependency on imports, which is encouraging the use of CAD technologies. However, cost sensitivity remains a challenge, making cloud-based solutions particularly attractive in this region.

Middle East & Africa

This region accounts for approximately 7% of the market, with growth driven by emerging manufacturing hubs and increasing investments in textile industries. Turkey is a major contributor due to its strong position as a bridge between European and Asian markets, while South Africa is leading adoption in the African continent. In the Middle East, countries such as the UAE and Saudi Arabia are witnessing the gradual adoption of CAD solutions, particularly among premium fashion brands and retail players. Growth drivers include diversification of economies away from oil, increasing focus on local manufacturing, and rising demand for high-quality apparel. Additionally, improving infrastructure, foreign investments, and government initiatives to develop textile industries are supporting long-term market expansion in the region.