Building Facade Cleaning Services Market Size

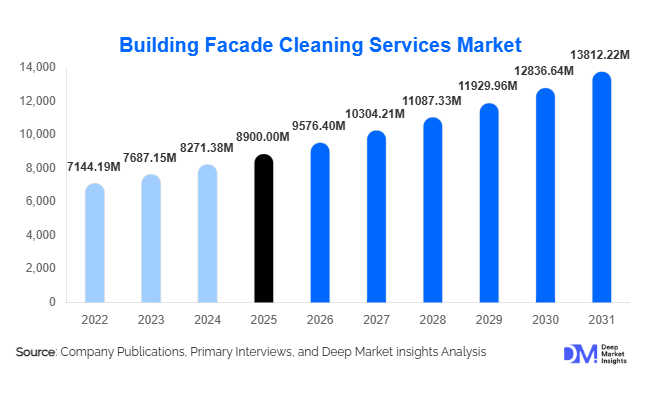

According to Deep Market Insights, the global building facade cleaning services market size was valued at USD 8,900 million in 2025 and is projected to grow from USD 9,576.40 million in 2026 to reach USD 13,812.22 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The market growth is primarily driven by rapid urbanization, increasing construction of high-rise buildings, and growing demand for aesthetic maintenance and regulatory compliance across commercial and residential infrastructure.

Key Market Insights

- High-rise and glass facade buildings are driving recurring demand, particularly in urban business districts and metropolitan regions.

- Automation in facade cleaning is gaining traction, with robotic and drone-based systems improving efficiency and safety.

- Asia-Pacific dominates the global market, supported by rapid infrastructure development and smart city initiatives.

- Commercial real estate remains the largest end-use segment, accounting for nearly half of total market demand.

- Sustainability-driven cleaning solutions are expanding, with increasing adoption of eco-friendly chemicals and water-saving technologies.

- Annual maintenance contracts (AMCs) are the preferred engagement model, ensuring stable revenue streams for service providers.

What are the latest trends in the building facade cleaning services market?

Automation and Robotics Transforming Cleaning Operations

The adoption of robotic and automated facade cleaning systems is transforming traditional service models. These systems significantly reduce reliance on manual labor, improve safety in high-rise environments, and enhance operational efficiency. Robotic cleaners equipped with sensors and AI capabilities can adapt to different building geometries, ensuring consistent cleaning quality. Drone-assisted inspection and cleaning are also gaining traction, especially for complex or hard-to-reach facades. This trend is particularly prominent in developed markets such as North America and parts of Europe, where labor costs and safety regulations are high.

Shift Toward Sustainable and Eco-Friendly Cleaning Solutions

Environmental sustainability is becoming a central focus in facade cleaning services. Companies are increasingly adopting biodegradable chemicals, water-efficient systems, and recycling technologies to minimize environmental impact. Green building certifications such as LEED are influencing cleaning standards, prompting building owners to choose eco-conscious service providers. Water-fed pole systems and chemical-free cleaning technologies are also gaining popularity, aligning with regulatory requirements and corporate sustainability goals.

What are the key drivers in the building facade cleaning services market?

Rapid Urbanization and Vertical Construction Growth

The increasing density of urban populations has led to a surge in high-rise and skyscraper construction globally. These structures require specialized and frequent facade cleaning, creating sustained demand for professional services. Emerging economies, particularly in the Asia-Pacific and the Middle East, are witnessing significant growth in vertical infrastructure, further boosting the market.

Expansion of the Commercial Real Estate Sector

The growth of office spaces, IT parks, shopping malls, and mixed-use developments is driving demand for regular facade maintenance. Commercial buildings prioritize cleanliness and visual appeal to attract tenants and customers, leading to higher service frequency and long-term contracts. This segment continues to generate consistent revenue streams for service providers globally.

What are the restraints for the global market?

High Operational and Compliance Costs

Facade cleaning involves significant costs related to equipment, skilled labor, safety measures, and insurance. Compliance with stringent safety regulations further increases operational expenses, particularly in developed markets. These factors can limit profitability and create barriers for smaller service providers.

Weather Dependency and Seasonal Constraints

Cleaning operations are highly dependent on weather conditions. Adverse conditions such as rain, strong winds, and extreme temperatures can delay projects and disrupt schedules. This variability impacts revenue predictability and operational efficiency, especially in regions with seasonal climatic fluctuations.

What are the key opportunities in the building facade cleaning services industry?

Integration of Smart and Predictive Maintenance Technologies

The integration of IoT and AI-driven predictive maintenance systems offers significant growth opportunities. These technologies enable real-time monitoring of building conditions and optimize cleaning schedules based on dirt accumulation and environmental factors. Service providers adopting such solutions can enhance efficiency and offer value-added services.

Expansion in Emerging Urban Markets

Rapid infrastructure development in emerging economies presents strong growth potential. Countries such as India, Indonesia, and Vietnam are investing heavily in urban development and smart city projects. These markets offer opportunities for both new entrants and established players to expand their footprint and capture long-term contracts.

Service Type Insights

Exterior glass cleaning dominates the building facade cleaning services market, accounting for approximately 32% of the total market share in 2025. This leadership is primarily driven by the rapid proliferation of glass-intensive architecture in commercial buildings, including office complexes, IT parks, airports, and retail malls. Glass facades require frequent cleaning due to dust accumulation, pollution exposure, and weather-related staining, resulting in recurring service demand and higher contract frequency. Additionally, premium commercial real estate owners prioritize visual aesthetics and transparency, further reinforcing demand for specialized glass cleaning solutions.

High-pressure washing and chemical cleaning services remain essential for non-glass surfaces such as concrete, stone, and composite panels, particularly in industrial and institutional buildings. Meanwhile, restoration and protective coating services are gaining traction as building owners increasingly focus on extending facade lifespan and reducing long-term maintenance costs. These value-added services are witnessing higher adoption in developed markets, where lifecycle cost optimization and sustainability are key decision factors.

Cleaning Method Insights

Manual cleaning methods continue to hold the largest share at around 45%, particularly in emerging markets across Asia-Pacific, Latin America, and parts of Africa. The dominance of manual cleaning is driven by lower initial costs, workforce availability, and flexibility in handling diverse building structures. Rope access and scaffolding-based cleaning methods remain widely used for mid-rise and even high-rise buildings in cost-sensitive markets.

However, automated and robotic cleaning methods are the fastest-growing segment, driven by increasing labor costs, stringent safety regulations, and technological advancements. Developed regions such as North America and Europe are leading this transition, where compliance with worker safety standards is critical. Robotic facade cleaning systems, drone-assisted inspections, and water-fed pole technologies are enhancing operational efficiency and reducing turnaround time. This shift is expected to accelerate globally, particularly in high-rise dense urban centers.

Building Height Insights

High-rise buildings account for approximately 38% of the market share, making them the leading segment in the building height category. This dominance is directly linked to the global trend of vertical urban expansion, particularly in megacities where land availability is limited. High-rise and skyscraper structures require specialized equipment, skilled labor, and frequent maintenance cycles, resulting in higher service value per building compared to low- and mid-rise structures.

The increasing number of mixed-use developments and smart city projects is further strengthening this segment. Additionally, high-rise buildings often incorporate glass-heavy facades, increasing the complexity and frequency of cleaning requirements. As urban skylines continue to evolve, this segment is expected to remain a primary revenue driver for service providers globally.

End-Use Insights

Commercial buildings dominate the market with nearly 47% share, driven by the need for regular maintenance, brand image enhancement, and compliance with hygiene and safety standards. Office buildings, shopping malls, and hospitality infrastructure require frequent facade cleaning to maintain visual appeal and attract tenants and customers. Long-term maintenance contracts are particularly prevalent in this segment, ensuring stable and recurring revenue streams.

Residential high-rise complexes are emerging as the fastest-growing segment, supported by rapid urban housing development, increasing disposable incomes, and the rise of premium gated communities. The growing preference for professionally managed residential properties is driving demand for scheduled facade cleaning services. Additionally, institutional and infrastructure segments, including airports and metro stations, are contributing to steady demand due to high visibility and public usage.

| By Service Type | By Cleaning Method | By Building Height | By End-Use Industry |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the market with approximately 38% share in 2025, driven by rapid urbanization, population growth, and large-scale infrastructure development. China and India are the primary contributors, supported by extensive construction of high-rise residential and commercial buildings. Government initiatives such as smart cities, urban redevelopment programs, and foreign investments in real estate are accelerating demand. Southeast Asian countries, including Indonesia, Vietnam, and Thailand, are also witnessing strong growth due to rising commercial construction and tourism infrastructure development. The availability of low-cost labor further supports the dominance of manual cleaning methods in the region.

North America

North America holds around 26% of the market share, with the United States accounting for the majority of demand. Growth in this region is driven by a mature commercial real estate sector, stringent safety and labor regulations, and high adoption of advanced cleaning technologies. The presence of a large number of high-rise office buildings and corporate headquarters necessitates regular facade maintenance. Additionally, increasing investments in automation, including robotic cleaning systems, are enhancing service efficiency and reducing operational risks, further driving market expansion.

Europe

Europe is characterized by a strong demand for sustainable and regulation-compliant cleaning solutions. Countries such as Germany, the UK, and France are focusing heavily on eco-friendly practices, driving the adoption of biodegradable cleaning agents and water-efficient technologies. Strict environmental regulations and green building certifications are key growth drivers in this region. Furthermore, the renovation and maintenance of heritage and historical buildings create additional demand for specialized facade cleaning services, particularly in Western Europe.

Middle East & Africa

The Middle East is a high-value market, particularly in countries such as the UAE and Saudi Arabia, where iconic skyscrapers, luxury hotels, and mega infrastructure projects drive demand. The region’s harsh climatic conditions, including dust storms and high temperatures, necessitate frequent facade cleaning, increasing service frequency and market value. Government-led megaprojects and tourism initiatives are further fueling growth. In Africa, the market is gradually expanding, supported by urbanization, infrastructure development, and increasing foreign investments, although growth remains uneven across countries.

Latin America

Latin America, led by Brazil and Mexico, exhibits moderate growth potential. Urbanization and expansion of commercial real estate are key drivers, particularly in major metropolitan areas. However, economic volatility and budget constraints can impact large-scale adoption of advanced cleaning technologies. Despite these challenges, increasing investments in infrastructure and rising awareness of building maintenance are creating new opportunities for service providers in the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Building Facade Cleaning Services Market

- ABM Industries

- ISS A/S

- Sodexo

- Compass Group

- Mitie Group

- CBRE Group

- JLL (Jones Lang LaSalle)

- Cushman & Wakefield

- Rentokil Initial

- OCS Group

- Servest Group

- Emrill Services

- Farnek Services

- Khidmah

- Kleen-Tex Industries