Box Liners Market Size

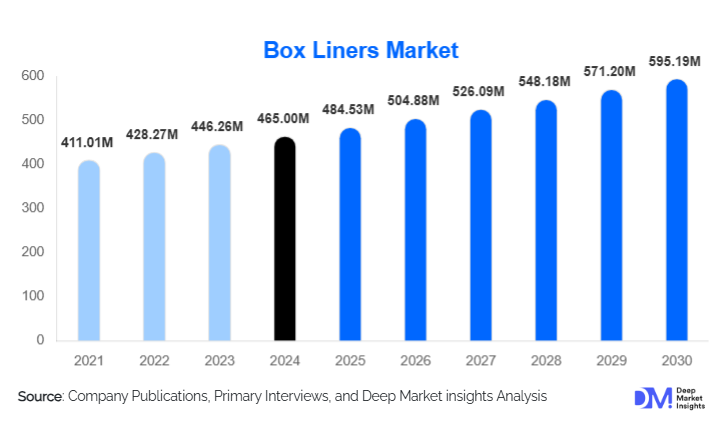

According to Deep Market Insights, the global box liners market size was valued at USD 465 million in 2025 and is projected to grow to USD 484.53 million in 2026 and further reach USD 595.19 million by 2031, expanding at a CAGR of 4.2% during the forecast period (2026–2031). Market growth is primarily driven by rising demand for industrial bulk packaging, rapid expansion of e-commerce logistics, stringent hygiene and contamination-control requirements, and increasing adoption of protective packaging across food, pharmaceutical, chemical, and agricultural industries.

Key Market Insights

- Polyethylene (PE) liners dominate the global market, holding the largest share due to cost-effectiveness, versatility, and widespread use in industrial, food, and e-commerce packaging.

- Asia-Pacific leads global demand, driven by rapid industrialization, bulk commodity exports, and expanding manufacturing output.

- Eco-friendly and biodegradable liners are emerging rapidly as companies shift away from single-use plastics under regulatory pressure.

- Bulk industrial packaging remains the largest application area, with chemicals, fertilizers, agriculture, minerals, and food commodities driving sustained long-term demand.

- E-commerce and retail shipments are the fastest-growing segment, benefiting from increased need for moisture, dust, and damage protection inside cartons.

- Technological advancements in multi-layer barrier films, anti-static liners, and customized gauge solutions are enabling manufacturers to serve niche high-value applications.

What are the latest trends in the box liners market?

Sustainability-Driven Liner Innovations Accelerating

Environmental policies and corporate sustainability mandates are pushing manufacturers toward recyclable PE/PP liners, biodegradable films, and compostable polymer-based liners. Large buyers across food, chemical, and agriculture sectors are increasingly opting for sustainable packaging that meets circular-economy goals and extended producer responsibility (EPR) regulations. Bioplastic-based liners, once limited by high costs, are now entering mainstream use as material technology matures. Companies are also investing in downgauged films that reduce plastic use while offering similar performance. This sustainability push is reshaping procurement strategies, compelling manufacturers to innovate with recyclable mono-material solutions, water-based inks, and reprocessed polymer blends without compromising protective capabilities.

Rapid Adoption of Custom and Application-Specific Liners

The market is seeing strong uptake of specialized liners tailored for individual industrial applications. This includes chemical-resistant liners for hazardous materials, anti-static liners for electronics, moisture-barrier liners for pharmaceuticals, and food-grade liners designed to maintain hygiene during transport. Customized gauge thicknesses, form-fit liners for bulk boxes, and high-strength liners for heavy commodities are becoming a competitive differentiator among suppliers. In parallel, industrial clients are increasingly adopting pre-formed liners to simplify warehouse operations, reduce spillage, enhance loading efficiency, and improve safety. This trend supports premiumization, raising average selling prices (ASPs) and improving margins for leading manufacturers.

What are the key drivers in the box liners market?

Growing Need for Protective Packaging Across Industries

Industrial sectors such as chemicals, fertilizers, pharmaceuticals, agriculture, food processing, and minerals rely heavily on secure bulk packaging. Box liners provide essential protection against leakage, contamination, moisture, abrasion, and product degradation. As global commodity trade expands, bulk shipments increasingly require heavy-duty liners to ensure regulatory compliance and product integrity. The growth of high-value and sensitive products—such as powdered chemicals, grain seeds, medical ingredients, and specialty materials—is further boosting long-term demand.

Expansion of E-commerce & Global Logistics Networks

E-commerce growth has created a large-scale demand for inner packaging solutions that reduce damage during transit. Box liners help protect goods from moisture, dust, and vibration, especially in long-distance shipments. Rising consumer expectations for intact deliveries and reduced return rates push retailers and 3PL providers to incorporate high-quality liners into their packaging standards. Global cross-border shipping is also amplifying the use of liners in cartons intended for electronics, FMCG, apparel, and perishables.

Shift Toward Sustainable, Compliant & Hygienic Packaging

Hygiene regulations in food, pharmaceuticals, nutraceuticals, and chemicals are driving the adoption of specialized liners with barrier properties. Regulatory pressures on plastic waste—especially in Europe and North America—are boosting demand for recyclable or compostable liners. ESG commitments across major corporations are pushing procurement departments to replace conventional liners with environmentally responsible alternatives, driving innovation and market expansion.

Restraints for the Global Market

Raw Material Price Volatility

Fluctuations in prices of polyethylene (PE), polypropylene (PP), and specialized polymers significantly impact manufacturing costs. These price swings reduce margins for suppliers and limit the willingness of end users to upgrade to advanced or eco-friendly liners. During periods of high polymer prices, substitution threats from lower-cost packaging alternatives increase, suppressing short-term demand.

Plastic Waste Regulations & Compliance Burden

Strict enforcement of plastic-waste laws, bans on single-use plastics, and requirements for recyclability challenge traditional liner manufacturers. Compliance increases costs and may force companies to redesign product lines. Some regions impose plastic taxes or packaging levies, discouraging consumption of conventional PE/PP liners unless sustainable alternatives are adopted.

What are the key opportunities in the box liners industry?

Sustainable & Biodegradable Liner Solutions

Widespread sustainability initiatives are opening opportunities for compostable films, recyclable mono-material liners, biodegradable polymers, and downgauged film technologies. Companies investing early in green-liner manufacturing—particularly in Europe, North America, and parts of Asia—can gain high-value contracts from food, chemical, and pharmaceutical industries seeking to meet ESG and circular-economy standards. These segments offer premium pricing and long-term recurring demand.

Industrial Growth in APAC, LATAM & MEA

Rapid industrialization and expansion of chemical, fertilizer, agro-processing, and mining sectors in emerging economies represent multi-billion-dollar opportunities. Bulk exports from India, China, Brazil, Mexico, the UAE, and South Africa increasingly require reliable liners to meet international packaging standards. As manufacturing shifts to Asia and Africa, box-liner consumption will grow through new facilities, expanded production capacities, and modernization of export logistics.

Specialized Liner Applications (Anti-Static, Barrier, Chemical-Resistant)

High-value sectors such as electronics, pharmaceuticals, fine chemicals, and premium food exports require advanced functional liners. Anti-static liners, UV-stabilized films, glycol-resistant liners, and multi-layer barrier solutions command significantly higher margins. Manufacturers that invest in R&D for specialty liners can differentiate themselves in a market where commodity-grade liners face intense price competition.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 465 Million |

| Market Size in 2026 | USD 484.53 Million |

| Market Size in 2031 | USD 595.19 Million |

| CAGR | 4.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

PE-based liners lead the global market, accounting for nearly 50% of total demand due to their low cost, durability, and compatibility with both industrial and retail packaging. PP liners serve niche chemical and high-temperature applications, while multi-layer laminated liners are gaining traction in pharmaceuticals and food export segments. Biodegradable liners, though currently niche, are the fastest-growing product type as sustainability regulations tighten globally. Heavy-duty liners dominate the bulk packaging sector, while thin-gauge liners are widely used in e-commerce and consumer goods packaging.

Application Insights

Bulk industrial packaging is the largest application segment, representing around 45–50% of the market. It includes liners for drums, bulk boxes, crates, and IBCs used to transport chemicals, fertilizers, powders, resins, grains, and agricultural inputs. Food & beverage applications are rapidly expanding due to rising hygiene requirements, while pharmaceutical and healthcare packaging is witnessing strong growth in barrier and sterile liners. E-commerce and retail form the fastest-growing application segment as companies focus on damage reduction and enhanced package protection.

Distribution Channel Insights

B2B procurement channels dominate the market, with manufacturers sourcing liners directly from packaging suppliers through long-term contracts. Industrial distributors and bulk packaging suppliers serve mid-sized customers, while online procurement platforms are emerging for standardized liner products. Customized liner development is often handled through direct manufacturer partnerships to meet application-specific requirements such as chemical resistance, static control, or food safety certification.

End-Use Industry Insights

Chemicals & petrochemicals lead the end-user segment with around 35–40% share, driven by demand for heavy-duty liners in bulk material transport. Agriculture and fertilizers follow, benefiting from rising global exports of seeds, agrochemicals, and bulk grains. Food & beverage and pharmaceuticals are high-growth categories, supported by stricter hygiene regulations. E-commerce and retail remain the fastest-growing end-use sector with robust adoption of carton liners to prevent product damage during last-mile delivery.

Explore more data points, trends and opportunities Download Free Sample Report

Box Liners Market Segmentations

By Material Type

- Polyethylene (PE – LDPE, LLDPE, HDPE)

- Polypropylene (PP)

- Biodegradable / Compostable Polymer Liners

- Multi-Layer Laminated Liners

- Specialty Barrier Liners (Anti-Static, Chemical-Resistant)

By Application

- Industrial Bulk Packaging (Drums, Crates, IBCs, Bulk Boxes)

- Food & Beverage Packaging

- Pharmaceutical & Healthcare Packaging

- Agriculture & Fertilizer Packaging

- E-Commerce & Retail Packaging

By Distribution Channel

- B2B Industrial Supply

- Direct Manufacturer Contracts

- Industrial Distributors

- Online Procurement Platforms

- Custom Liner Supply Partners

By End-Use Industry

- Chemicals & Petrochemicals

- Agriculture & Fertilizers

- Food & Beverage

- Pharmaceuticals & Healthcare

- E-Commerce, Retail & Consumer Goods

Regional Insights

North America

North America accounts for 25–30% of global demand, driven by mature chemical, pharmaceuticals, food, and e-commerce industries. The U.S. leads the region, with strong adoption of custom industrial liners and sustainable packaging solutions. Companies prioritize high-performance liners with strict compliance to FDA, food safety, and hazardous-material standards.

Europe

Europe holds a 15–20% market share, supported by high regulatory pressure for sustainable and recyclable packaging. Demand is strong in Germany, the U.K., France, and Italy, where industrial, food, and pharma sectors increasingly integrate recyclable and biodegradable liners. Circular-economy policies are accelerating the shift toward mono-material films.

Asia-Pacific

APAC is the largest and fastest-growing regional market with a 35–45% share in 2025. China and India dominate due to rapid industrialization, bulk commodity exports, and growth in chemicals, agriculture, and manufacturing. Southeast Asian markets such as Indonesia, Vietnam, and Thailand are also expanding their packaging infrastructure, contributing to strong liner demand.

Latin America

LATAM accounts for 5–8% of the market, with demand rising in Brazil, Mexico, Chile, and Argentina. Agriculture, fertilizers, and mining exports drive consumption of heavy-duty bulk liners. Increasing industrialization and improved port infrastructure support long-term growth.

Middle East & Africa

MEA holds a 5–10% share, with strong demand from petrochemical hubs such as Saudi Arabia, the UAE, and Qatar. Africa's agriculture and mining exports are creating new opportunities for bulk packaging liners, while South Africa remains the region’s most advanced market with established industrial liner usage.

Key Players in the Box Liners Market

- Berry Global

- Mondi Group

- Amcor plc

- Greif, Inc.

- Sealed Air Corporation

- Novolex

- Inteplast Group

- Coveris

- Uline

- Paiho Group

- Shenzhen Chuangxinhong Packaging

- LC Packaging

- Scholle IPN (SIG Group)

- Trioplast

- Shako Co.