Bonded Warehouse Market Size

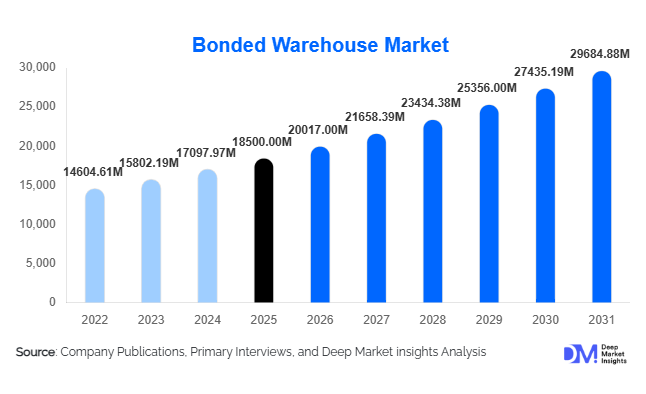

According to Deep Market Insights, the global bonded warehouse market size was valued at USD 18,500 million in 2025 and is projected to grow from USD 20,017.00 million in 2026 to reach USD 29,684.88 million by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The bonded warehouse market growth is primarily driven by increasing globalization, rising cross-border trade volumes, and the growing need for duty deferment solutions among importers and exporters. Additionally, the rapid expansion of e-commerce, increasing supply chain complexity, and government initiatives promoting free trade zones are further accelerating market demand.

Key Market Insights

- Bonded warehousing is becoming a strategic supply chain tool, enabling businesses to optimize cash flow through deferred duty payments and improved inventory management.

- Asia-Pacific dominates the market, driven by strong export-import activity in China, India, and Southeast Asia.

- 3PL providers are leading market operations, accounting for a significant share due to the increasing outsourcing of logistics functions.

- E-commerce and electronics sectors are the largest demand generators, requiring fast-moving, duty-efficient storage solutions.

- Technology adoption is accelerating, with IoT, AI, and warehouse automation improving operational efficiency and compliance.

- Integrated logistics services are gaining traction, as customers prefer bundled warehousing, transportation, and customs clearance solutions.

What are the latest trends in the bonded warehouse market?

Digitalization and Smart Warehousing Adoption

The bonded warehouse market is undergoing rapid digital transformation, with companies adopting advanced technologies such as IoT-enabled inventory tracking, AI-based warehouse management systems, and blockchain for customs documentation. These innovations improve real-time visibility, enhance compliance accuracy, and reduce operational inefficiencies. Automated storage and retrieval systems (AS/RS) are increasingly being deployed to handle high-volume goods, especially in major trade hubs. Additionally, cloud-based platforms are enabling seamless coordination between customs authorities, logistics providers, and clients, reducing processing time and errors. This trend is particularly strong in developed markets such as North America and Europe, but is also gaining momentum in the Asia-Pacific.

Growth of Free Trade Zones and Logistics Parks

Governments worldwide are expanding free trade zones (FTZs) and integrated logistics parks to boost international trade and attract foreign investments. Bonded warehouses are a core component of these ecosystems, offering tax benefits, simplified customs procedures, and strategic proximity to ports and airports. Countries such as the UAE, China, and India are heavily investing in such infrastructure to strengthen their position as global trade hubs. These developments are creating new opportunities for large-scale bonded warehousing facilities and enhancing overall logistics efficiency.

What are the key drivers in the bonded warehouse market?

Expansion of Global Trade and Supply Chains

The steady increase in global trade volumes is a major driver for the bonded warehouse market. Businesses engaged in import-export activities rely on bonded storage to manage inventory efficiently and defer customs duties. As supply chains become more globalized, the need for flexible and cost-effective warehousing solutions continues to rise.

Growth of E-commerce and Cross-Border Fulfillment

The rise of cross-border e-commerce has significantly increased demand for bonded warehouses. Online retailers use these facilities to store imported goods closer to end markets, enabling faster delivery and improved customer satisfaction. This trend is particularly strong in Asia-Pacific and North America, where e-commerce growth rates remain high.

What are the restraints for the global market?

Regulatory Complexity and Compliance Challenges

Strict customs regulations and varying policies across countries create operational challenges for bonded warehouse operators. Compliance requirements can increase administrative costs and limit market entry for smaller players.

High Capital and Operational Costs

Establishing and maintaining bonded warehouses requires significant investment in infrastructure, security systems, and technology. These high costs can act as a barrier to expansion, particularly in developing regions.

What are the key opportunities in the bonded warehouse industry?

Cross-Border E-commerce Expansion

The rapid growth of international e-commerce presents a major opportunity for bonded warehouse operators. Companies can leverage bonded storage to reduce delivery times, optimize inventory placement, and improve cost efficiency. Emerging markets such as Southeast Asia and India offer strong growth potential due to increasing online shopping penetration.

Technology Integration and Automation

Investments in automation, robotics, and AI-driven warehouse management systems can significantly enhance operational efficiency and reduce costs. Companies adopting smart technologies can gain a competitive edge by offering faster and more reliable services.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18500 Million |

| Market Size in 2026 | USD 20017 Million |

| Market Size in 2031 | USD 29684.88 Million |

| CAGR | 8.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Public bonded warehouses continue to dominate the global market, accounting for approximately 42% of the total share in 2025, primarily due to their cost-efficiency and accessibility for multiple users across industries. The leading driver behind this dominance is the increasing participation of small and medium-sized enterprises (SMEs) in international trade, which prefer shared infrastructure to avoid high capital investments. Public facilities also benefit from strategic locations near ports, airports, and free trade zones, enabling faster cargo handling and reduced transit times. In contrast, private bonded warehouses are gaining traction among large multinational corporations that require greater control over inventory management, compliance, and security, especially in high-value sectors such as electronics and pharmaceuticals. Government-operated bonded warehouses play a critical role in highly regulated industries, ensuring strict adherence to customs protocols, security norms, and national trade policies, particularly in defense, chemicals, and controlled goods segments.

Application Insights

General cargo storage remains the leading application segment, capturing approximately 48% of the market share in 2025, driven by its widespread applicability across diverse industries such as retail, consumer goods, electronics, and industrial manufacturing. The primary growth driver for this segment is the high volume of non-specialized goods traded globally, which do not require specific storage conditions, making general cargo facilities highly scalable and cost-effective. Meanwhile, cold storage bonded warehouses are witnessing the fastest growth, supported by rising global demand for temperature-sensitive products, particularly in pharmaceuticals, biologics, and perishable food items. Increasing regulatory requirements for product integrity and safety are further accelerating this trend. Additionally, hazardous and high-value goods storage segments are expanding steadily, driven by stricter compliance requirements, growing trade in chemicals and specialty products, and increasing demand for secure storage solutions for luxury goods and advanced electronics.

Distribution Channel Insights

Third-party logistics (3PL) providers dominate the bonded warehouse market, accounting for approximately 46% of the total share, as companies increasingly outsource logistics operations to specialized service providers. The key driver for this segment’s leadership is the growing need for operational efficiency, scalability, and cost optimization, especially among global enterprises managing complex supply chains. 3PL providers offer integrated solutions that combine warehousing, transportation, and customs clearance, reducing administrative burdens for clients. Integrated logistics services are gaining significant traction as businesses seek end-to-end supply chain visibility and seamless coordination across multiple geographies. These bundled offerings are particularly attractive for e-commerce and manufacturing companies aiming to streamline operations. On the other hand, enterprise-owned bonded warehouses remain relevant for large corporations with consistent, high-volume trade flows, where in-house control over logistics operations provides strategic advantages in terms of customization, security, and long-term cost management.

End-Use Industry Insights

The electronics and semiconductor industry leads the bonded warehouse market, contributing approximately 21% of the total demand in 2025. The primary driver for this segment is the high volume of international trade in electronic components, coupled with the need for secure, duty-deferred storage solutions to manage fluctuating demand cycles. The pharmaceutical industry is emerging as one of the fastest-growing end-use segments, driven by the globalization of drug manufacturing and distribution, along with stringent requirements for temperature-controlled storage and regulatory compliance. The rapid expansion of cross-border e-commerce and retail sectors is also significantly boosting demand for bonded warehouses, as companies seek to optimize inventory placement and reduce delivery timelines. Additionally, industries such as automotive, chemicals, and aerospace are contributing to steady growth, supported by increasing exports, global sourcing strategies, and the need for efficient supply chain management.

Explore more data points, trends and opportunities Download Free Sample Report

Bonded Warehouse Market Segmentations

By Product Type

- Public Bonded Warehouses

- Private Bonded Warehouses

- Government Bonded Warehouses

By Application

- General Cargo Storage

- Cold Storage

- Hazardous Goods Storage

- High-Value Goods Storage

By Distribution Channel

- Third-Party Logistics (3PL) Providers

- Integrated Logistics Service Providers

- Enterprise-Owned Warehousing

By End-Use Industry

- Electronics & Semiconductors

- Pharmaceuticals & Healthcare

- Retail & E-commerce

- Automotive

- Chemicals & Petrochemicals

- Food & Beverages

Regional Insights

Asia-Pacific

Asia-Pacific dominates the bonded warehouse market with a share of approximately 38% in 2025, driven by its position as the global manufacturing and export hub. China leads the region due to its extensive network of bonded logistics zones, high export volumes, and strong government support for trade facilitation. A key growth driver in the region is the expansion of free trade zones and export-oriented industrial clusters, which are increasing demand for duty-deferred storage solutions. India is emerging as a high-growth market, supported by initiatives such as “Make in India,” improvements in customs digitization, and rising manufacturing exports. Japan and South Korea contribute significantly through advanced logistics infrastructure and high-value exports, particularly in electronics and automotive sectors. Additionally, the rapid growth of e-commerce across Southeast Asia is further accelerating demand for bonded warehousing facilities.

North America

North America accounts for approximately 26% of the global market, with the United States being the largest contributor. The region’s growth is driven by advanced logistics infrastructure, high import volumes, and the increasing adoption of bonded warehouses for inventory optimization and duty deferment. A major driver is the expansion of cross-border e-commerce, which requires efficient storage solutions near key consumption markets. The presence of large multinational corporations and established 3PL providers further strengthens the market. Canada also plays a significant role, benefiting from strong trade relations with the U.S. and participation in agreements such as USMCA, which facilitate cross-border trade and increase demand for bonded storage solutions.

Europe

Europe represents a mature but strategically important market, led by countries such as Germany, the Netherlands, and the United Kingdom. The region’s growth is primarily driven by its well-established trade networks, strong intra-European commerce, and world-class port infrastructure. Major logistics hubs such as Rotterdam and Hamburg serve as critical gateways for global trade, driving demand for bonded warehousing. Additionally, stringent regulatory frameworks and customs procedures in the European Union encourage the use of bonded facilities to manage duties efficiently. The increasing focus on supply chain resilience and nearshoring strategies is also supporting steady demand growth across the region.

Middle East & Africa

The Middle East & Africa region is witnessing rapid growth in the bonded warehouse market, particularly in the UAE and Saudi Arabia. The primary driver for regional growth is heavy investment in free trade zones, logistics parks, and port infrastructure, aimed at positioning these countries as global trade hubs. The UAE, in particular, benefits from its strategic location connecting Asia, Europe, and Africa, along with business-friendly policies and tax incentives. Saudi Arabia’s Vision 2031 initiative is also driving infrastructure development and boosting logistics capabilities. In Africa, growing trade volumes and improving port infrastructure are gradually increasing the adoption of bonded warehousing, although challenges such as regulatory complexity and limited infrastructure persist.

Latin America

Latin America is an emerging market for bonded warehousing, with Brazil and Mexico leading regional demand. Growth in this region is primarily driven by expanding manufacturing exports, particularly in the automotive and electronics sectors, and strong trade ties with North America. Mexico benefits significantly from its proximity to the United States and participation in USMCA, which enhances cross-border trade flows. Brazil’s large domestic market and increasing import-export activities also contribute to demand. However, infrastructure limitations, regulatory challenges, and economic volatility remain key constraints that could impact the pace of market expansion in the region.

Key Players in the Bonded Warehouse Market

- DHL Supply Chain

- Kuehne + Nagel

- DB Schenker

- DSV A/S

- UPS Supply Chain Solutions

- FedEx Logistics

- Nippon Express

- CEVA Logistics

- Sinotrans

- CJ Logistics

- Agility Logistics

- Expeditors International

- Bolloré Logistics

- GEODIS

- Yusen Logistics