Body Tape Market Size

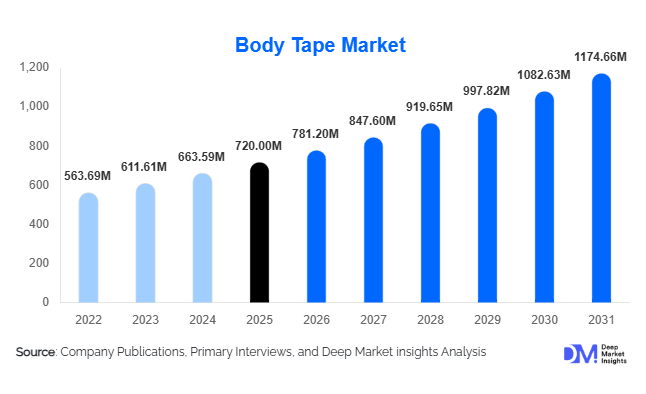

According to Deep Market Insights, the global body tape market size was valued at USD 720 million in 2025 and is projected to grow from USD 781.20 million in 2026 to reach USD 1,174.66 million by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The body tape market growth is primarily driven by rising sports participation, increasing demand for non-invasive aesthetic solutions, and expanding fashion applications requiring invisible support products. Growing awareness of injury prevention, rehabilitation techniques, and influencer-driven fashion trends is accelerating product adoption globally. Additionally, advancements in skin-safe adhesives and breathable materials are enhancing product performance, improving consumer trust, and supporting premium pricing strategies across developed and emerging markets.

Key Market Insights

- Kinesiology body tape dominates product demand, driven by rising sports injuries and physiotherapy adoption worldwide.

- E-commerce leads distribution channels, accounting for over 40% of global sales due to influencer marketing and direct-to-consumer strategies.

- North America holds the largest regional share, supported by high sports participation and beauty spending.

- Asia-Pacific is the fastest-growing region, fueled by expanding middle-class consumption and manufacturing capabilities.

- Hypoallergenic and latex-free variants are gaining popularity, particularly in Europe, due to strict dermatological standards.

- Private-label and OEM production in China and South Korea is strengthening global supply chains.

What are the latest trends in the body tape market?

Shift Toward Skin-Safe and Sustainable Adhesives

Manufacturers are increasingly focusing on dermatologically tested, latex-free, and hypoallergenic body tapes to reduce allergic reactions and improve comfort. Silicone-based and medical-grade acrylic adhesives are gaining traction due to their balance of durability and skin compatibility. Sustainable packaging and biodegradable cotton substrates are emerging trends, particularly in Europe and North America, where regulatory and consumer pressure is encouraging eco-conscious product innovation.

Expansion Beyond Fashion into Rehabilitation and Sports Medicine

While fashion-driven breast lift tapes gained early popularity through celebrity endorsements, the market is witnessing stronger and more stable growth from kinesiology applications. Sports therapists, chiropractors, and physiotherapists are incorporating body tape into injury management programs. Educational campaigns and sports event sponsorships are reinforcing clinical acceptance and repeat usage patterns, making the sports and rehabilitation segment a consistent revenue generator.

What are the key drivers in the body tape market?

Growing Global Sports Participation

The expansion of fitness culture, marathon participation, and organized sports leagues is increasing demand for muscle support and injury prevention solutions. Athletes and fitness enthusiasts increasingly use kinesiology tape to enhance performance and recovery, driving repeat purchases and brand loyalty.

Influence of Fashion and Social Media

Body tapes designed for invisible garment support are benefiting from red-carpet fashion trends and influencer marketing. Tutorials and styling demonstrations across digital platforms are accelerating consumer awareness and adoption, particularly among millennials and Gen Z consumers.

What are the restraints for the global market?

Skin Sensitivity and Regulatory Compliance

Concerns related to skin irritation and allergic reactions pose challenges for manufacturers. Compliance with dermatological standards in Europe and North America increases R&D and testing costs, impacting smaller manufacturers.

Price Sensitivity in Emerging Markets

Premium body tapes can cost significantly more than standard adhesive tapes, limiting penetration in price-sensitive regions. Local low-cost substitutes intensify pricing pressure.

What are the key opportunities in the body tape industry?

Integration with Medical and Physiotherapy Networks

Partnerships with rehabilitation clinics and sports medicine centers can unlock recurring institutional demand. Aging populations and rising musculoskeletal disorders globally create opportunities for clinical-grade product expansion.

Emerging Market Expansion

Rising disposable incomes in India, Brazil, Indonesia, and the UAE are driving demand for premium fashion and wellness products. Localized marketing and regional manufacturing hubs can improve cost competitiveness and market penetration.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 720 Million |

| Market Size in 2026 | USD 781.20 Million |

| Market Size in 2031 | USD 1174.66 Million |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Kinesiology body tape remains the leading product category, accounting for approximately 38% of global revenue in 2025. The segment’s dominance is primarily driven by the sustained rise in global sports participation, expanding gym memberships, marathon events, and increasing awareness of injury prevention and muscle recovery techniques. The growing integration of kinesiology taping in physiotherapy protocols and chiropractic treatments has strengthened repeat institutional demand. In addition, endorsements by professional athletes and sports trainers have enhanced product credibility, reinforcing adoption across both professional and amateur segments.

Breast lift and fashion support tapes collectively contribute nearly 30% of total demand, supported by social media influence, bridal wear trends, red-carpet fashion, and increasing demand for invisible garment support solutions. Seasonal demand spikes during wedding and festive seasons further strengthen this segment. Meanwhile, medical-grade adhesive body tapes are steadily gaining share as hospitals and rehabilitation centers expand usage for post-surgical care, scar management, and therapeutic support, benefiting from rising global healthcare expenditure and aging populations.

Material Composition Insights

Cotton-based body tapes hold approximately 34% of the total market share, making them the leading material segment. Their dominance is driven by superior breathability, skin comfort, moisture absorption, and suitability for prolonged wear. Cotton substrates are particularly preferred in kinesiology applications where flexibility and airflow are critical for athletic performance. In addition, consumer preference for natural and hypoallergenic materials in North America and Europe further supports cotton-based tape demand.

Synthetic blends such as polyester, nylon, and spandex are gaining momentum in high-performance sports applications due to enhanced elasticity, durability, and water resistance. These materials are increasingly used in waterproof and long-duration tapes designed for endurance athletes. Silicone-based materials are emerging as premium offerings in dermatologically sensitive markets, particularly in Europe, where regulatory standards and consumer awareness around skin safety are driving innovation in gentle adhesive formulations.

Adhesive Technology Insights

Acrylic adhesive technology dominates the market with nearly 46% share in 2025, driven by its cost-effectiveness, strong adhesion performance, and compatibility with both cotton and synthetic backings. Acrylic adhesives provide a balanced combination of durability and breathability, making them ideal for both sports and fashion applications. The scalability of acrylic coating processes also supports large-scale manufacturing, particularly in the Asia-Pacific.

Meanwhile, silicone adhesives are witnessing rapid growth in medical-grade and hypoallergenic segments due to reduced skin irritation and ease of removal. This technology is gaining strong traction in Europe and North America, where dermatological compliance standards are stringent. Hydrocolloid and rubber-based adhesives remain niche but are used in specialized medical and cosmetic applications.

Distribution Channel Insights

E-commerce leads the distribution landscape with approximately 42% market share in 2025. The segment’s leadership is driven by influencer marketing, social media tutorials, cross-border private-label trade, and direct-to-consumer brand strategies. Online platforms allow brands to offer product bundles, subscription models, and global shipping, significantly expanding reach beyond traditional retail boundaries.

Pharmacies and drug stores continue to play a vital role, particularly for medical-grade and kinesiology tapes recommended by healthcare professionals. Sports retailers remain influential in developed markets where consumers seek expert advice before purchasing performance-enhancing products. Specialty beauty stores contribute significantly to fashion tape sales, especially in urban centers.

End-Use Industry Insights

The sports & fitness industry accounts for nearly 35% of overall market demand, making it the largest end-use segment. Rising awareness of injury prevention, increasing sports participation among youth, and growing adoption of home fitness programs are the primary growth drivers. The segment benefits from repeat usage patterns and brand loyalty among athletes. The fashion & apparel sector follows closely, supported by event-based demand, influencer culture, and seasonal buying cycles. The bridal and premium fashion segments significantly contribute to high-margin sales. Meanwhile, medical & rehabilitation applications are expanding at approximately 9–10% annually due to aging demographics, rising musculoskeletal disorders, and the integration of taping techniques into physiotherapy treatment protocols.

Explore more data points, trends and opportunities Download Free Sample Report

Body Tape Market Segmentations

By Product Type

- Kinesiology Body Tape

- Breast Lift Tape

- Medical-Grade Adhesive Body Tape

- Fashion & Apparel Support Tape

- Scar & Post-Surgical Body Tape

By Material Composition

- Cotton-Based

- Synthetic (Polyester/Nylon/Spandex Blends)

- Silicone-Based

- Acrylic Adhesive-Based

- Latex-Free Hypoallergenic Materials

By Adhesive Technology

- Acrylic Adhesive

- Silicone Adhesive

- Hydrocolloid Adhesive

- Rubber-Based Adhesive

By End-Use Industry

- Sports & Fitness

- Fashion & Apparel

- Medical & Rehabilitation

- Cosmetics & Aesthetic Clinics

- Entertainment & Media Industry

By Distribution Channel

- E-Commerce

- Pharmacies & Drug Stores

- Sports Goods Retailers

- Specialty Beauty Stores

- Direct-to-Consumer (Brand Websites)

Regional Insights

North America

North America accounts for approximately 34% of the global market share in 2025, making it the largest regional market. The United States represents the majority of demand, driven by a strong sports culture, high participation in professional and amateur athletics, and widespread awareness of injury management solutions. Advanced healthcare infrastructure supports clinical adoption of kinesiology and medical-grade tapes. Additionally, high per capita spending on beauty and personal care products strengthens fashion tape sales. Canada contributes to steady growth through expanding physiotherapy networks and growing fitness trends.

Europe

Europe holds around 27% of global revenue, led by Germany, the UK, and France. The region’s growth is supported by stringent dermatological regulations that encourage innovation in hypoallergenic and silicone-based adhesives. Sustainability regulations and consumer demand for eco-friendly materials are further driving product differentiation. Strong public healthcare systems promote rehabilitation-based applications, while a growing fitness culture across Western Europe supports kinesiology tape demand.

Asia-Pacific

Asia-Pacific represents nearly 28% of the global market and is the fastest-growing region at approximately 10% CAGR. China plays a dual role as both a major manufacturing hub and a rapidly expanding consumer market. Rising disposable incomes and growing sports participation in China and India are strengthening domestic demand. Japan and South Korea contribute significantly through high adoption of advanced sports medicine products and innovation in adhesive technologies. Expanding e-commerce penetration further accelerates regional growth.

Latin America

Latin America is experiencing steady expansion, with Brazil and Mexico as key contributors. Brazil leads regional growth at nearly 9% CAGR, supported by increasing gym memberships, rising participation in football and athletic events, and expanding beauty awareness among urban consumers. Improving retail infrastructure and growing online sales channels are further enhancing product accessibility.

Middle East & Africa

The Middle East & Africa region is emerging as a high-potential market, led by the UAE and Saudi Arabia. Growth drivers include increasing disposable incomes, expanding fitness centers, and strong demand for fashion-oriented products linked to event-driven consumption. Government initiatives promoting sports participation and wellness programs further stimulate market growth. In Africa, South Africa contributes to demand through organized sports and rehabilitation applications, while gradual healthcare infrastructure improvements are supporting long-term expansion.

Key Players in the Body Tape Market

- 3M

- KT Tape

- RockTape

- Nitto Denko Corporation

- Kinesio Holding Corporation

- Mueller Sports Medicine

- SpiderTech Inc.

- StrengthTape

- Towatek Korea Co., Ltd.

- Healixon Ltd.

- GSPMED

- Adhesives Research, Inc.

- Scapa Group

- Paul Hartmann AG

- Johnson & Johnson