Blush Market Size

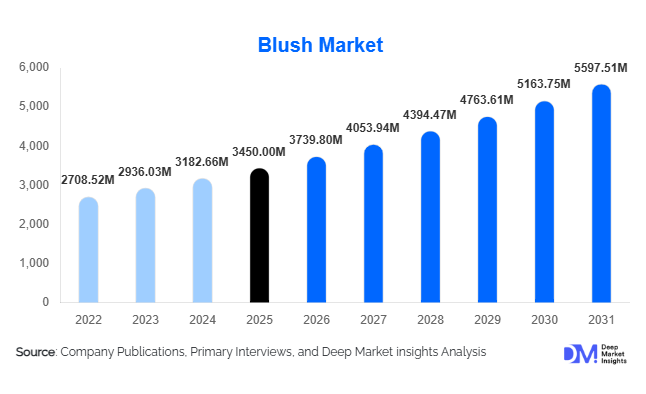

According to Deep Market Insights, the global blush market size was valued at USD 3,450 million in 2025 and is projected to grow from USD 3,739.80 million in 2026 to reach USD 5,597.51 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). The blush market growth is primarily driven by the rising popularity of natural makeup aesthetics, increasing consumer inclination toward multifunctional cosmetic products, and the rapid expansion of digital beauty retail platforms globally.

Key Market Insights

- Blush products are increasingly evolving into hybrid skincare-makeup formulations, incorporating ingredients such as hyaluronic acid and vitamins to meet clean beauty demand.

- Asia-Pacific dominates market growth momentum, supported by rising disposable income and strong e-commerce penetration in countries like China and India.

- Millennials account for the largest consumer base, contributing nearly 42% of total demand due to high engagement with beauty trends and brands.

- Online retail is the fastest-growing distribution channel, driven by influencer marketing, virtual try-ons, and direct-to-consumer models.

- Mid-range products dominate pricing segments, balancing affordability and premium quality perception among consumers.

- Clean beauty and sustainability trends, including vegan formulations and eco-friendly packaging, are reshaping product innovation strategies.

What are the latest trends in the blush market?

Skinification of Makeup Products

The integration of skincare benefits into cosmetic products is a defining trend in the blush market. Brands are increasingly formulating blushes with hydrating, anti-aging, and skin-protective ingredients, transforming them into multifunctional products. This trend aligns with consumer demand for minimalistic routines and healthier skin. Products combining pigmentation with skincare efficacy are gaining strong traction, particularly among younger consumers who prioritize ingredient transparency and long-term skin health. As a result, hybrid blush formulations are commanding premium pricing and expanding the product lifecycle within the beauty ecosystem.

Digital and Influencer-Driven Consumption

Social media platforms such as Instagram and TikTok are playing a pivotal role in shaping blush consumption trends. Viral makeup techniques, including “blush draping” and “sun-kissed glow,” are accelerating product adoption cycles. Influencers and beauty creators significantly impact purchasing decisions, with brands leveraging collaborations and user-generated content to drive visibility. Additionally, augmented reality (AR)-based virtual try-on tools are enhancing online shopping experiences, reducing purchase hesitation, and increasing conversion rates. This digital transformation is redefining how consumers discover, evaluate, and purchase blush products globally.

What are the key drivers in the blush market?

Growing Demand for Natural and Minimal Makeup

The shift toward natural, everyday makeup routines has significantly boosted demand for blush products. Consumers increasingly prefer subtle enhancements over heavy contouring, positioning blush as an essential product for achieving a healthy, radiant look. This trend is particularly strong among Gen Z and millennial consumers, who favor lightweight formulations and skin-like finishes. The versatility of blush across various makeup styles further strengthens its role as a core cosmetic product.

Expansion of E-commerce and Direct-to-Consumer Channels

The rapid growth of online retail platforms has transformed the blush market landscape. E-commerce enables brands to reach a global audience while offering extensive product variety and competitive pricing. Direct-to-consumer (DTC) strategies allow brands to build stronger relationships with customers, enhance margins, and leverage data-driven insights for personalized marketing. Subscription models, influencer partnerships, and social commerce are further driving online sales growth.

What are the restraints for the global market?

Intense Market Fragmentation and Pricing Pressure

The blush market is highly competitive, with numerous global and indie brands offering similar products. This saturation leads to pricing pressure and increased marketing expenses, making it challenging for new entrants to establish a foothold. Brands must continuously innovate and differentiate to maintain market relevance and profitability.

Regulatory and Ingredient Compliance Challenges

Stringent regulations regarding cosmetic ingredients, labeling, and safety standards pose challenges for manufacturers. Compliance requirements vary across regions, particularly in Europe and North America, increasing product development costs and slowing time-to-market. Growing scrutiny on chemical ingredients also necessitates investment in research and reformulation.

What are the key opportunities in the blush market?

Expansion in Emerging Markets

Emerging economies such as India, Brazil, and Indonesia present significant growth opportunities due to rising middle-class populations and increasing beauty awareness. Localization strategies, including region-specific shades and climate-adapted formulations, can help brands capture untapped demand in these markets. Rapid urbanization and digital adoption further accelerate market expansion.

Technology-Driven Personalization

Advancements in artificial intelligence and augmented reality are enabling personalized beauty experiences. AI-powered shade matching and AR-based virtual try-ons are improving customer engagement and reducing product returns. Brands investing in these technologies can enhance customer satisfaction and build long-term loyalty.

Product Type Insights

Powder blush continues to dominate the global market, accounting for approximately 38% of total revenue in 2025. The leadership of this segment is primarily driven by its ease of application, longer shelf life, cost-effectiveness, and compatibility across all skin types. Powder formulations are widely preferred by both beginners and professional makeup artists due to their blendability and buildable coverage, making them suitable for daily as well as professional use. Additionally, their stability in varying climatic conditions, particularly in humid regions, has further strengthened their global adoption.

Meanwhile, cream and liquid blushes are witnessing accelerated growth, supported by the rising popularity of dewy and natural makeup trends. These formats offer a skin-like finish and are often infused with hydrating ingredients, aligning with the “skinification” movement in cosmetics. Stick and gel blush formats are emerging as high-growth niches, especially among Gen Z consumers, due to their portability, quick application, and multifunctional usage (e.g., lip-and-cheek products). Continuous innovation in textures, pigmentation, and skincare-infused formulations is expanding the overall product landscape, allowing brands to cater to diverse consumer preferences globally.

Application Insights

Daily wear applications represent the largest segment, contributing nearly 50% of total demand. The dominance of this segment is driven by the shift toward minimalistic and natural makeup routines, where blush is increasingly considered an essential product for enhancing facial radiance. Consumers are incorporating blush into everyday routines due to its ability to deliver quick, visible results with minimal effort.

Professional makeup applications account for a significant share, supported by demand from salons, makeup artists, fashion industries, and media production. The growth of social events, weddings, and digital content creation has further boosted this segment. Special occasion usage continues to drive demand for high-performance, long-lasting formulations, particularly in premium product categories. Additionally, the increasing adoption of blush in gender-neutral and male grooming segments is creating new application avenues, expanding the addressable market, and supporting long-term growth.

Distribution Channel Insights

Offline retail channels, including specialty beauty stores, supermarkets, and department stores, account for approximately 60% of the market share. The continued dominance of this segment is driven by the consumer preference for physical product testing, shade matching, and instant purchase gratification. In-store experiences, including personalized consultations and product trials, play a critical role in influencing purchasing decisions, particularly for new product launches.

However, online channels are the fastest-growing segment, driven by rapid expansion in e-commerce platforms and brand-owned digital stores. The growth of this segment is fueled by convenience, wider product availability, competitive pricing, and the integration of digital technologies such as AR-based virtual try-ons. Social commerce, influencer-driven marketing, and direct-to-consumer (DTC) strategies are further strengthening online distribution networks. The shift toward omnichannel retailing is enabling brands to integrate both online and offline touchpoints, enhancing overall consumer engagement and sales conversion rates.

Traveler Type Insights

Millennials represent the largest consumer segment, accounting for around 42% of total market demand. This segment’s leadership is driven by high disposable income, strong engagement with digital beauty trends, and frequent product experimentation. Millennials are also more inclined toward premium and mid-range products, contributing significantly to market value growth.

Gen Z consumers are emerging as the fastest-growing segment, driven by their preference for innovative product formats, sustainable beauty solutions, and influencer-driven purchasing behavior. Their strong presence on social media platforms makes them key drivers of trend adoption and brand visibility. Gen X and older demographics contribute to stable demand, particularly in premium segments, where product quality and skin compatibility are prioritized. The growing acceptance of gender-neutral cosmetics is further broadening the consumer base across all demographic groups.

Age Group Insights

The 25–40 age group dominates the market due to higher purchasing power, brand loyalty, and consistent usage of cosmetic products. This demographic actively follows beauty trends while maintaining stable consumption patterns, making them a core target group for brands.

The 16–24 age group is a key growth driver, characterized by trend-driven consumption, experimentation with new formats, and strong influence from social media platforms. This group significantly contributes to the popularity of innovative products such as liquid and stick blushes. Older demographics, particularly those above 40 years, focus on premium, skin-friendly, and dermatologically tested products, supporting growth in high-value segments. Increasing inclusivity in product offerings, including wider shade ranges and formulations for different skin types, is enabling brands to cater effectively to all age groups.

| By Product Type | By Finish Type | By Ingredient Composition | By Application | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 28% of the global blush market, with the United States being the dominant contributor, accounting for over 75% of regional demand. Growth in this region is primarily driven by high consumer spending on personal care, the strong presence of global beauty brands, and the rapid adoption of premium and innovative products. The region also benefits from advanced retail infrastructure and high penetration of e-commerce platforms. Additionally, the influence of celebrity brands, social media trends, and frequent product launches supports sustained demand. The growing focus on clean beauty and sustainable formulations is further shaping product innovation in this region.

Europe

Europe holds around 24% of the global market share, led by countries such as France, Germany, and the United Kingdom. The region’s growth is driven by strong demand for premium cosmetics, increasing consumer preference for organic and clean-label products, and stringent regulatory standards ensuring product quality. France remains a key hub for luxury cosmetics, while Germany and the UK contribute significantly to volume demand. The rising popularity of sustainable and ethically sourced products is a major driver, with consumers increasingly prioritizing environmentally friendly packaging and formulations.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing region, accounting for nearly 32% of the global market. China, India, Japan, and South Korea are the primary growth engines. The region’s rapid expansion is fueled by rising disposable income, urbanization, increasing beauty awareness, and strong digital commerce ecosystems. China leads in terms of volume due to its massive consumer base and advanced e-commerce infrastructure, while India is witnessing rapid growth driven by a young population and increasing penetration of global brands. South Korea and Japan continue to influence global beauty trends through innovation and product development. The region is expected to maintain double-digit growth rates, making it a key focus area for market participants.

Latin America

Latin America represents about 8% of the global market, with Brazil and Mexico as major contributors. Regional growth is driven by increasing beauty consciousness, a large young population, and rising adoption of affordable cosmetic products. Brazil, in particular, is one of the largest beauty markets globally, supported by strong cultural emphasis on personal grooming. The expansion of retail networks and growing e-commerce adoption are further supporting market penetration in this region.

Middle East & Africa

The Middle East & Africa region accounts for approximately 8% of the global market, led by the UAE and Saudi Arabia. Growth in this region is supported by high per capita income, strong preference for premium and luxury cosmetics, and increasing influence of international beauty trends. The Middle East, in particular, demonstrates strong demand for high-performance and long-lasting makeup products due to climatic conditions. In Africa, rising urbanization, improving retail infrastructure, and increasing awareness of global beauty brands are contributing to gradual market expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|