Blackout Fabric Market Size

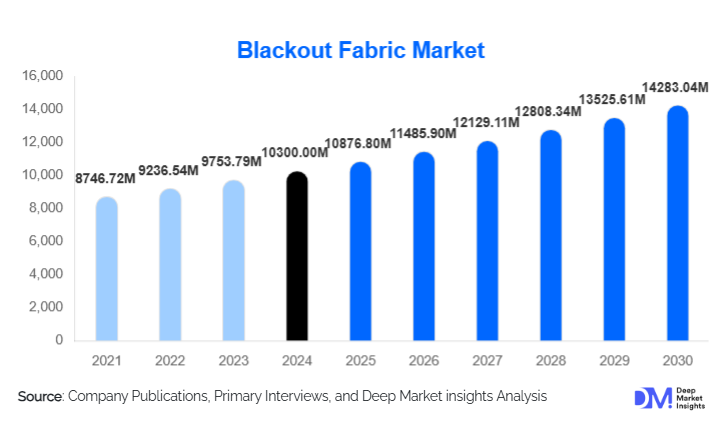

According to Deep Market Insights, the global blackout fabric market size was valued at USD 10,300 million in 2025 and is projected to grow from USD 10,876.80 million in 2026 to reach USD 14,283.04 million by 2031, expanding at a CAGR of 5.6% during the forecast period (2026–2031). The blackout fabric market growth is driven by expanding residential construction, rising adoption of energy-efficient building materials, and accelerating demand from hospitality, healthcare, and commercial infrastructure projects worldwide.

Key Market Insights

- Blackout fabrics are increasingly used as energy-efficient materials, reducing heat gain/loss and supporting green-building compliance.

- Residential applications dominate global demand, driven by rising home renovation, privacy needs, and modern interior décor trends.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, expanding middle-class income, and large-scale construction activity.

- Transportation, healthcare, and hospitality sectors are emerging high-volume buyers due to privacy, light control, and thermal-insulation requirements.

- Technological advancements in foam lamination, acoustic finishing, and fire-retardant coatings are reshaping product differentiation.

- Polyester blackout fabric remains the market leader, offering superior durability, cost-efficiency, and mass-manufacturing compatibility.

What are the latest trends in the blackout fabric market?

Energy-Efficient and Sustainable Blackout Solutions

Global building codes now emphasize thermal insulation, energy savings, and eco-friendly materials. As a result, manufacturers are expanding portfolios of thermal blackout fabrics, recycled polyester variants, low-VOC coatings, and fire-retardant materials that comply with green-building standards. These solutions reduce HVAC loads, support sustainability certifications, and help builders achieve cost-effective energy ratings. Growing consumer awareness of environmental impact is also pushing demand for eco-conscious blackout fabrics, giving rise to recycled yarn blends and chemical-free coatings. As climate-change policies strengthen worldwide, sustainable blackout products are expected to represent a growing share of premium demand.

Technological Integration and Multi-Functional Blackout Fabrics

The blackout fabric market is experiencing a surge in multi-functional engineered fabrics incorporating thermal regulation, acoustic dampening, flame resistance, antimicrobial coatings, and UV protection. These innovations cater to hospitals, hospitality chains, and high-performance office interiors. Additionally, compatibility with smart curtains, AI-driven home automation, and motorized blinds is rapidly expanding, aligning blackout materials with smart-home adoption. Laminated composite blackout fabrics capable of blocking 99–100% light are gaining traction in studios, theatres, RV interiors, aviation cabins, and high-end residential spaces. These advancements enhance product value, differentiate brands, and support long-term demand expansion.

What are the key drivers in the blackout fabric market?

Construction Boom and Interior Renovation Trends

Urbanization and growing residential construction across APAC, North America, and the Middle East have propelled demand for blackout fabrics. Consumers are prioritizing privacy, sleep quality, and aesthetic window design, making blackout curtains a staple of modern interiors. Renovation trends amplify demand further, with homeowners shifting toward premium fabrics with decorative, insulating, and acoustic capabilities. Commercial spaces, including offices, educational institutions, and retail sectors, also increasingly rely on blackout fabrics for climate control, privacy, and energy efficiency.

Growth in Hospitality and Healthcare Sectors

Hotels, resorts, serviced apartments, and hospitals represent one of the fastest-growing user bases. These industries require bulk procurement of blackout fabrics for guest rooms, recovery rooms, ICUs, conference areas, and VIP lounges. Hospitality chains prefer blackout fabrics for uniform aesthetics, superior comfort, and energy savings, while healthcare facilities prioritize light control and patient comfort. Large infrastructure investments worldwide, especially in Asia and the Middle East, further strengthen demand for institutional-grade blackout textiles.

What are the restraints for the global market?

Volatile Raw Material Prices

Blackout fabric manufacturing depends heavily on polyester yarn, synthetic resins, foam lamination chemicals, and specialized coatings. Global price fluctuations in petrochemical-derived materials can raise production costs and squeeze manufacturer margins. Smaller producers struggle to maintain competitiveness during raw material spikes. Additionally, supply-chain disruptions, particularly during global crises, create delays that impact large-scale procurement for construction and hospitality projects.

Competition from Substitutes and Alternative Window Treatments

Blackout fabrics face competition from blinds, shutters, window films, PVC panels, and smart glass technology. These alternatives often appeal to cost-sensitive buyers or minimalistic interior styles. In climates with lower sunlight intensity, basic window treatments may suffice, reducing blackout fabric adoption. For commercial spaces adopting automated shading or tinted glass solutions, traditional blackout fabrics may be deprioritized, posing a restraint on long-term growth.

What are the key opportunities in the blackout fabric industry?

Eco-Friendly and Recycled Blackout Fabrics

With global emphasis on sustainability, there is a strong market opportunity for blackout fabrics made from recycled polyester, bio-based coatings, waterless dyeing technologies, and low-VOC formulations. Builders, hotels, and corporate campuses are increasingly selecting materials that reduce carbon footprint and support green certifications like LEED and BREEAM. Manufacturers offering eco-label compliance and transparent material traceability can capture premium demand in Europe, North America, and APAC.

Expansion into Transportation and Specialized Sectors

Blackout fabrics are gaining significant adoption in transportation interiors, including buses, RVs, trains, aircraft cabins, and marine applications. Their light-blocking, thermal insulation, and privacy benefits make them essential in long-distance travel cabins. Similarly, demand is rising in cinemas, recording studios, media rooms, photography spaces, and planetariums. As these market segments modernize, the need for specialized blackout fabrics with noise-reduction and fire-retardant features presents a high-margin growth opportunity for fabric manufacturers worldwide.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 10300 Million |

| Market Size in 2026 | USD 10876.80 Million |

| Market Size in 2031 | USD 14283.04 Million |

| CAGR | 5.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

2-Ply blackout fabrics dominate the market, accounting for nearly 45–50% of 2025 demand. Their balance of cost-efficiency, light-blocking performance, and compatibility with decorative overlays makes them the preferred choice for residential and commercial curtains. Multi-ply and laminated blackout fabrics are gaining traction in premium and specialized applications requiring enhanced insulation, acoustic dampening, or durability. Basic single-ply fabrics continue to serve budget-conscious consumers but remain limited in advanced markets due to performance constraints.

Application Insights

Residential usage leads global demand, contributing roughly 50–55% of total market revenue in 2025. Rising home ownership, interior redesign trends, and the growing importance of sleep wellness are driving widespread adoption. Hospitality applications are the second-largest segment, supported by growing global hotel construction and refurbishment cycles. Healthcare applications are also expanding rapidly as hospitals adopt blackout fabrics for patient recovery areas, ICUs, and privacy partitions. Transportation and specialty applications, such as studios and theatres, represent fast-growing niches with high-value product requirements.

Distribution Channel Insights

B2B and OEM channels dominate, supplying blackout fabrics to curtain manufacturers, furniture brands, hotels, hospitals, and real-estate developers. Direct-to-consumer channels are expanding through home décor stores and rapidly growing e-commerce platforms offering customization, fabric visualization tools, and made-to-order blackout curtains. Institutional procurement, especially in hospitality and healthcare, remains a high-volume, high-frequency sales channel. Digital catalogues, influencer-driven décor trends, and comparison platforms are boosting online visibility and customer engagement.

End-User Insights

Households are the largest end-user, adopting blackout fabrics for bedrooms, living rooms, nurseries, and media rooms. Hotels and resorts rely heavily on blackout curtains for guest comfort and energy efficiency. Hospitals and clinics require advanced blackout fabrics offering antimicrobial, fire-retardant, and light-control performance. Transportation OEMs integrate blackout fabric into cabin dividers and privacy panels. Studios, theatres, and premium interior designers are increasingly adopting specialty-grade blackout textiles, creating long-term demand across diversified end-use categories.

Explore more data points, trends and opportunities Download Free Sample Report

Blackout Fabric Market Segmentations

By Product Type

- 1-Ply Blackout Fabric

- 2-Ply Blackout Fabric

- 3-Ply / Multi-Ply Blackout Fabric

- Laminated / Composite Blackout Fabric

By Material Type

- Polyester-Based Blackout Fabric

- Cotton-Based Blackout Fabric

- Poly-Cotton Blends

- Technical / Specialty Blackout Fabrics (Thermal, Acoustic, Fire-Retardant)

By Application

- Residential

- Commercial

- Hospitality (Hotels & Resorts)

- Healthcare & Institutional

- Transportation (Automotive, Rail, Aviation, Marine)

- Studios & Theatres / Specialty Use

By Distribution Channel

- B2B / OEM Supply

- Retail / Offline Stores

- E-commerce / Online Retail

- Institutional Bulk Procurement

Regional Insights

North America

North America represents one of the largest regional markets, accounting for 33–35% of global demand in 2025. Strong home renovation trends, rising smart-home adoption, and high commercial construction investments fuel demand for premium blackout fabrics. The U.S. dominates regional consumption, followed by Canada, with robust adoption across residential, hotel, and healthcare projects.

Europe

Europe remains a mature but high-value market with a strong preference for energy-efficient, sustainable, and acoustically enhanced blackout materials. Germany, the U.K., France, and the Nordics represent key consumers. Stringent building regulations and strong sustainability awareness drive the adoption of eco-friendly and fire-retardant fabrics. The region is also a leader in premium automated window treatments compatible with advanced blackout textiles.

Asia-Pacific

APAC is the fastest-growing region, propelled by rapid urbanization, residential construction booms, and rising middle-class affordability. China and India dominate demand, while Japan, South Korea, and Southeast Asia contribute to premium market expansion. The region also serves as the largest global manufacturing hub for blackout fabrics, strengthening export-driven growth.

Latin America

Demand in Latin America is growing steadily, driven by increasing home renovation trends and expanding hotel investments. Brazil and Mexico lead regional consumption. Budget and mid-range blackout solutions dominate due to cost-sensitive consumer behavior, though premium segments are emerging in metropolitan areas.

Middle East & Africa

MEA demand is fueled by large-scale hospitality, residential, and commercial construction projects, particularly in the UAE, Saudi Arabia, and South Africa. The region’s focus on luxury interiors, energy efficiency, and high-end hotel developments drives consistent demand for blackout fabrics. African nations with developing urban centers are increasingly adopting blackout fabrics in institutional and hospitality infrastructure.

Key Players in the Blackout Fabric Market

- Hunter Douglas

- Eclipse Curtains

- Mermet

- Serge Ferrari Group

- Springs Window Fashions

- Rowley Company

- Keystone Weaving Mills

- Sunbrella / Glen Raven

- Marlen Textiles

- Acoustical Surfaces Inc.

- Lutex

- Jameco Textiles

- Nien Made

- Herculite

- Phifer Incorporated