Biofuel Wood Pellets Market Size

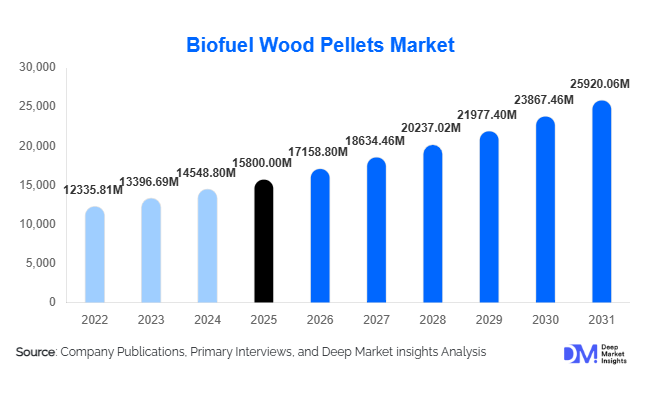

According to Deep Market Insights, the global biofuel wood pellets market size was valued at USD 15,800 million in 2025 and is projected to grow from USD 17,158.80 million in 2026 to reach USD 25,920.06 million by 2031, expanding at a CAGR of 8.6% during the forecast period (2026–2031). The market growth is primarily driven by increasing global emphasis on decarbonization, rising adoption of renewable energy sources, and the growing use of biomass as a substitute for coal in power generation.

Key Market Insights

- Utility-scale biomass power generation dominates demand, accounting for the majority of wood pellet consumption globally.

- Europe leads global demand, driven by strong regulatory frameworks supporting renewable energy and carbon neutrality goals.

- Asia-Pacific is the fastest-growing region, with Japan and South Korea significantly increasing pellet imports.

- North America serves as a major export hub, supplying pellets to Europe and Asia through long-term contracts.

- Industrial decarbonization is emerging as a key demand driver, especially in the cement and steel industries.

- Technological advancements such as torrefied pellets are improving efficiency, storage, and transportation.

What are the latest trends in the biofuel wood pellets market?

Shift Toward Utility-Scale Biomass Power

One of the most prominent trends is the growing use of wood pellets in utility-scale power plants. Coal-to-biomass conversions are accelerating, particularly in Europe and Asia, where governments are enforcing strict emission reduction targets. Power plants are increasingly adopting co-firing technologies, enabling them to reduce carbon emissions without significant infrastructure changes. This trend is expected to sustain long-term demand through supply contracts spanning 10–15 years.

Emergence of Advanced Pellet Technologies

Technological innovation is reshaping the market, with the introduction of torrefied pellets that offer higher energy density and better moisture resistance. These advanced pellets improve logistics efficiency and reduce storage-related losses. Automation in pellet manufacturing is also enhancing production efficiency, lowering operational costs, and ensuring consistent quality, thereby supporting global trade expansion.

What are the key drivers in the biofuel wood pellets market?

Global Decarbonization Policies

Governments worldwide are implementing policies such as carbon pricing, renewable energy targets, and emissions trading systems, which are significantly boosting the demand for biomass fuels. Wood pellets are increasingly recognized as a carbon-neutral alternative, driving adoption across power and industrial sectors.

Abundant Feedstock Availability

The availability of forestry residues and industrial wood waste in regions like North America ensures a steady and cost-effective supply of raw materials. This reduces dependency on virgin timber and supports sustainable production practices, strengthening the supply chain.

What are the restraints for the global market?

High Logistics and Transportation Costs

The bulk nature of wood pellets and the need for international shipping increase transportation costs significantly. This affects pricing competitiveness, especially in distant import markets.

Stringent Sustainability Regulations

Compliance with environmental standards and certification requirements adds complexity and cost to production. Concerns over deforestation and carbon accounting also pose challenges to market expansion.

What are the key opportunities in the biofuel wood pellets industry?

Expansion in Industrial Decarbonization

Industries such as cement, steel, and chemicals are increasingly adopting biomass fuels to reduce emissions. Wood pellets provide a scalable and efficient solution for high-temperature industrial processes, creating new growth avenues beyond traditional applications.

Rising Demand in Asia-Pacific

Countries like Japan and South Korea are significantly increasing pellet imports to meet renewable energy targets. This creates opportunities for exporters and new entrants to establish supply chains and production facilities.

Feedstock Type Insights

Industrial wood waste dominates the global biofuel wood pellets market, accounting for approximately 42% of the total market share in 2025. This segment leads primarily due to its cost efficiency, consistent quality, and year-round availability, making it highly suitable for large-scale pellet production. Sawmill by-products such as sawdust and wood shavings require minimal preprocessing, significantly reducing production costs and enhancing margin stability for manufacturers. Additionally, the use of industrial waste aligns with circular economy principles, which are increasingly favored under global sustainability frameworks.

Forest residues represent the second-largest feedstock segment, driven by increasing forest management practices and government-backed initiatives to reduce wildfire risks through biomass utilization. Meanwhile, agricultural residues are emerging as a high-growth segment, particularly in Asia-Pacific and Latin America, due to improved pelletization technologies and the need to monetize agricultural waste streams. Although currently smaller in share, this segment is expected to gain momentum as countries focus on diversifying feedstock sources and reducing dependence on traditional wood inputs.

Application Insights

Power generation remains the dominant application segment, contributing to nearly 60% of total global demand in 2025. The segment’s leadership is driven by the accelerated transition from coal to biomass in utility-scale power plants, particularly in Europe and Asia-Pacific. Governments are incentivizing co-firing and full biomass conversion projects through subsidies, carbon credits, and renewable energy mandates, making wood pellets a commercially viable alternative to fossil fuels.

Residential heating continues to maintain a stable share, supported by widespread adoption of pellet stoves and boilers in colder regions such as Europe and North America. The commercial heating segment, including district heating systems, is also expanding steadily, particularly in urban areas aiming to reduce carbon emissions. While smaller in comparison, combined heat and power (CHP) applications are gaining traction due to their efficiency advantages and ability to deliver both electricity and heat from a single fuel source.

Distribution Channel Insights

Direct supply contracts dominate the distribution landscape, accounting for over 70% of the total market share. This dominance is primarily driven by the procurement preferences of large-scale buyers such as utilities and industrial users, who rely on long-term supply agreements to ensure price stability, volume security, and consistent quality. These contracts often span multiple years, providing predictable revenue streams for manufacturers and reducing exposure to spot market volatility.

Retail distribution plays a comparatively smaller role and is largely confined to the residential segment, where pellets are sold in bagged form through dealers, home improvement stores, and local distributors. However, the gradual rise of online and direct-to-consumer channels is improving accessibility and convenience for smaller buyers, particularly in developed markets.

End-Use Industry Insights

The utilities and power generation sector remains the largest end-use industry, accounting for approximately 58% of global demand in 2025. This leadership is driven by strong policy support, including renewable energy targets, carbon taxation, and subsidies for biomass-based electricity generation. Utilities benefit from the ability to retrofit existing coal-fired infrastructure, significantly lowering capital investment requirements.

The industrial sector is the fastest-growing end-use segment, with growth rates exceeding 10% annually. Industries such as cement, steel, and food processing are increasingly adopting wood pellets to meet decarbonization targets and reduce reliance on fossil fuels. This shift is particularly prominent in regions with stringent emission regulations. Residential and commercial sectors continue to provide stable and recurring demand, especially in regions with colder climates. Increasing adoption of energy-efficient heating systems and government incentives for clean heating solutions are further supporting growth in these segments.

| By Feedstock Type | By Application | By End-Use Industry | By Distribution Channel | By Pellet Grade |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Europe

Europe dominates the global biofuel wood pellets market, accounting for approximately 45% of total demand in 2025. The region’s leadership is primarily driven by stringent decarbonization policies, carbon pricing mechanisms, and aggressive coal phase-out targets. Countries such as the UK, Germany, the Netherlands, and Denmark are major consumers, supported by well-established biomass infrastructure and government subsidies. The UK, in particular, leads demand due to large-scale biomass power plants and long-term import contracts. Additionally, the region benefits from strong district heating networks and high residential adoption of pellet-based heating systems, further reinforcing demand.

North America

North America holds around 30% market share, primarily functioning as the largest production and export hub globally. The United States and Canada benefit from abundant forest resources, advanced pellet manufacturing infrastructure, and efficient logistics networks. The region’s growth is driven by strong export demand from Europe and Asia, supported by long-term supply agreements. Domestic consumption is also increasing, particularly in residential heating and small-scale industrial applications, aided by favorable government policies promoting renewable energy adoption.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 10% during the forecast period. Japan and South Korea are the primary demand centers, driven by renewable energy targets, feed-in tariff (FIT) schemes, and limited domestic biomass resources. These countries rely heavily on imports, creating significant opportunities for global exporters. Additionally, emerging economies such as China and India are gradually adopting biomass energy as part of their broader energy transition strategies. Increasing investments in biomass power plants and industrial decarbonization initiatives are further accelerating regional growth.

Latin America

Latin America is an emerging market, with Brazil leading regional adoption. Growth in this region is driven by abundant biomass resources, expanding agricultural waste utilization, and increasing awareness of renewable energy solutions. Government initiatives promoting sustainable energy and rural development are encouraging local pellet production. Export potential is also rising, as countries in the region look to supply pellets to Europe and Asia.

Middle East & Africa

The Middle East & Africa region is at a nascent stage but shows promising growth potential. Countries such as South Africa are witnessing early adoption, driven by energy diversification efforts and the need to reduce dependence on coal and fossil fuels. Growth is further supported by international climate funding, renewable energy investments, and an increasing focus on sustainable energy infrastructure. In the Middle East, rising interest in alternative fuels and carbon reduction strategies is expected to gradually boost demand over the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Biofuel Wood Pellets Market

- Enviva Inc.

- Drax Group plc

- Pinnacle Renewable Energy

- Graanul Invest

- German Pellets GmbH

- Lignetics Inc.

- Energex Corporation

- Pacific BioEnergy

- Rentech Inc.

- Viridis Energy

- Pfeifer Group

- Stora Enso

- Vyborgskaya Cellulose

- Highland Pellets LLC

- AS Graanul Invest