Biodegradable Plastic Bags Market Size

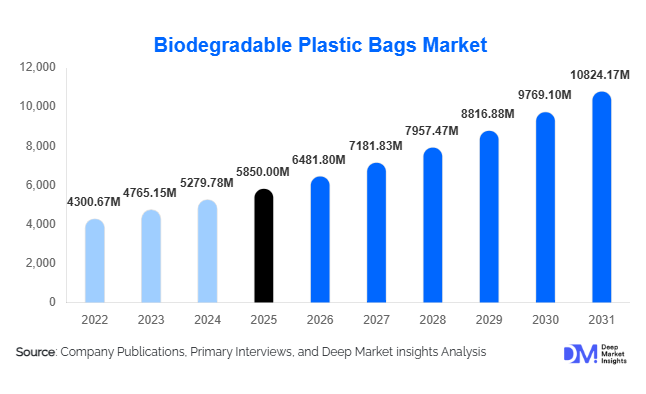

According to Deep Market Insights, the global biodegradable plastic bags market size was valued at USD 5,850 million in 2025 and is projected to grow from USD 6,481.80 million in 2026 to reach USD 10,824.17 million by 2031, expanding at a CAGR of 10.8% during the forecast period (2026–2031). The market growth is primarily driven by increasing regulatory restrictions on single-use plastics, rising environmental awareness among consumers, and growing adoption of sustainable packaging solutions across industries such as retail, food service, and healthcare.

Key Market Insights

- Regulatory bans on single-use plastics are accelerating the adoption of biodegradable alternatives across developed and emerging economies.

- Retail and food service sectors dominate demand, accounting for over 60% of total consumption globally.

- Asia-Pacific leads the market, supported by large-scale manufacturing capabilities and strong domestic demand.

- Europe remains the most regulated region, driving innovation in compostable and certified biodegradable materials.

- Technological advancements in biopolymers such as PLA, PHA, and PBAT blends are improving performance and cost-efficiency.

- Corporate sustainability commitments are increasing the bulk procurement of biodegradable plastic bags globally.

What are the latest trends in the biodegradable plastic bags market?

Shift Toward Advanced Biopolymer Blends

Manufacturers are increasingly adopting advanced biodegradable polymer blends, particularly combinations of PLA, PBAT, and PHA, to improve product durability, flexibility, and decomposition rates. These materials are enabling biodegradable bags to match the functional performance of conventional plastics while maintaining eco-friendly characteristics. Innovations are also focusing on enhancing resistance to moisture and extending shelf life, making these bags suitable for a wider range of applications, including industrial packaging and healthcare waste management.

Rising Adoption of Certified Compostable Products

There is a growing preference for certified compostable bags that comply with global standards such as EN 13432 and ASTM D6400. Businesses and consumers are increasingly prioritizing products that can decompose under industrial composting conditions within a defined timeframe. This trend is particularly strong in Europe and North America, where regulatory compliance and environmental labeling play a critical role in purchasing decisions. Companies are also investing in clear labeling and consumer education to differentiate compostable products from conventional plastics.

What are the key drivers in the biodegradable plastic bags market?

Stringent Government Regulations

Governments worldwide are implementing strict bans and restrictions on conventional plastic bags, which has significantly boosted demand for biodegradable alternatives. Policies such as extended producer responsibility (EPR) and plastic waste reduction targets are compelling businesses to adopt sustainable packaging solutions. Regions such as Europe and parts of the Asia-Pacific are leading in regulatory enforcement, creating a favorable environment for market expansion.

Growing Consumer Environmental Awareness

Consumers are becoming increasingly conscious of environmental issues, particularly plastic pollution and its impact on marine ecosystems. This shift in consumer behavior is driving demand for eco-friendly packaging solutions, with many consumers willing to pay a premium for biodegradable products. Retailers are responding by offering sustainable alternatives, further accelerating market growth.

What are the restraints for the global market?

High Production Costs

Biodegradable plastic bags are more expensive to produce compared to conventional plastic bags, primarily due to higher raw material costs and limited economies of scale. This price disparity can limit adoption, particularly in cost-sensitive markets where affordability remains a key concern.

Limited Composting Infrastructure

The effectiveness of biodegradable plastic bags depends on proper disposal and composting infrastructure, which is lacking in many regions. Without adequate facilities, these products may not decompose as intended, reducing their environmental benefits and slowing market adoption.

What are the key opportunities in the biodegradable plastic bags industry?

Expansion in Emerging Markets

Emerging economies such as India, Brazil, and Indonesia present significant growth opportunities due to rapid urbanization, expanding retail sectors, and increasing regulatory focus on plastic waste management. Government initiatives promoting sustainable manufacturing and local production are further supporting market entry and expansion in these regions.

Innovation in Next-Generation Biodegradable Materials

Advancements in materials such as PHA and marine-degradable plastics are opening new application areas, including marine environments and healthcare packaging. Companies investing in R&D can capitalize on these high-growth segments by offering differentiated, high-performance products that meet evolving regulatory standards.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5850 Million |

| Market Size in 2026 | USD 6481.80 Million |

| Market Size in 2031 | USD 10824.17 Million |

| CAGR | 10.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Carry bags continue to dominate the biodegradable plastic bags market, accounting for approximately 35% of the total market share in 2025. The leadership of this segment is primarily driven by stringent global regulations banning single-use plastic carry bags, particularly across retail and grocery sectors. Governments in Europe, the Asia-Pacific region, and parts of North America have mandated the transition to biodegradable alternatives, making carry bags the most visible and immediate replacement category. Additionally, high consumption frequency in supermarkets and convenience stores ensures sustained volume demand, reinforcing its dominance.

Garbage and waste disposal bags represent another significant segment, supported by increasing demand from municipalities, commercial establishments, and residential waste management systems. The push for segregated waste collection and composting initiatives is further driving adoption in this segment. Compostable bags are witnessing accelerated growth due to regulatory mandates requiring certified compostable materials for organic waste collection. Rising consumer awareness regarding environmental sustainability and proper waste disposal practices is further strengthening this segment’s uptake. Industrial and packaging bags are also gaining traction, particularly in logistics, manufacturing, and e-commerce sectors. Companies are increasingly adopting biodegradable packaging solutions to align with ESG goals and reduce carbon footprints, contributing to steady growth in this category.

Material Type Insights

Polylactic acid (PLA) leads the biodegradable plastic bags market with an estimated 28% share in 2025, driven by its scalability, commercial availability, and compatibility with existing plastic processing infrastructure. The segment’s dominance is largely attributed to its cost-efficiency at scale and widespread use in food packaging and retail applications. Additionally, PLA benefits from strong supply chain integration, particularly in regions with abundant agricultural feedstock such as corn. Starch-based plastics remain widely used in cost-sensitive markets, especially in Asia-Pacific and Latin America, where affordability is a critical factor. These materials are commonly used for lightweight carry bags and agricultural applications.

PBAT is gaining increasing importance due to its flexibility and biodegradability, often blended with PLA to enhance performance characteristics such as strength and elongation. This makes it particularly suitable for applications requiring higher durability. PHA, although currently representing a smaller share, is emerging as a high-growth segment due to its superior biodegradability in marine and soil environments. Its potential applications in high-value sectors such as healthcare and marine packaging are expected to drive future growth.

End-Use Industry Insights

The retail and consumer goods sector dominates the biodegradable plastic bags market, accounting for approximately 38% of total demand in 2025. This leadership is driven by direct regulatory pressure on retailers to eliminate conventional plastic bags, combined with high consumer visibility and usage frequency. Large retail chains and supermarkets are increasingly adopting biodegradable alternatives to meet sustainability targets and enhance brand positioning. The food and beverage industry is another major contributor, particularly in takeaway, delivery, and fresh produce packaging. The rapid growth of online food delivery platforms is further amplifying demand for sustainable packaging solutions.

The hospitality and food service sector is the fastest-growing segment, with a CAGR exceeding 12%. Increasing adoption of eco-friendly practices by restaurants, cafes, and quick-service chains is driving demand for biodegradable bags, particularly for takeaway packaging. The agriculture sector is emerging as a new application area, particularly for biodegradable mulch films and utility bags. These products help reduce soil contamination and eliminate the need for plastic removal, making them increasingly attractive for sustainable farming practices.

Distribution Channel Insights

Direct B2B sales dominate the market, accounting for approximately 55% of total distribution in 2025. This segment leads due to bulk procurement by large retailers, industrial users, municipalities, and institutional buyers. Long-term supply contracts and cost advantages further strengthen the position of direct sales channels. Retail distribution channels, including supermarkets and specialty stores, play a significant role in consumer-facing segments, particularly for household and small-scale usage. These channels are benefiting from increasing consumer awareness and preference for eco-friendly products.

E-commerce platforms are emerging as a rapidly growing distribution channel, driven by digitalization and the convenience of online purchasing. Small and medium enterprises, along with individual consumers, are increasingly sourcing biodegradable bags through online platforms, contributing to this segment’s growth.

Explore more data points, trends and opportunities Download Free Sample Report

Biodegradable Plastic Bags Market Segmentations

By Material Type

- Starch-Based Plastics

- Polylactic Acid (PLA)

- Polybutylene Adipate Terephthalate (PBAT)

- Polyhydroxyalkanoates (PHA)

- Cellulose-Based Plastics

- Blended Biodegradable Polymers

By Product Type

- Carry Bags

- Garbage & Waste Disposal Bags

- Compostable Bags

- Industrial & Packaging Bags

- Agricultural Utility Bags

By End-Use Industry

- Retail & Consumer Goods

- Food & Beverage

- Healthcare

- Agriculture

- Hospitality & Food Service

- Industrial & Logistics

By Distribution Channel

- Direct B2B Sales

- Retail Distribution

- E-commerce Platforms

By Degradation Type

- Industrial Compostable Bags

- Home Compostable Bags

- Soil-Degradable Bags

- Marine-Degradable Bags

Regional Insights

Asia-Pacific

The Asia-Pacific region leads the biodegradable plastic bags market, with an approximate 42% share in 2025, driven by a combination of large-scale manufacturing capacity, rising domestic consumption, and supportive government policies. China dominates regional production due to its well-established polymer industry and export capabilities, while India is the fastest-growing market with a CAGR exceeding 14%. Growth in India is fueled by nationwide plastic bans, increasing urbanization, and government initiatives promoting sustainable alternatives. Additionally, the region benefits from abundant raw materials such as starch-based feedstock, enabling cost-effective production.

Europe

Europe accounts for around 28% of the global market, with countries such as Germany, France, and Italy leading adoption. The region’s growth is primarily driven by stringent EU regulations, including bans on single-use plastics and mandates for compostable packaging. High consumer awareness and strong demand for certified eco-friendly products further support market expansion. Europe also serves as a global hub for innovation in biodegradable materials, with significant investments in R&D and circular economy initiatives driving long-term growth.

North America

North America holds approximately 18% market share, with the United States being the dominant contributor. Growth in this region is driven by state-level plastic bans, increasing corporate sustainability commitments, and rising consumer preference for environmentally friendly products. Large retailers and food service companies are actively transitioning to biodegradable packaging solutions. Canada is also witnessing steady growth, supported by federal regulations and increasing environmental awareness among consumers.

Latin America

Latin America is an emerging market, led by Brazil and Mexico. Growth in this region is driven by increasing regulatory focus on plastic waste reduction and expanding retail and food service sectors. Urbanization and rising environmental awareness are further supporting demand. However, limited composting infrastructure and higher product costs remain key challenges that may slow adoption in certain areas.

Middle East & Africa

The Middle East and Africa region is gradually adopting biodegradable plastic bags, with key markets including the UAE and South Africa. Growth is driven by government-led sustainability initiatives, increasing tourism-related demand, and rising awareness of environmental issues. In the Middle East, diversification strategies away from oil-based economies are encouraging investments in sustainable materials. In Africa, improving waste management systems and international environmental commitments are supporting gradual market expansion, although adoption remains slower compared to other regions.

Key Players in the Biodegradable Plastic Bags Market

- BASF SE

- Novamont S.p.A.

- TotalEnergies Corbion

- NatureWorks LLC

- Danimer Scientific

- Biome Bioplastics

- Plastiroll Oy

- TIPA Corp

- BioBag International

- Futamura Group

- Mondi Group

- Smurfit Kappa

- Amcor Plc

- Toray Industries

- Mitsubishi Chemical Group