Binder Clips Market Size

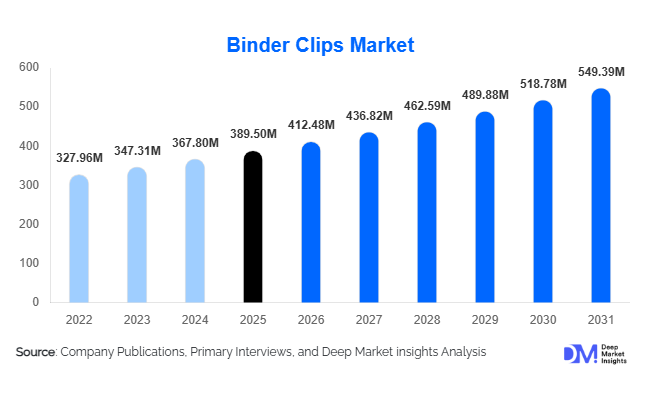

According to Deep Market Insights, the global binder clips market size was valued at USD 389.5 million in 2025 and is projected to grow from USD 412.48 million in 2026 to reach USD 549.39 million by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). Market growth is primarily driven by steady demand from corporate offices, educational institutions, and government administrative sectors, alongside expanding applications in retail packaging, home organization, and cable management. Despite increasing digitalization, binder clips continue to remain essential low-cost organizational tools due to their durability, reusability, and multifunctional applications across professional and personal environments.

Key Market Insights

- Institutional procurement remains the backbone of demand, with corporate offices and government agencies accounting for a major share of bulk purchases globally.

- Asia-Pacific dominates global consumption and manufacturing, supported by expanding SMEs, education investments, and large-scale production ecosystems.

- Sustainable and recyclable binder clips are gaining adoption, particularly across Europe and North America due to ESG procurement policies.

- E-commerce sales channels are expanding rapidly, enabling manufacturers to reach home-office users and small businesses directly.

- Multi-functional usage beyond paper organization, including cable management and packaging applications, is expanding total addressable demand.

- Automation in manufacturing and coating technologies is improving production efficiency and stabilizing pricing amid raw material volatility.

What are the latest trends in the binder clips market?

Rise of Sustainable and Reusable Office Supplies

Sustainability initiatives across corporations and educational institutions are significantly influencing stationery procurement decisions. Binder clips, being reusable metal products, are increasingly preferred over disposable fastening alternatives. Manufacturers are introducing recycled steel variants, low-emission coating processes, and plastic-free packaging solutions to align with ESG compliance standards. European and North American buyers are particularly prioritizing eco-certified office supplies, allowing suppliers to introduce premium product lines while improving brand differentiation. Sustainability labeling is also becoming a competitive advantage during institutional tenders and government procurement contracts.

Expansion of Home Office and Hybrid Work Culture

The growth of hybrid work models has expanded stationery consumption beyond traditional offices into households. Consumers are purchasing binder clips for workspace organization, cable management, and creative applications. Online marketplaces have enabled manufacturers to offer aesthetic designs, color-coded variants, and customized multi-pack formats tailored toward students, freelancers, and content creators. This shift is diversifying revenue streams and reducing dependency on corporate procurement cycles while strengthening direct-to-consumer sales channels globally.

What are the key drivers in the binder clips market?

Growth of SMEs and Administrative Infrastructure

The rapid expansion of small and medium enterprises worldwide continues to drive consistent demand for affordable office organization tools. Emerging economies across Asia and Africa are witnessing rising office formation rates, increasing recurring procurement of essential stationery supplies. Binder clips remain a preferred choice due to their durability and low replacement cost, making them highly attractive for cost-sensitive businesses.

Expansion of Global Education Systems

Increasing student enrollment and government investments in education infrastructure are supporting steady demand growth. Schools, universities, and training institutions require large volumes of paper organization tools for examinations, documentation, and administrative management. Educational procurement cycles ensure predictable yearly demand, stabilizing market growth even during economic fluctuations.

Growing Multi-Application Utility

Binder clips are increasingly used beyond document handling, including retail packaging, warehouse labeling, cable bundling, and creative DIY applications. This diversification broadens market scope and reduces dependency on traditional office demand, enabling stable long-term expansion across multiple industries.

What are the restraints for the global market?

Shift Toward Digital Documentation

The gradual adoption of digital workflows and cloud-based documentation systems reduces paper consumption in developed markets. While binder clips remain essential in hybrid environments, declining paper dependency limits volume growth potential, particularly in highly digitized corporate sectors.

Raw Material Price Volatility

Binder clips rely heavily on steel and coated metal inputs. Fluctuations in global metal prices impact manufacturing costs and compress profit margins for suppliers operating within price-sensitive stationery markets. Smaller manufacturers are particularly vulnerable to cost instability, requiring operational efficiency improvements to remain competitive.

What are the key opportunities in the binder clips industry?

Government and Institutional Procurement Expansion

Public-sector investments in administrative modernization and education infrastructure are creating large-scale procurement opportunities. Long-term supply contracts with schools, ministries, and public organizations offer stable demand visibility for manufacturers capable of meeting compliance and sustainability standards. Emerging economies present particularly strong opportunities due to expanding public service networks.

Sustainable Product Innovation

Eco-friendly binder clips manufactured using recycled metals and environmentally compliant coatings are gaining traction globally. Companies investing in sustainable production processes can capture premium institutional buyers and differentiate their product portfolios while improving long-term profitability.

E-commerce and Direct-to-Consumer Growth

Digital retail platforms are enabling manufacturers to bypass traditional distributors and reach consumers directly. Customized packaging sizes, decorative designs, and bundled office organization kits are attracting individual buyers and small businesses, opening new revenue streams beyond bulk procurement channels.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 389.50 Million |

| Market Size in 2026 | USD 412.48 Million |

| Market Size in 2031 | USD 549.39 Million |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Medium-sized binder clips (26–40 mm) dominate the global market, accounting for nearly 34% of total demand in 2025, primarily due to their optimal balance between holding capacity, portability, and multi-purpose usability. These clips provide sufficient strength to secure moderate document volumes while remaining convenient for daily handling, making them the preferred choice across corporate offices, educational institutions, and commercial packaging environments. Their standardized sizing also simplifies bulk procurement and inventory management for organizations, further strengthening adoption across institutional buyers. The continued shift toward hybrid workplaces and organized document management practices has reinforced demand for universally adaptable products, positioning medium-sized clips as the leading segment globally. Small and mini clips continue to witness stable demand in academic and personal applications where lightweight document handling is required, while large and extra-large variants remain essential in printing facilities, legal documentation management, and industrial recordkeeping environments where thicker paper stacks are common. Increasing emphasis on operational efficiency and workspace organization is expected to sustain strong demand for medium-sized products throughout the forecast period.

Material Type Insights

Powder-coated metal binder clips represent approximately 41% of the global market share, supported by their superior durability, corrosion resistance, and enhanced visual appeal compared to traditional finishes. The protective coating extends product lifespan, reducing replacement frequency for institutional buyers and lowering long-term procurement costs, which has emerged as a key driver behind segment leadership. Additionally, colored coatings enable efficient document categorization and workflow organization, particularly in corporate and educational environments managing large documentation volumes. Stainless steel variants are increasingly adopted within premium office environments and government procurement programs where longevity and structural reliability are prioritized. At the same time, recycled-material binder clips are emerging as a rapidly expanding niche segment as sustainability commitments and circular economy initiatives influence purchasing decisions globally. Growing environmental awareness among enterprises, coupled with regulatory encouragement for eco-friendly office supplies, is accelerating innovation in recyclable coatings and low-impact manufacturing processes, gradually reshaping material preferences across developed markets.

Distribution Channel Insights

Institutional and B2B procurement channels account for nearly 44% of global sales, reflecting the highly standardized purchasing behavior of corporations, educational institutions, and government organizations that procure stationery products in bulk through long-term supplier contracts. The dominance of this channel is driven by predictable consumption cycles, centralized procurement policies, and cost-efficiency advantages associated with volume purchasing. Office supply retailers continue to play an important role in serving small and medium-sized enterprises and independent professionals requiring flexible purchasing quantities. However, e-commerce platforms represent the fastest-growing distribution channel, supported by increasing digital procurement adoption, wider product availability, and competitive pricing transparency. The expansion of hybrid work models has accelerated online purchasing behavior, enabling businesses and individuals to replenish office supplies remotely while benefiting from subscription-based ordering and direct-to-consumer logistics networks. As digital retail infrastructure improves globally, online platforms are expected to capture a growing share of total binder clip sales.

End-Use Insights

Corporate offices remain the largest end-use segment, contributing approximately 36% of global demand, driven by continuous documentation requirements, administrative workflows, and organizational needs across finance, legal, consulting, and administrative sectors. The segment’s leadership is supported by recurring consumption patterns and standardized office supply procurement policies that ensure consistent product demand regardless of economic cycles. Educational institutions represent the fastest-growing end-use category, fueled by rising global student enrollment, expanding school infrastructure, and increased public and private investment in education systems, particularly across emerging economies. Binder clips are widely utilized for assignments, record organization, and administrative documentation within academic environments, strengthening long-term consumption trends. Meanwhile, retail and packaging businesses are emerging as important growth contributors as binder clips gain adoption for temporary sealing, price tagging, labeling, and merchandising applications. This diversification beyond traditional stationery usage is expanding the functional scope of binder clips and enabling penetration into non-office commercial applications.

Explore more data points, trends and opportunities Download Free Sample Report

Binder Clips Market Segmentations

By Product Size

- Mini Binder Clips

- Small Binder Clips

- Medium Binder Clips

- Large Binder Clips

- Extra-Large Binder Clips

By Material Type

- Steel Binder Clips

- Stainless Steel Binder Clips

- Powder-Coated Metal Binder Clips

- Plastic-Handled Binder Clips

- Recycled Material Binder Clips

By Distribution Channel

- Office Supply Retail Stores

- Supermarkets & Hypermarkets

- E-commerce Platforms

- Institutional & B2B Procurement

- Wholesale & Stationery Distributors

By End Use

- Corporate Offices

- Educational Institutions

- Government & Administrative Offices

- Printing & Publishing Industry

- Retail & Packaging Businesses

- Household & Personal Use

Regional Insights

North America

North America accounts for nearly 24% of the global binder clips market, led primarily by the United States, where structured procurement frameworks and mature corporate office infrastructure support stable and recurring demand. Regional growth is driven by widespread adoption of organized workplace practices, strong presence of large enterprises, and consistent consumption from educational institutions and government offices. Increasing emphasis on sustainable procurement policies has accelerated demand for recyclable materials and premium powder-coated products, particularly among corporations pursuing environmental compliance goals. Additionally, the expansion of remote and hybrid work arrangements has strengthened e-commerce distribution channels, allowing suppliers to reach decentralized consumers more efficiently. Continuous innovation in office organization solutions and premium stationery branding further contributes to steady regional market expansion.

Europe

Europe holds approximately 20% market share, with Germany, the United Kingdom, and France serving as major demand centers. Regional growth is strongly influenced by stringent environmental regulations and sustainability-focused procurement policies that encourage adoption of recyclable, eco-certified, and long-life office supplies. Institutional buyers increasingly prioritize environmentally responsible sourcing, prompting manufacturers to introduce low-emission production processes and recycled material offerings. Stable demand from public administration offices, educational systems, and professional service industries supports consistent consumption levels across the region. Furthermore, increasing workplace organization standards and ergonomic office trends continue to reinforce the role of durable stationery products within European administrative environments.

Asia-Pacific

Asia-Pacific dominates the global market with around 42% share in 2025, supported by strong manufacturing capabilities, expanding education systems, and rapid commercial development. China remains the leading production hub and export supplier, benefiting from large-scale manufacturing infrastructure and cost-efficient production networks. India represents the fastest-growing national market, expanding at nearly 8% CAGR, driven by rising small and medium enterprise formation, expanding corporate employment, and significant investments in education infrastructure. Increasing urbanization and office space development across Southeast Asia are further strengthening regional consumption. Japan and developed Asian economies contribute stable institutional demand characterized by high-quality product preferences and consistent procurement cycles. The combination of manufacturing dominance and growing domestic consumption positions Asia-Pacific as the primary engine of global binder clip market growth.

Latin America

Latin America accounts for roughly 8% of global demand, led by Brazil and Mexico, where improving economic activity and expanding retail distribution networks are supporting stationery market growth. Regional demand is increasingly driven by education sector reforms, rising school enrollment rates, and modernization of administrative systems across both public and private institutions. Growth of organized retail channels and expanding e-commerce penetration are improving product accessibility, particularly in urban centers. As businesses formalize operations and administrative documentation requirements increase, binder clip consumption is expected to grow steadily across commercial and institutional segments.

Middle East & Africa

The Middle East & Africa region is witnessing gradual adoption driven by administrative expansion, economic diversification initiatives, and rising education investments in countries such as the UAE, Saudi Arabia, and South Africa. Government modernization programs and digital transformation efforts are increasing documentation management needs within public sector organizations, supporting steady procurement growth. Expansion of private education institutions and corporate office infrastructure is further contributing to regional demand. Additionally, improving distribution networks and growing awareness of organized office practices are enhancing market penetration, positioning the region as an emerging growth opportunity over the long term.

Key Players in the Binder Clips Market

- ACCO Brands Corporation

- Newell Brands Inc.

- Kokuyo Co., Ltd.

- PLUS Corporation

- Deli Group Co., Ltd.

- Shuter Enterprise Co., Ltd.

- MAX Co., Ltd.

- Comix Group Co., Ltd.

- Bostitch Office

- Officemate International Corporation

- 3M Company

- Maped Group

- Snopake Brands Ltd.

- Lion Office Products Corp.

- Guangbo Group Co., Ltd.