Beard Grooming Products Market Size

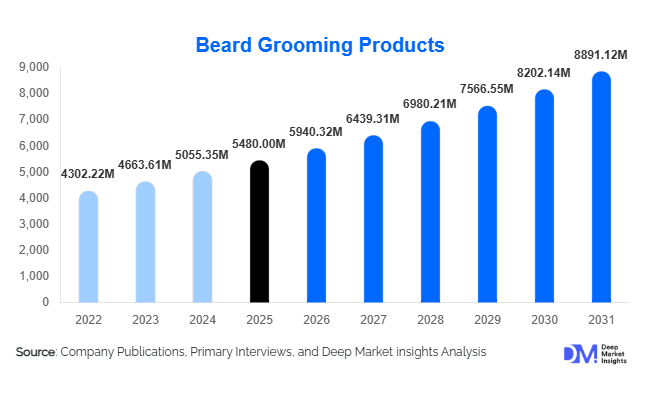

According to Deep Market Insights, the global beard grooming products market size was valued at USD 5,480 million in 2025 and is projected to grow from USD 5940.32 million in 2026 to reach USD 8891.12 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). The beard grooming products market growth is primarily driven by increasing male grooming awareness, rising disposable incomes, social media-driven style trends, and the premiumization of men’s personal care portfolios worldwide.

Key Market Insights

- Beard oils remain the dominant product category, accounting for nearly 34% of global revenue in 2025 due to universal daily usage and hydration benefits.

- Natural and organic formulations are gaining rapid traction, representing approximately 38% of the total market as consumers shift toward clean-label grooming products.

- North America dominates the global market, contributing about 35% of total revenue in 2025, led by strong per capita spending in the United States.

- Asia-Pacific is the fastest-growing region, expanding at over 10% CAGR, driven by rising urban male grooming adoption in India, China, and Southeast Asia.

- Online retail channels account for nearly 36% of global sales, reflecting strong growth in direct-to-consumer and subscription-based grooming models.

- Premium and mid-premium segments together contribute more than 60% of total value share, highlighting consumer willingness to pay for quality formulations.

What are the latest trends in the beard grooming products market?

Clean-Label and Dermatologically-Tested Formulations

The market is witnessing strong momentum toward natural, organic, vegan, and cruelty-free formulations. Consumers increasingly scrutinize ingredient lists, preferring botanical oils such as argan, jojoba, and almond over synthetic alternatives. Dermatologically-tested and hypoallergenic certifications are becoming strong differentiators, particularly in North America and Europe. Brands are reformulating products to eliminate parabens, sulfates, and artificial fragrances while adopting sustainable packaging materials. This trend is enabling premium pricing and enhancing brand loyalty among health-conscious consumers.

Digital-First and Subscription-Based Retail Expansion

E-commerce and direct-to-consumer (D2C) channels are transforming distribution strategies. Online retail accounts for over one-third of total market sales, supported by subscription-based replenishment models for beard oils and grooming kits. AI-driven recommendation engines, influencer marketing, and personalized product bundles are increasing customer retention rates. Social media platforms are playing a critical role in educating consumers through grooming tutorials, product reviews, and influencer endorsements, accelerating global product penetration.

What are the key drivers in the beard grooming products market?

Rising Male Grooming Awareness

The normalization of beards across professional and social settings has significantly expanded demand for maintenance products. Younger demographics aged 18–35 are investing in structured grooming routines, including cleansing, conditioning, styling, and nourishment. The broader men’s personal care industry expansion has positively influenced beard-specific SKUs, encouraging portfolio diversification among major personal care manufacturers.

Premiumization and Brand Differentiation

Consumers are increasingly willing to spend more on specialized beard products offering targeted benefits such as growth stimulation, anti-frizz properties, and skin nourishment. The mid-premium segment alone holds approximately 41% of market share, reflecting a balance between affordability and perceived quality. Luxury offerings featuring rare botanical extracts and designer packaging are further elevating average selling prices globally.

What are the restraints for the global market?

Volatility in Raw Material Prices

Essential oils and natural extracts are subject to agricultural fluctuations, impacting production costs. Price volatility in argan and jojoba oils can compress manufacturer margins, particularly for small and mid-sized brands.

Market Saturation in Developed Economies

North America and Western Europe face intense brand competition and SKU overcrowding. High marketing expenditures and price-based competition limit new entrant scalability without strong differentiation.

What are the key opportunities in the beard grooming products industry?

Emerging Market Penetration

Asia-Pacific and the Middle East present underpenetrated yet high-growth opportunities. Rising disposable incomes and urban lifestyle shifts in India, China, the UAE, and Saudi Arabia are driving double-digit growth rates. Localization strategies and climate-specific formulations can unlock incremental revenue streams.

Technology-Integrated Grooming Solutions

Smart grooming tools, AI-powered beard style recommendations, and personalized product formulations represent high-margin innovation areas. Subscription bundling and digital profiling can significantly enhance lifetime customer value while reducing churn rates.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5480 Million |

| Market Size in 2026 | USD 5940.32 Million |

| Market Size in 2031 | USD 8891.12 Million |

| CAGR | 8.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Beard oils remain the leading product segment, accounting for approximately 34% of the global market share in 2025, making them the single largest revenue contributor within the beard grooming products market. Their dominance is driven by universal applicability across beard lengths and textures, daily use, and multifunctional benefits, including moisturization, itch relief, skin nourishment, and shine enhancement. The growing prevalence of longer and styled beards, particularly among urban male consumers aged 20–40, continues to sustain repeat purchases. Additionally, the shift toward natural carrier oils such as argan and jojoba has elevated average selling prices within this segment.

Beard balms and waxes follow as strong secondary categories, supported by rising demand for styling control in corporate and professional environments. These products are particularly popular in North America and Europe, where structured beard aesthetics are mainstream. Beard shampoos and conditioners are gaining traction as consumers adopt multi-step grooming regimens, mirroring trends in haircare routines. Grooming kits are increasingly positioned as premium gifting solutions, especially during festive seasons such as Christmas and Father’s Day, leading to seasonal revenue spikes in Q4 across mature markets.

Ingredient Profile Insights

Natural and organic formulations lead the ingredient profile segment, capturing nearly 38% of global revenue in 2025. The primary driver behind this leadership is the accelerating clean-beauty movement, with consumers demanding transparency, plant-based ingredients, and cruelty-free certifications. Growth is particularly strong in Europe and North America, where regulatory awareness and sustainability concerns are high. Brands leveraging vegan certifications and eco-friendly packaging are achieving stronger brand loyalty and premium pricing advantages.

Conventional formulations continue to maintain volume share in price-sensitive markets across Asia-Pacific and Latin America, where affordability drives purchasing decisions. However, growth momentum clearly favors botanical-based and dermatologist-tested products. Hypoallergenic variants are expanding rapidly within premium SKUs, especially among consumers with sensitive skin concerns, contributing to higher margin realization for manufacturers.

Distribution Channel Insights

Online retail dominates distribution, accounting for approximately 36% of global sales in 2025. The leading driver for this segment is the rapid adoption of direct-to-consumer (D2C) models, subscription replenishment services, and influencer-led marketing strategies. E-commerce platforms enable global brand access, competitive pricing comparisons, and targeted promotions, particularly among millennials and Gen Z consumers. Digital advertising analytics and AI-powered product recommendations further enhance customer acquisition and retention rates.

Specialty stores and hypermarkets maintain a steady share, particularly in urban centers where impulse purchases and in-store brand visibility influence buying behavior. Professional salon and barbershop channels play a strategic role in premium brand discovery, enabling experiential product trials and upselling, which contribute to higher-value transactions and brand credibility.

End-Use Insights

Individual consumers account for approximately 72% of total market demand, driven by daily grooming routines and the increasing normalization of beards in professional settings. The growth driver for this segment lies in rising self-care awareness and social media influence, which encourage structured grooming habits at home. Subscription-based oil and grooming kit models are further strengthening recurring revenue streams in this segment.

Professional barbershops represent the fastest-growing end-use segment, expanding at over 9% CAGR. The global barbershop industry, valued at over USD 30 billion, is playing a significant role in premium product endorsement. Experiential grooming services, beard sculpting trends, and product bundling during salon visits are driving higher product penetration. Export-driven demand is also notable, particularly in the Middle East and Southeast Asia, where premium grooming brands are increasingly supplied through professional channels.

Explore more data points, trends and opportunities Download Free Sample Report

Beard Grooming Products Market Segmentations

By Product Type

- Beard Oils

- Beard Balms

- Beard Waxes

- Beard Shampoos & Cleansers

- Beard Conditioners

- Beard Serums & Growth Solutions

- Beard Dyes & Colorants

- Beard Grooming Kits

- Beard Tools & Accessories

By Ingredient Profile

- Natural & Organic Formulations

- Conventional/Synthetic Formulations

- Vegan & Cruelty-Free Certified Products

- Dermatologically-Tested / Hypoallergenic Products

By Distribution Channel

- Online Retail

- Hypermarkets & Supermarkets

- Specialty Stores

- Pharmacies & Drug Stores

- Professional Salon & Barbershop Sales

By End-Use

- Individual Consumers (Home Use)

- Professional Barbershops & Salons

Regional Insights

North America

North America leads the global market with approximately 35% share in 2025, with the United States alone contributing nearly 28% of global revenue. Regional growth is driven by high disposable incomes, strong penetration of digital marketing, celebrity and influencer endorsements, and a well-established men’s grooming culture. Premiumization trends are particularly strong in the U.S., where consumers are willing to pay for organic and dermatologist-tested formulations. Canada contributes steadily, supported by expanding clean-label demand and rising e-commerce adoption.

Europe

Europe accounts for approximately 27% of global revenue, led by the U.K., Germany, France, and Italy. Growth in this region is driven by high awareness of sustainable and organic grooming products, especially in Germany, where demand for certified natural cosmetics is strong. Regulatory focus on ingredient transparency further supports premium product sales. The U.K. market benefits from a strong barbershop culture, while Southern Europe shows increasing demand for styling-oriented products such as balms and waxes.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 10% CAGR. Rapid urbanization, increasing middle-class income, and Westernized fashion influence are major growth drivers in India and China. India benefits from a young demographic profile and rising D2C grooming startups, while China’s premium segment is fueled by e-commerce expansion and social commerce platforms. Japan and South Korea contribute through innovation-driven demand, particularly for skincare-grooming hybrid products and premium formulations.

Latin America

Latin America holds approximately 5% of the global share, led by Brazil and Mexico. Regional growth is supported by expanding retail infrastructure, increasing digital penetration, and rising grooming awareness among younger male consumers. Brazil’s strong beauty and personal care industry provides a favorable ecosystem for beard product adoption, while Mexico benefits from growing barbershop chains and urban male fashion trends.

Middle East & Africa

The Middle East and Africa contribute nearly 6–7% of global revenue. Growth in the Middle East, particularly in the UAE and Saudi Arabia, is driven by cultural emphasis on beard grooming and premium lifestyle preferences. High per capita income and luxury retail presence further support demand for high-end grooming oils and styling products. In Africa, South Africa leads regional consumption due to established retail networks and increasing urban grooming trends. Strong import flows from North America and Europe continue to shape premium product availability in the region.

Key Players in the Beard Grooming Products Market

- Procter & Gamble

- Unilever

- L'Oréal

- Beiersdorf

- Edgewell Personal Care

- The Estée Lauder Companies

- Revlon

- Colgate-Palmolive

- Coty Inc.

- Kao Corporation

- Shiseido

- Honasa Consumer Ltd.

- Bombay Shaving Company

- Beardbrand

- Mountaineer Brand